Eddie Lampert and AutoZone, Part 1: An Excellent Company

The Owner's Memo #14; By 1997, AutoZone showed a lot of proof that it was a great company providing customers with something they couldn't get from anyone else.

There has been one investment story I’ve been obsessed with for many years, and now, I’ve finally taken the time to break it down: AutoZone.

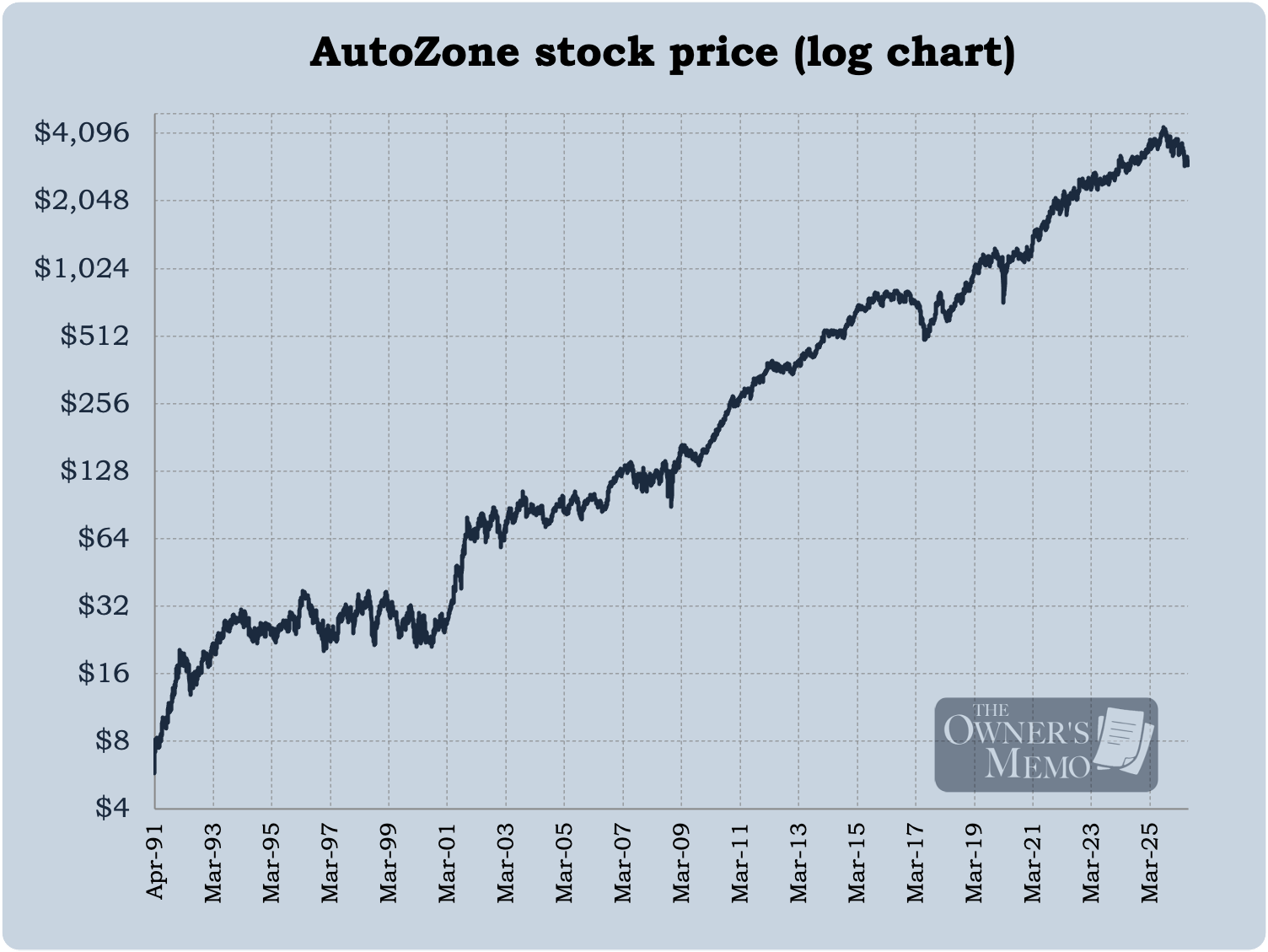

Over the past 35 years, since the company’s IPO in April 1991 through July 13, 2026, AutoZone’s common stock has increased 448-fold, which equates to a compounded annual growth rate of 18.9%. Moreover, the company is famous for dramatically shrinking its share count during that time by 89%, from 152.7 million shares at the peak in June 1998 to 16.5 million shares as of May 2026.

Share buybacks are a widely misunderstood corporate action, both by critics and, to a lesser extent, by adherents.

AutoZone has been the poster-child for share buybacks done well. And the conventional explanation is that these share buybacks were the primary driver that led to great returns. But that conventional explanation is incomplete

Eddie Lampert and AutoZone

What first turned me on to AutoZone was reading, perhaps around the year 2007, about Eddie Lampert, then a superstar investor who had accumulated a large stake in the retailer, had apparently prodded management to begin buying back stock, and had earned stellar returns on his investment.1 I’ve always wondered what Lampert saw in the stock and how and why share buybacks seemed to be very effective in producing returns for the company’s equity investors.

Although AutoZone has produced tremendous returns for shareholders over its entire life as a public company, I’ll limit the analysis here to Lampert’s investment in AutoZone, from 1997 to 2012, so as to definitively restrict us to a single point in time at the start so we can try to see the same potential he saw when he invested.

The first public disclosure of Lampert’s ownership that I could find is a 13D filing from August 1998 for several of Lampert’s investment vehicles that lists a combined ownership of exactly 11 million shares, or 7.2% of the company’s stock.2 According to a BusinessWeek article, Lampert started accumulating AutoZone in 1997, although no specific date is given. The SEC requires investors to file a 13D within five business days of acquiring 5% or more of a company’s stock, so it seems likely that Lampert owned less than 5% of AutoZone’s stock starting sometime in 1997. I’ll assume he started buying in Q2 of 1997 and that he had access to the 1996 annual report and any disclosures prior to March 31, 1997.

AutoZone was an excellent company

AutoZone was and still is in the business of auto parts retailing, and it’s been in business since 1979. Here is a succinct explanation of the company’s business from the 1996 10-K:

The Company began operations in 1979 and at August 31, 1996, operated 1,423 stores in 27 states, principally located in the Sunbelt and Midwest regions of the United States. Each AutoZone store carries an extensive product line, including new and re-manufactured automotive hard parts, such as alternators, starters, water pumps, brake shoes and pads, carburetors, clutches and engines; maintenance items, such as oil, antifreeze, transmission, brake and power steering fluids, engine additives, protectants and waxes; and accessories, such as car stereos and floor mats.

Two things jumped out at me when I opened the 1996 10-K report:

how consistent their business was, and

how profitable it seemed to be.

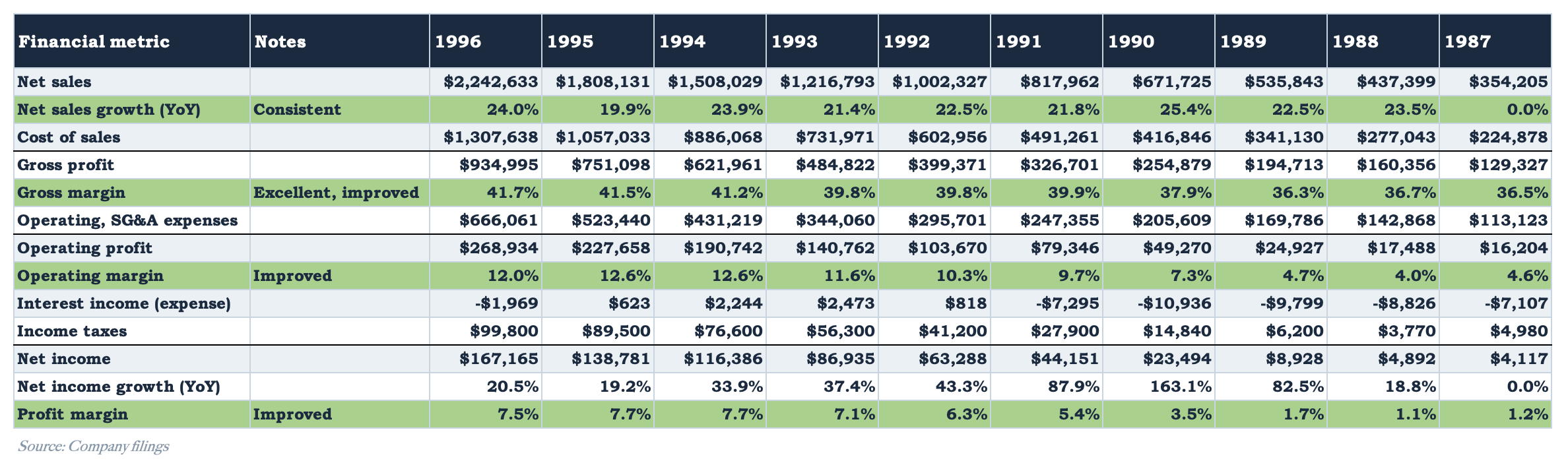

In fact, as a loose confirmation of the consistency, AutoZone conveniently laid out 10-year financial histories in its annual reports and 10-K’s; I couldn’t help but feel that management was showing off how consistently the company was growing sales and earning more and more income. Below, I reproduce an abbreviated version of AutoZone’s income statement that appeared in the 10-K.

From the data above, it is not hard to see that AutoZone had been doing very well over the ten years prior to 1997:

Net sales were growing consistently in the range of 20-25% per year. That suggests the company was continuing to tap into some form of unsatisfied demand.

Gross margins were high, and they had improved. That suggests that customers were willing to pay up for whatever AutoZone was providing them and/or AutoZone was paying less to obtain salable items.

Operating and profit margins were good, and they had improved a lot. That suggests the company had been improving the way it was run and/or that its business model was benefitting from scale.

Why was AutoZone able to perform so well? What was the company’s business model?

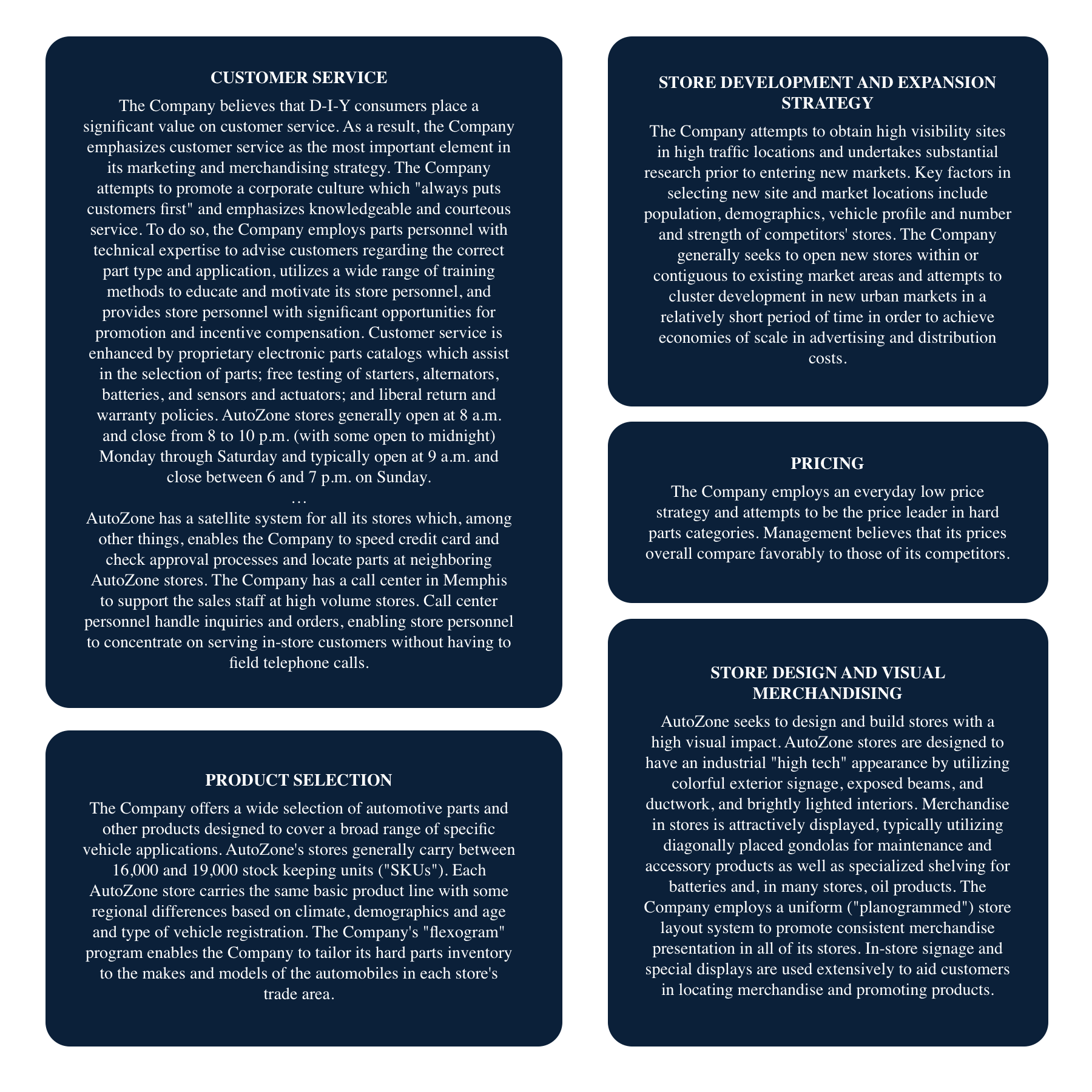

AutoZone had a simple and compelling business model: It was “professionalizing” the auto parts retailing business, opening larger stores with more selection, in convenient locations, with good prices. From the 1996 10-K:

AutoZone is dedicated to a marketing and merchandising strategy to provide customers with superior service, value and parts selection at conveniently located, well-designed stores. The Company has implemented this strategy primarily with knowledgeable and motivated store personnel trained to emphasize prompt and courteous customer service, through an everyday low price policy and by maintaining an extensive product line with an emphasis on automotive hard parts. AutoZone’s stores are generally situated in high-visibility locations and provide a distinctive merchandise presentation in an attractive store environment.

Management takes the time in its 10-K to expound upon each part of its retail strategy by discussing customer service, product selection, price, and store location and design at length. For those interested in a more in-depth look, I’ve reproduced their strategy and philosophy on each below:

I’m quoting extensively from the 10-K here in order to relay something important about the retail industry: customers do not shop at great retail stores for one reason alone. They need several compelling reasons. I’m reminded of the following quote from Sam Walton’s autobiography, Made in America:3

...the secret to successful retailing is to give your customers what they want. And really, if you think about it from your point of view, as a customer, you want everything: a wide assortment of good quality merchandise; the lowest possible prices; guaranteed satisfaction with what you buy; friendly, knowledgeable service; convenient hours; free parking; a pleasant shopping experience. You love it when you visit a store that somehow exceeds your expectations, and you hate it when the store inconveniences you, or gives you a hard time, or just pretends you’re invisible.

Of course, it would be naive to suggest that AutoZone was another Wal-Mart simply on the basis of quotations from the management team. In fact, a skeptic would argue that “superior service, value and parts selection at conveniently located, well-designed stores” are the kind of thing any retailer would claim.

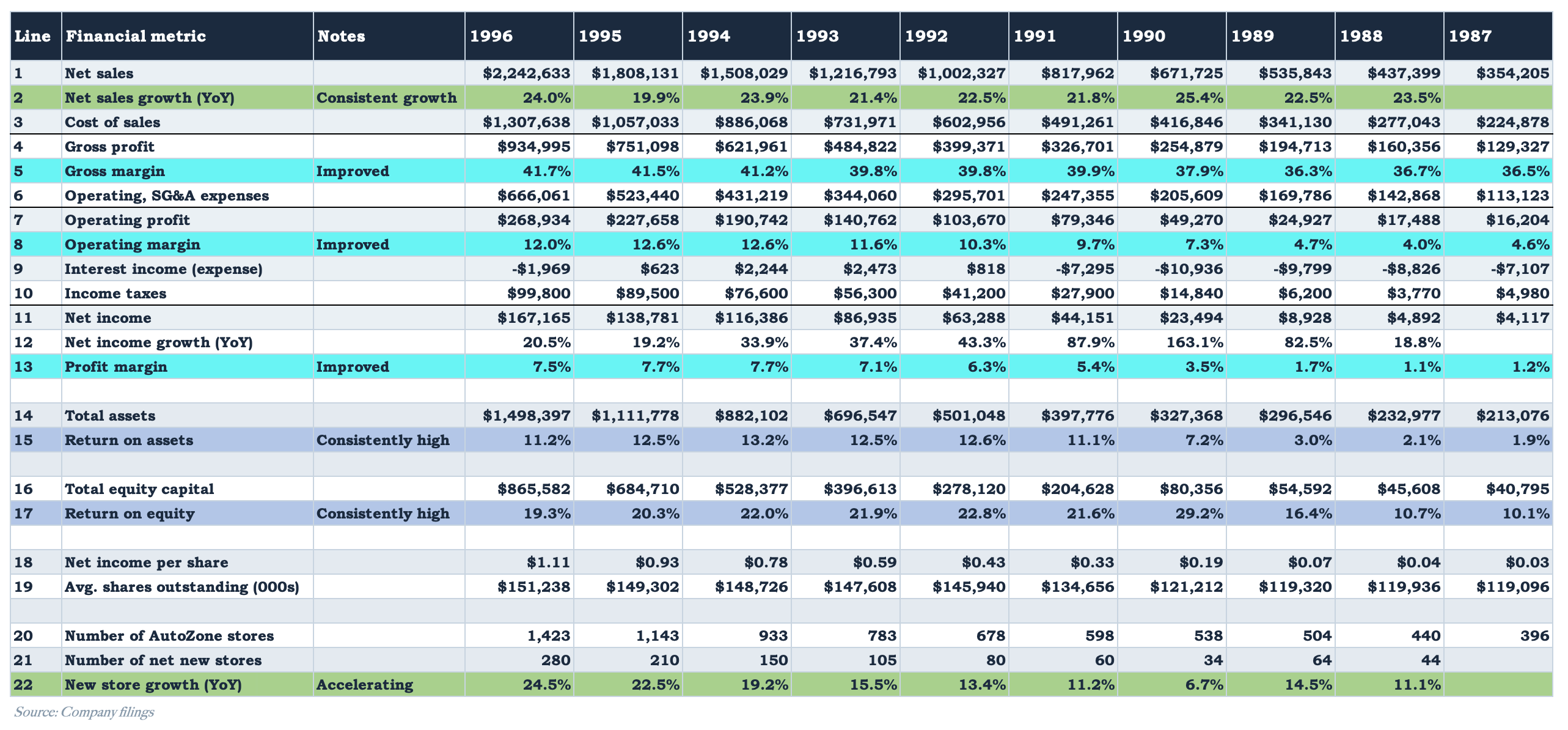

In order to understand whether or not the stores were truly resonating with customers, I needed some better proof. And I found it in the company’s financials. The table below shows an expanded version of the financials shown earlier.

These financials show a few things over the course of ten years through 1996, which I have highlighted in different colors:

Green lines: AutoZone was growing consistently over those ten years, with net sales growth, as evidenced by line 2, in the 20-25% range. A careful reading of the 10-K shows that the company was doing this with a combination of good same-store sales growth, and, more importantly, very strong new store growth (see line 20). In fact, new store growth was accelerating from 1990 to 1996; the company was growing faster.

Teal lines: AutoZone’s underlying business was improving too. Lines 5, 8, and 13 highlight the company’s margins. Each had increased over the past several years since 1989. Higher margins indicate that the company was benefiting from scale by getting more favorable purchasing terms from suppliers, benefiting from centralization of certain expenses (like advertising), or simply benefiting from its experience in running a better, more profitable business as time went by.4

Blue lines: AutoZone consistently generated a high amount of profit relative to the capital the business employed, as shown in lines 15 and 17, return on average assets and return on average equity capital. This implies that the company was delivering something (or things, plural) to customers that other retailers were not or could not. Otherwise, I would expect the company’s return to be falling as other competitors swooped in and deployed their own capital to challenge AutoZone.

So from the 1996 10-K alone, AutoZone looked like an excellent business, growing, profitable, and earning high returns on its capital. But a great business in a tapped-out market is a different proposition than a great business with room to run. Before Lampert could be confident that what he was seeing would continue, he needed to understand the industry AutoZone was operating in: how large it was, who else competed in it, and how much of it AutoZone had already taken.

Next week, in Part Two, we’ll cover each of those things.

Lampert was developing a reputation as a great investment manager, with a reported CAGR at his hedge fund of 29% per year from 1988 through 2004. There were several articles written about him in the 2000’s and early 2010’s, like the ones I list below. Lampert, famously, made a large investment in Sears, which proved to be very difficult, failing to become the turnaround story it was slated to be, and seemingly ending the fascination with Lampert as “the next Warren Buffett”.

The Next Warren Buffett?, BusinessWeek, November 22, 2004.

Eddie Lampert: The best investor of his generation, CNNMoney, February 6, 2006.

There seem to be no public filings or reports of exactly when Lampert began accumulating AutoZone stock. The BusinessWeek article listed in the prior footnote describes Lampert as having started making his purchases in 1997, without providing an exact date.

The 13D filing lists five entities as owning AutoZone stock as of August 21, 1998: ESL Partners, L.P. (a Delaware limited partnership), ESL Limited (a Bermuda corporation), ESL Institutional Partners, L.P. (a Delaware limited partnership), Acres Partners, L.P. (a Delaware limited partnership), and Marion Partners, L.P. (a Delaware limited partnership). In future disclosures, Lampert would also list five other vehicles too: ESL Investors, L.L.C. (a Delaware limited liability company), RBS Investment Management, L.L.C. (a Delaware limited liability company), Tynan, LLC (a Delaware limited liability company), RBS Partners, L.P. (a Delaware limited partnership), and ESL Investments, Inc. (a Delaware corporation).

Made in America by Sam Walton with John Huey. Chapter 12.

All of the above was true for AutoZone. On the “experience” front, for example, AutoZone’s stores were evolving over time, most notably with the company’s new stores becoming larger and larger.