Li Lu’s 7x Return on Timberland, Part 1

The Owner's Memo #3

This is Part One of a three part series on Li Lu’s investment in Timberland. Part Two and Part Three are also available.

In the fall of 1998, Li Lu discovered a great investment opportunity in the well-known boot manufacturer Timberland that would reportedly earn him a 7x return on his money. This is that story.

In 2006, Li gave a well-known talk to Columbia Business School students. The talk is perhaps the best source for learning more about Li’s investment style and some of his early investment ideas.

At one point in the talk, Li discusses his investment from the late 1990’s in Timberland Co., the US manufacturer and retailer of boots, apparel, and other footwear. According to Li, he became aware of the stock in the fall of 1998 when it was battered due to the Asian Financial Crisis and appeared to be cheap. Li describes some of the work he did over the course of just a few weeks, the investment he made, and the result: a stunning 6-7 times return in just two years.

Let’s find out more.

How Li discovered the opportunity in Timberland

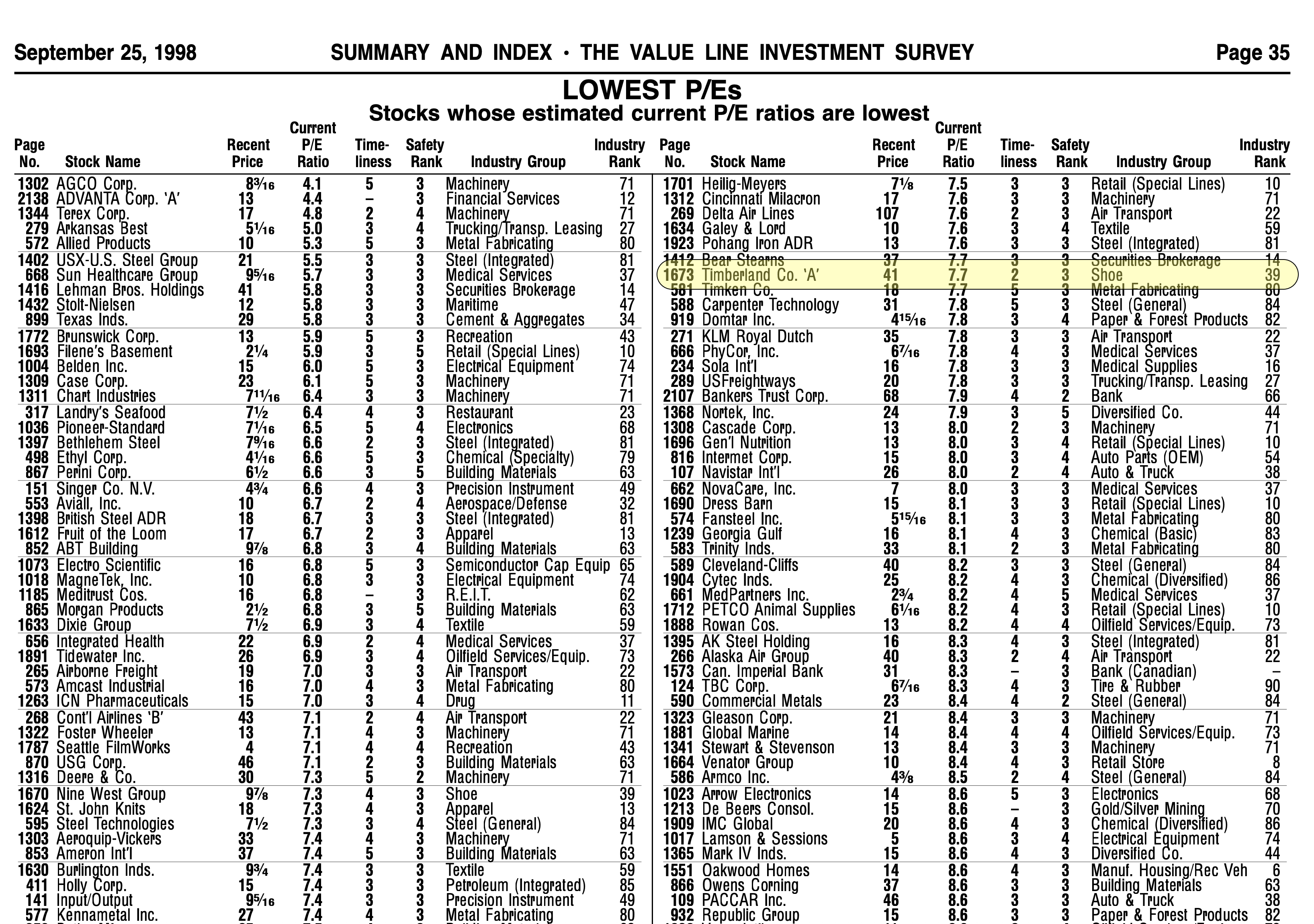

Li first discusses one of the ways he gets ideas: by reading manuals. He mentions Value Line specifically and, later in the talk, manuals from S&P. He tells the class how he loved to read every issue of Value Line front to back, page after page, how it was a great way for him to learn about many different businesses. He also specifically mentions checking the “new low” lists, those stocks with the lowest price-to-earnings and price-to-book ratios.

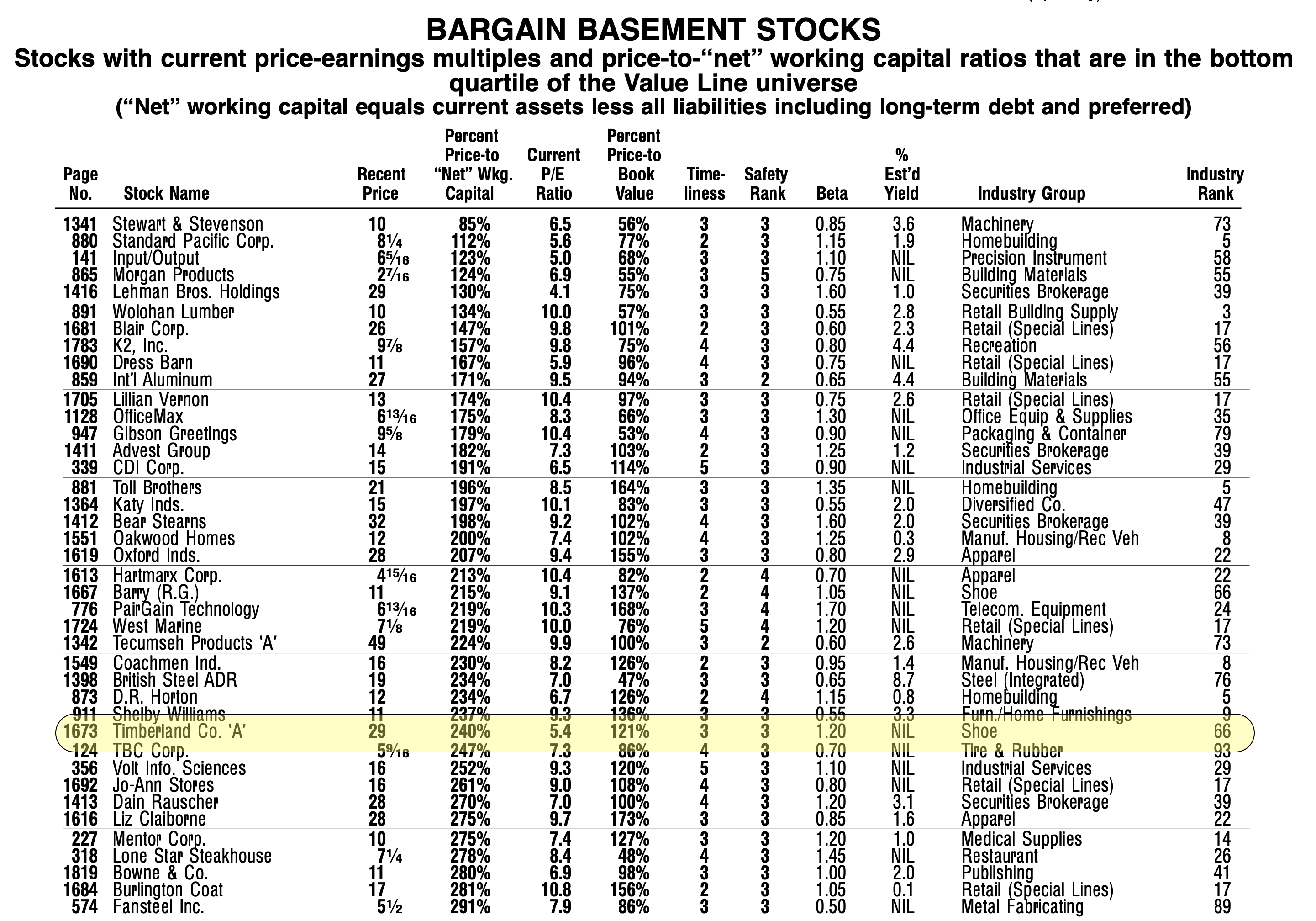

Every weekly issue of Value Line comes with a “Summary & Index” that lists all the stocks profiled by the publication and a variety of valuation tables, like “Lowest P/E’s” and “Widest Discounts from Book Value”.

I went back and checked all the Value Line issues from the summer of 1998 through the spring of 1999, and here is what I found.

Timberland first appeared on the Lowest P/E list on September 25th, 1998, and it remained on the list until February 5, 1999. It also first appeared on the “Bargain Basement Stocks” list in the October 2nd issue and remained on that list through January 8th, 1999. It may be that Li first discovered the opportunity in Timberland reading either of these lists or one just like them from another issue in the fall of 1998.

Let’s go back to October 1998

A good case study must put the analyst back at the moment in time of the investment, as much as possible, without the benefit of information from after that time. Li recalls that he made the investment in Timberland around $28 per share. According to Value Line, the stock traded as low as $28.1 in October of 1998, so it may be that Li first discovered the stock before that time. He may have seen it in the September 25th issue or an October issue and made his investment in the brief period in late October when the stock was just above $28. We’ll take Li at his word and assume he made his investment some time in October.

Establishing the exact time frame here is important, so that we can understand what company filings and other news articles Li would have had access to.

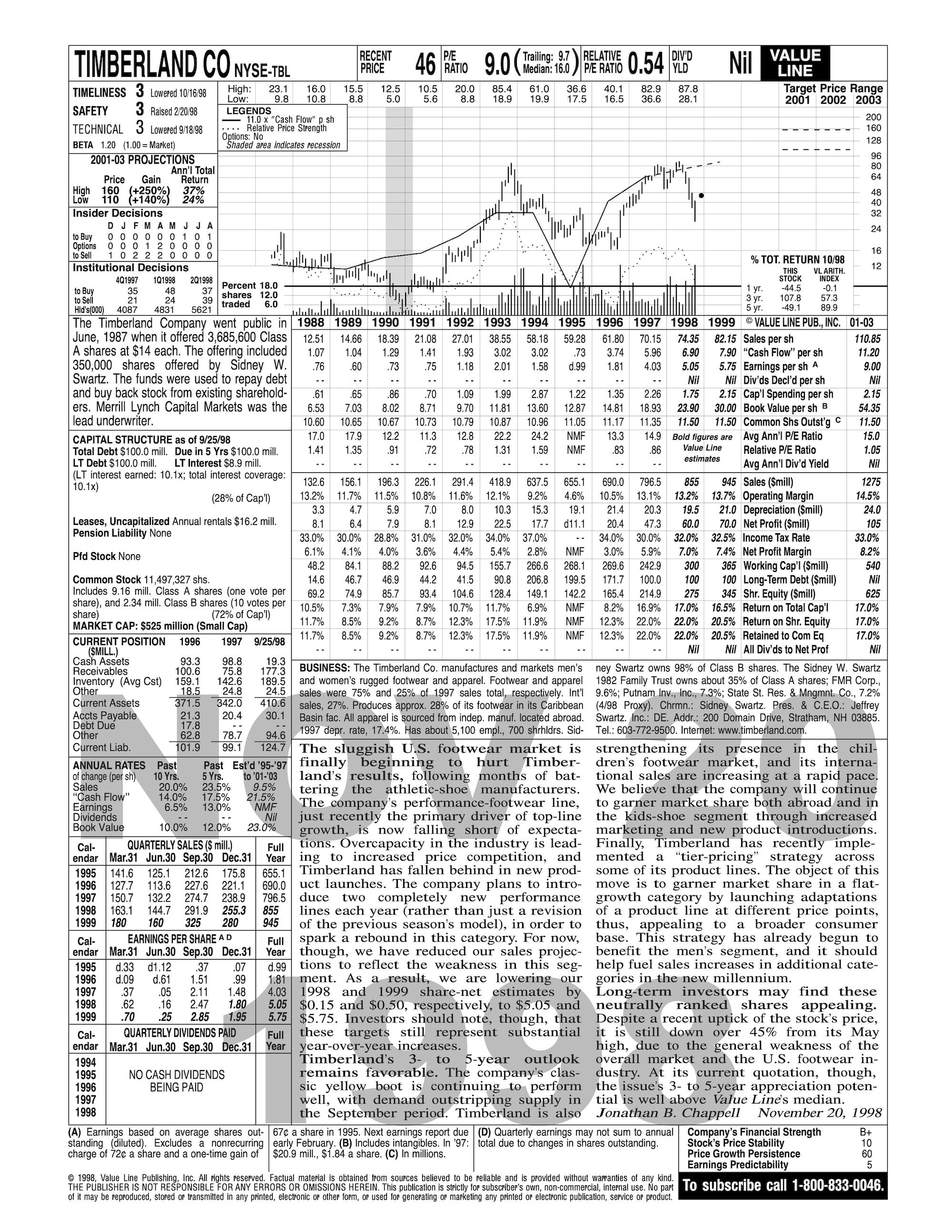

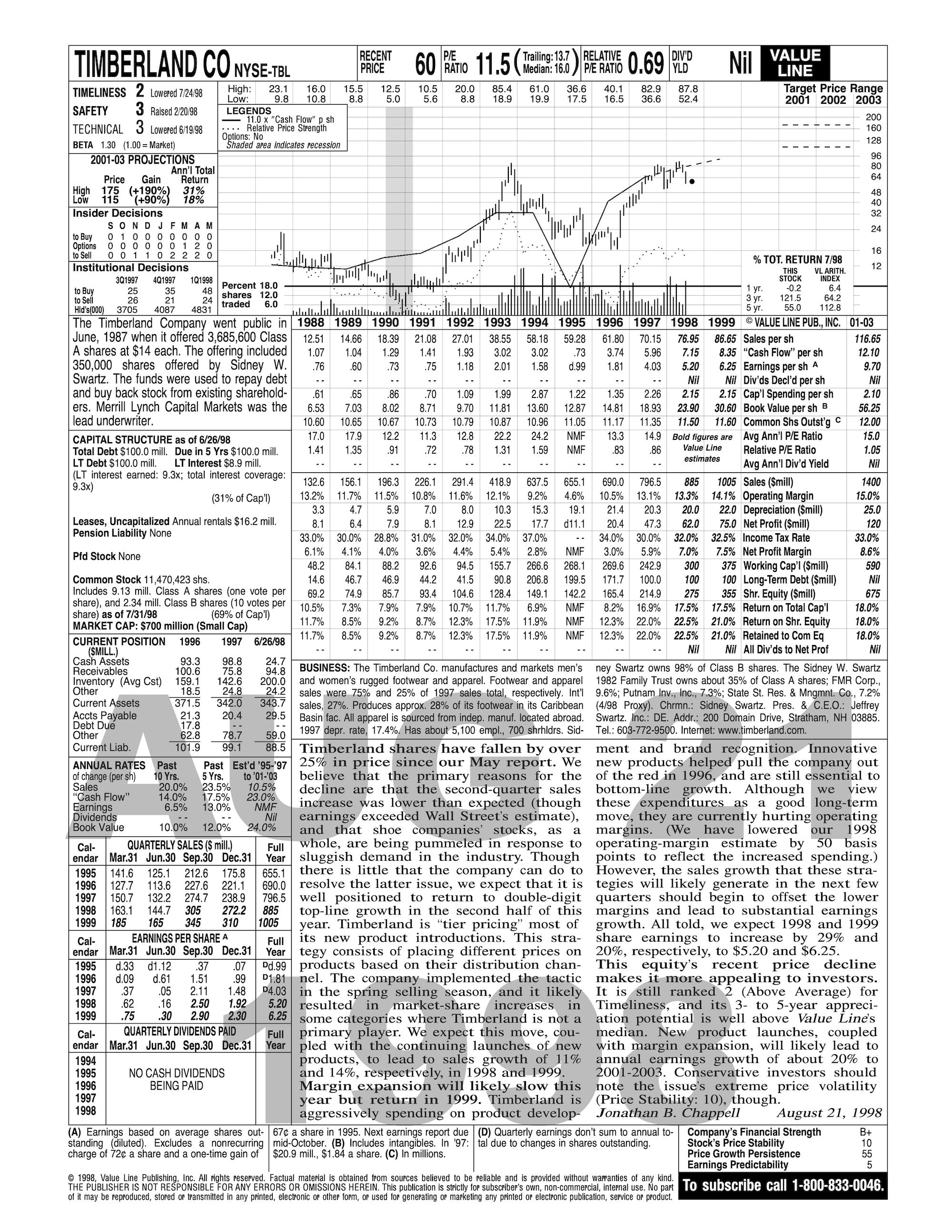

Li proceeds to discuss with the class his investment in Timberland by using the following page from Value Line from its November 20, 1998 issue. Note, however, that if Li was working in October, he would have only had access to the August 21, 1998 issue. Both are shown below.

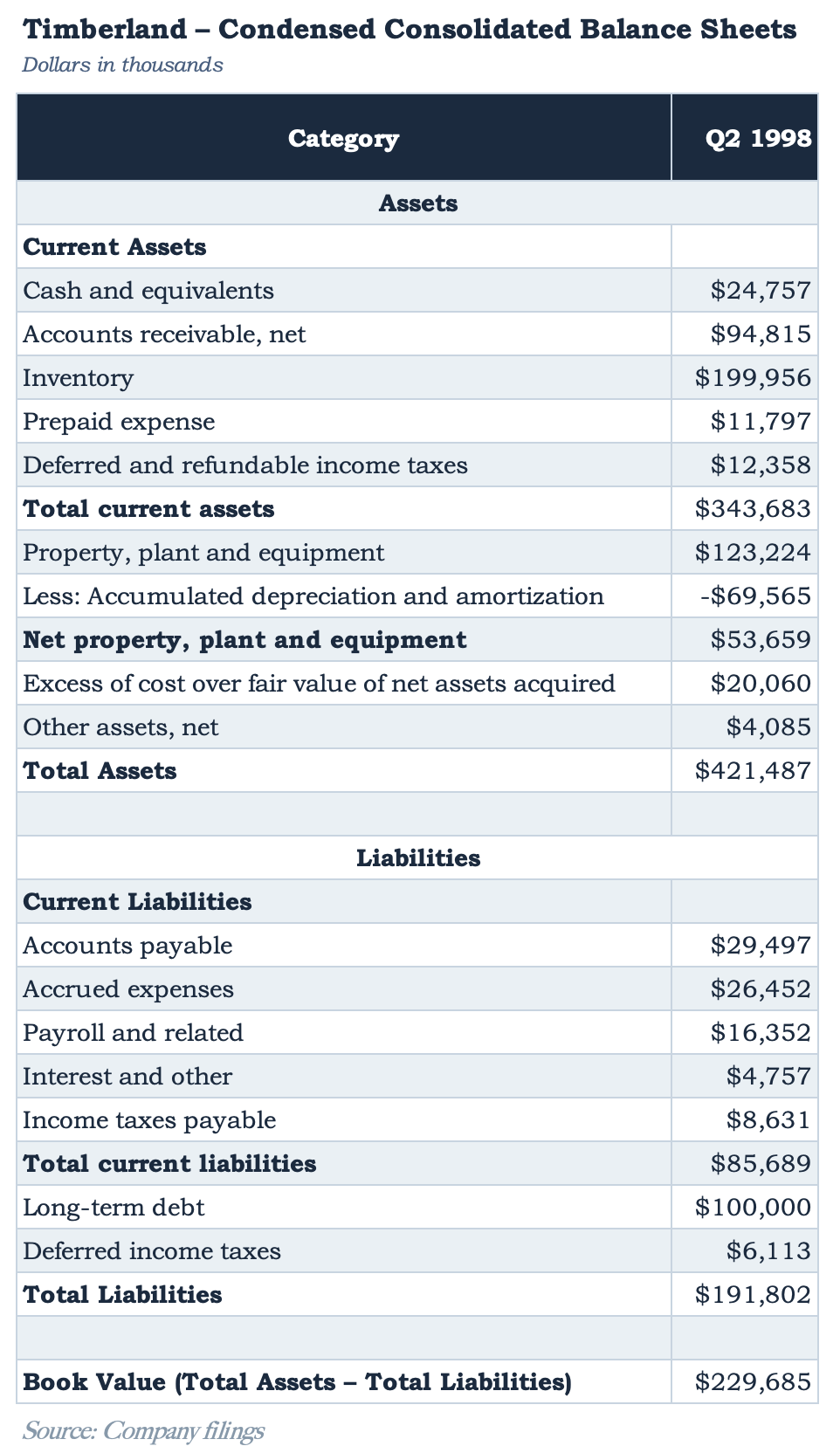

Li also would have had access to the company’s annual report for 1997, which was filed on March 26, 1998, and the two most recent 10Q’s: Q1 1998 was filed on May 7th and Q2 1998 on August 7th.

If Li was looking into the stock in October when the stock price was in the low $30’s or $29 per share range, he would have done some quick calculations to assess how cheap or rich the stock was.

First, at a share price of $29, and with 11,470,423 shares outstanding, Timberland would have had a market cap of $333mn. According to the latest 10Q, the stock had a book value of $229mn. On that basis, the company wasn’t screamingly cheap.

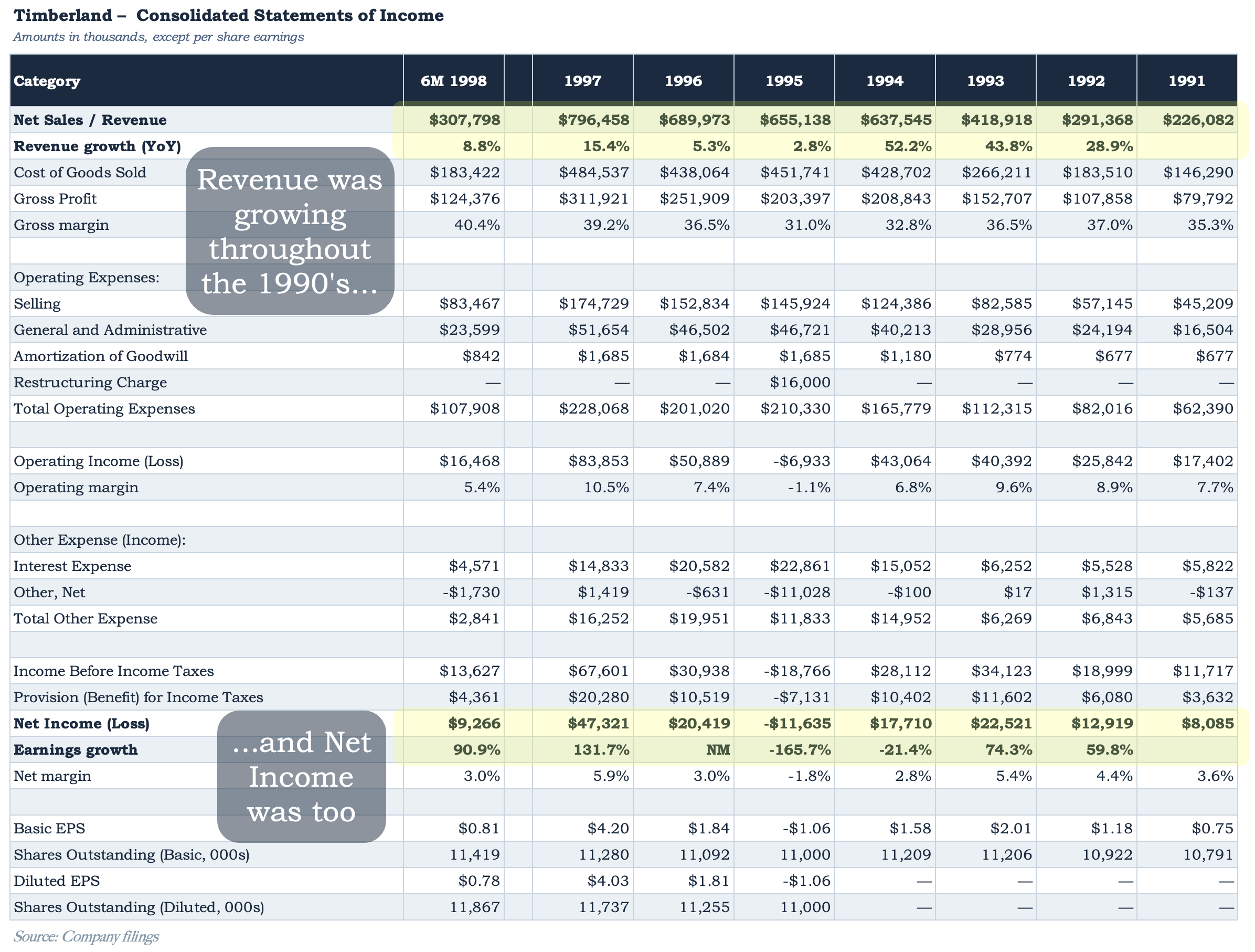

However, the income statement (or the information in the Value Line sheet) tells another story. The Value Line sheet from August 21st shows the company made $4.37 per share in earnings over the trailing twelve months, which, at a stock price of $29, equates to a P/E ratio of 6.6, or an earnings yield of 15%.

And a further look at the history of the income statement from the K’s and Q’s available at the time shows that the company was doing very well. It was consistently growing revenues from much lower levels during the 1990’s, and earnings were growing throughout the period as well. (Note that there was one major exception in 1995, which we will discuss).

The Timberland brand

In the 1990’s, just as today, Timberland boots had a great reputation for quality among tradesmen, like construction workers, carpenters, and factory workers. Although well-known and even iconic today, Timberland’s flagship product of a waterproof, leather boot was somewhat unique at the time of its creation in 1973 and was still leading its niche in 1998.

Moreover, through many years of prior trial-and-error in the shoe industry by its founder, Nathan Swartz, and later by his two sons, Sidney and Herman, the company had captured an even rarer niche starting in the 1970’s and 1980’s, that of a high-quality product loved by craftsmen but also sought after by the affluent layperson. A 1982 article in Inc magazine contains some entertaining evidence that Timberland boots were a status symbol even in the 1970’s:

Kravetz [Timberland’s EVP] was hired early in the summer of 1976. By July, he was tramping up and down Fifth Avenue in New York with a green plaid suitcase stuffed with samples. One day he marched into the shoe department at Bergdorf Goodman and found the manager in his office sipping tea. Kravetz sold him eight pairs of women’s boots and, with that sale, he uncorked a gusher. In the next two years, Kravetz and his remodeled sales team signed up 2,000 new accounts, including a crowd of fancy department stores and an assortment of smaller, upscale retailers.

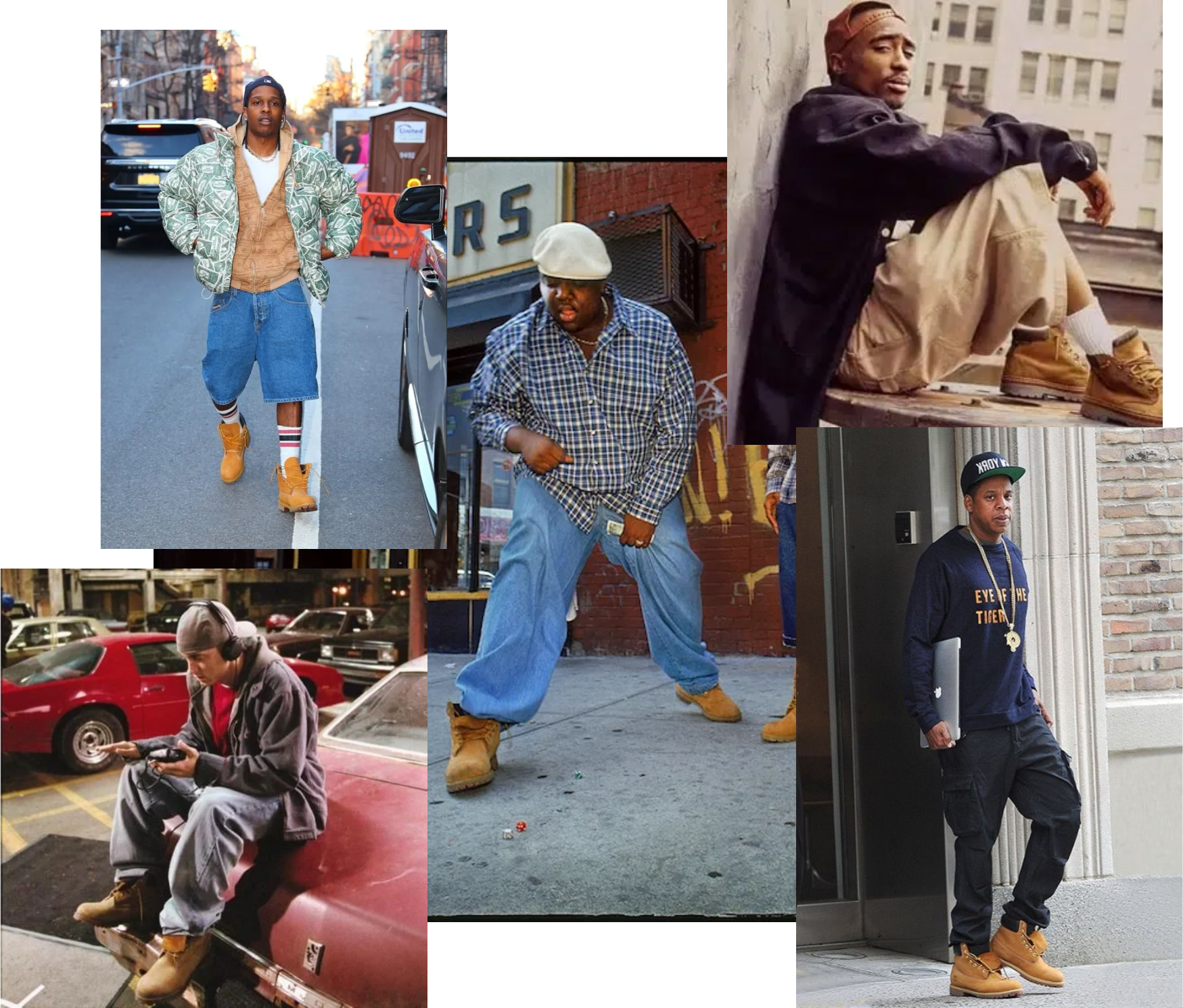

In addition, in the 1990’s, the company was also in the enviable position of seeing their product becoming adopted by even more markets. That period saw the start of a new fashion trend that still continues today. Along with other “outdoor” brands like North Face and Carhartt, hip-hop performers (and their fans) began sporting the company’s boots.

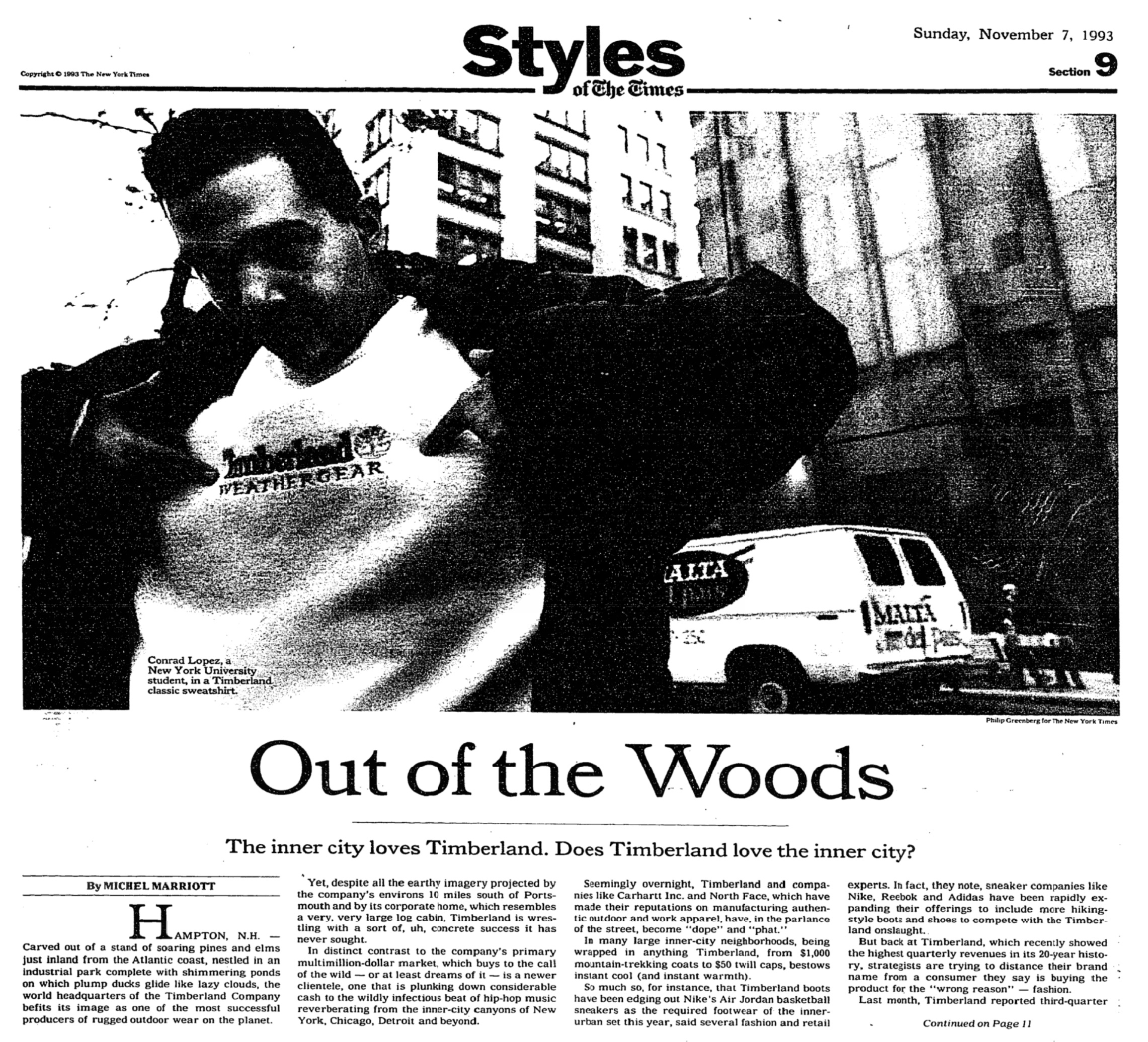

The trend was so prevalent that it even prompted a New York Times article that speculated the company did not realize how popular their boots were becoming.1

And yet, [then-COO Jeffrey Swartz] contended, the urban market constitutes less than 5 percent of the company’s domestic sales... Not so, say some outdoor-wear-for-style devotees, like Julia Chance, the fashion editor for The Source, a national magazine that monthly chronicles hip-hop culture. They say spokesmen for concerns like Carhartt and the C. C. Filson Company are grossly underestimating their sales to young black and Hispanic consumers.

Despite all these positives going for the company, Timberland’s stock was down -55% in just three months, from July 17, 1998 to October 14, 1998. Why the precipitous drop in stock price?

The company had strong revenue growth and good earnings growth over the longer-term and the company’s brand and product continued to be strong. Wasn’t a trailing twelve-month P/E ratio of 6-7 a bit too cheap? Were there any valid reasons for such a dramatic decline?

In Part Two, we’ll conclude the story with the four concerns that were dragging Timberland’s stock down, why Li concluded none of them were fatal, and the unconventional research that gave him the confidence to bet big.

Timberland and other outdoor clothing manufacturers initially attempted to downplay the trend according to the article, on the basis that appealing too much to fashion trends could prove costly if and when the fad faded. Even Jeffrey Swartz, the grandson of the founder, and soon-to-be CEO, seems to have been somewhat neglecting that Timberland was a fashionable status symbol from the start, appealing to the “survival fashion” trend that was popular in the 1970’s. In fact, one could argue that Timberland’s status as a fashion symbol is what enabled it to charge a higher price for its boots and allowed the company to escape the discount retailing problems that had plagued the founders for their entire careers in shoe manufacturing before founding Timberland.

Swartz expressed concern to the New York Times that the hip-hop trend could alienate the blue collar workforce, and the Times article was colored with insinuations of racism, which led Swartz to write a rebuttal in the New York Amsterdam News, “The New York Times again: racism sells - don’t buy it” (15 Jan 1994).

Later on, Timberland would fully embrace the hip-hop trend, creating many special-edition Timbs to appeal to the urban market and partnering with celebrity endorsers.

For readers: adding 1998 Q2's EPS back until 1997 Q3's EPS, you get $4.37/share. Then the Trailing 12-month P/E. Inverse it to get the earnings yield.

This is great content! I very much appreciate you making this available for free to us. I cannot wait to read the rest of your articles.