A Penny on the Dollar: Li Lu's Bet on Russian Privatization, Part 1

The Owner's Memo #10; How the fall of the Soviet Union created once-in-a-lifetime bargains

In 2012, Li Lu gave a rare talk at San Francisco State University, in which he discussed his investment philosophy, some of his practices, and a few brief investing stories.

He mentions a very interesting investment that he made in the 1990’s in at least two Russian companies, during the time the country was emerging from communist rule and undergoing the privatization of its government-owned assets. Li begins with a summary:

As some of you might know, in the early 90’s, Russia went through shock therapy and went into a free market almost overnight. In a short period of time they privatized some of the most prized state assets, including Lukoil and Gazprom... And it was so short [a period of time] that most people didn’t really understand what it was all about. A lot of the people who worked in the companies and also other citizens were given a certificate that they could convert into stock ownership, but most people really didn’t know what it was, so to anybody who came along and offered them real cash [for the certificates], they would just freely give [the certificates] away. As a result, [the certificates], at one point, were trading at extraordinarily low prices...

The price of oil... was 20 dollars per barrel on the open market, [and Lukoil or similar firms were trading at market caps as low as] about 10 to 20 cents per barrel of proven oil on the balance sheet... It was ridiculous. At that point in time, I thought “now that’s a margin of safety”, even considering the political situation in Russia.

The Fall of Communism and the Plan to Privatize Russia

Li is referring to the period of time after the fall of communism in Eastern Europe, stretching from the revolutions of 1989 and the fall of the Berlin Wall on November 9 of that year, to the formal dissolution of the Soviet Union on December 26, 1991.

The revolutions of 1989 saw the adoption of liberal democratic policies, governments, and economic structures across central and eastern Europe in countries like Poland, East Germany, Bulgaria, Czechoslovakia, and Romania. In the Soviet Union, such principles were also taking hold and ultimately led to dramatic changes in 1991.

The more progressive Boris Yeltsin was elected as the first President of Russia in June of that year, and an unsuccessful coup attempt was launched in August against Mikhail Gorbachev, whose policies of glastnost and perestroika were perceived as too progressive for staunch Soviets. After the failed coup, the pace of reform increased, and the final step in the Soviet Union’s dissolution occurred in December when the Supreme Soviet ratified the Belavezha Accords.

During and following these events, Yeltsin and the new Russian government moved rapidly to establish principles and structures around a new economic model for Russia. Among the most important decisions was what to do with the thousands of Russian businesses that had been nationalized ever since the October Revolution of 1917 long ago.

To solve the problem, the State Committee on the Management of State Property (GKI) was created, and Anatoly Chubais was charged with heading it in October 1991. Chubais championed and shepherded Russian privatization from planning to realization, through a very turbulent time for the Russian economy, and the appeasement of a host of stakeholders who each had their own interests, from the politicians to the managers of the businesses themselves to their employees and to ordinary Russian citizens.

Ultimately, Chubais and his team landed on a system of vouchers for privatizing Russian businesses.

The Voucher System

The voucher system worked as follows.

Starting in October 1992, each Russian citizen would be given a paper voucher that could be used, in government-organized auctions, to purchase a portion of a Russian business. 147 million vouchers would be printed, one for each Russian citizen, and distributed until January 1993 via local branches of the State Savings Bank. To obtain the vouchers, a citizen needed only to pay a nominal fee of 25 rubles (equivalent to 10 cents US).

We’ll discuss exactly how a person could turn their voucher into a share in a Russian business later. But first, let’s consider the broad facts and what that meant about the value of Russian companies.

By January, 144 million of the vouchers had been picked up and were circulating in public.

Importantly, the vouchers were freely tradable, which could help poorer Russian citizens monetize their vouchers if they chose to (and many did), and free tradability helped attract larger pools of capital that were needed in privatizing the economy.

Once Russian citizens had their vouchers, they could either hold them and use them at the auctions or they could trade them immediately for cash, typically on the streets of Russia.1 As soon as the vouchers began trading, it was apparent that they were trading for very low prices.

That statement is a critical point in this case study.

Sometimes, in studying the past, we deceive ourselves by oversimplifying the situation or misreporting or misremembering facts. But in the case of Russian privatization, there are a host of reports, some of which I will discuss, that make it clear just how cheap Russian assets were and how it could have been clear even to people with only modest experience in finance and investing. The situation in Russia at the time was enormously complicated, yes, but, in those early days, the discounted prices of businesses was extreme enough to offset tremendous risks.

Russian Vouchers Were Very Cheap

Just how cheap were Russian businesses and assets at the time?

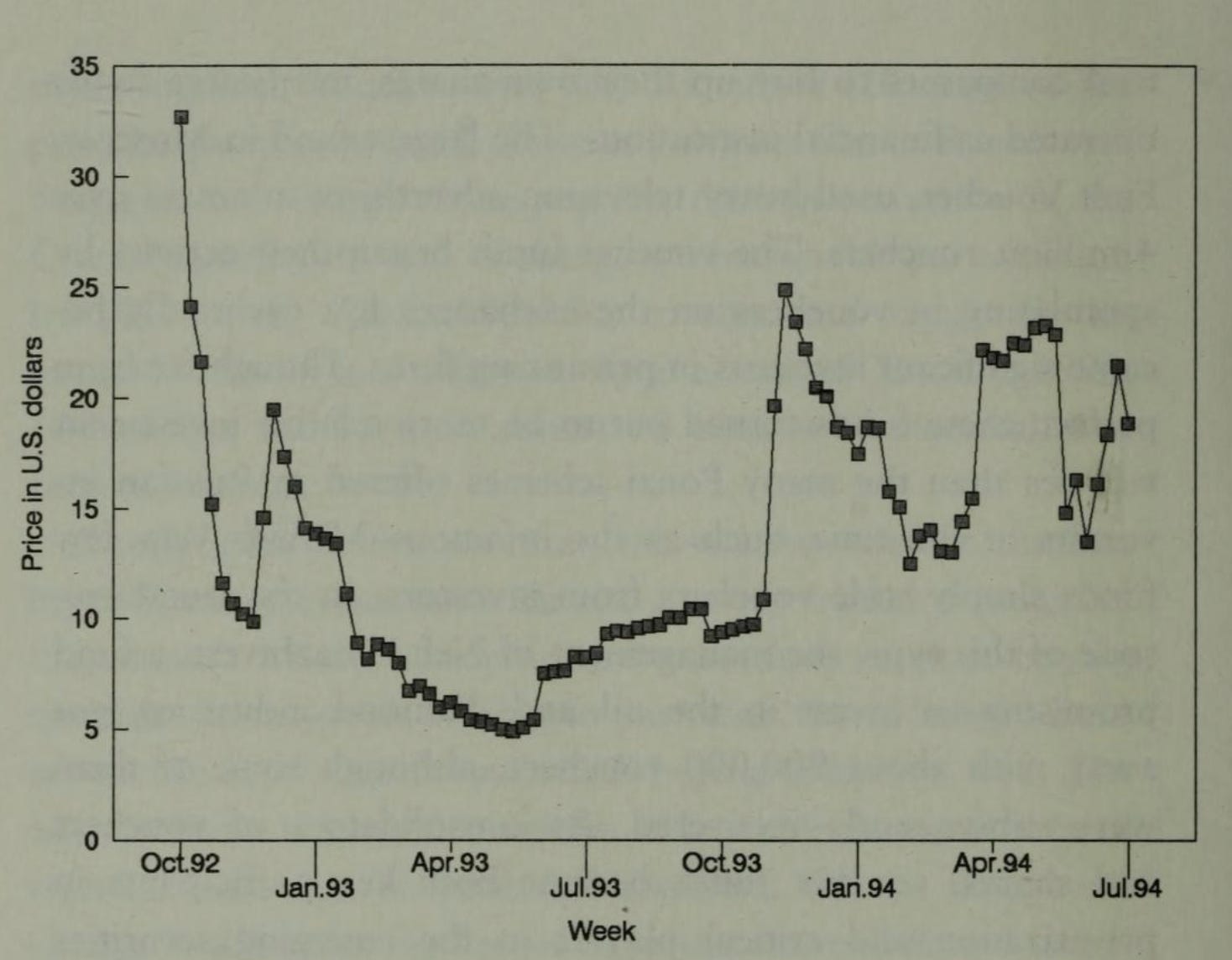

Consider the following chart from the great book Privatizing Russia by Maxim Boycko, Andrei Schleifer, and Robert Vishny, who report the trading price of vouchers from October 1992 to July 1994.2

As the chart shows, from 1992 to 1994, these vouchers were trading on the streets of Russia for anywhere from 5 to 25 USD each.

With some simple work, we can ascertain what these voucher prices implied for the value of Russian businesses, and it is astounding.

144 million privatization vouchers were distributed to Russian citizens. These vouchers were mandated by the government to be converted into the ownership of 29% of all businesses in the country. (In order to garner support for the privatization program, appease the other stakeholders who had control over Russian businesses, the remaining 71% of ownership was to be distributed to company managers and employees and retained by the Russian government. By June 1994, the vouchers accounted for on average 20% ownership of those companies auctioned, not 29%).3

Using a generous value of $20 per voucher, that implies the entirety of Russian businesses was worth $14.4bn at the time (equal to $20 x 144,000,000 vouchers / 20%). As if such an extreme undervaluation needs a comparison, the market cap of Exxon alone, a single US company, at its stock price low in 1993 was $71.7bn.

For another comparison, the market cap of all publicly listed US companies was $5.2tn in 1993.4 So, the opportunity to own Russian privatization vouchers, which would become an ownership stake in one or many Russian businesses, could have been had, between 1992 and 1994, at prices that valued all Russian businesses at 0.28% of all American businesses.

Why Were The Vouchers So Cheap?

Why were the vouchers trading at such incredibly low values? There were several reasons, and I will highlight three of them.

High Russian Inflation

First, inflation was rampant in Russia at that time. Prior to the fall of communism, the prices of many goods and services were set by the state. Starting in 1989 and in a few stages in the years following, Russian leaders slowly freed prices from government control. The effect was a massive inflation that gripped the country in the 1990’s, as shown in the table below.5

Many Russian citizens chose to sell their vouchers after receiving them, which is perhaps not surprising given the level of inflation. The average citizen may have appreciated having any amount of cash now in the face of prices that might be higher the next day.

Vouchers Were Complex for Ordinary Citizens

Second, and perhaps most obviously, the primary owners of the vouchers were ordinary Russian citizens. Now, the voucher auctions were designed to be as simple as possible, to the point where a citizen did not even need to know anything about a company to participate. (So as not to deter the flow of the article, I describe the mechanics of the Russian privatization program and the auction mechanics only in two footnotes below.67)

However, I suspect it is likely that, even with a simple voucher auction design, many citizens simply did not trouble themselves with trying to understand how to bid in the auction process. Moreover, with the Soviet Union recently dissolved, the average citizens’ opinion of Russian government procedure may have been sour. Many probably assumed the voucher auctions would never come to fruition, prompting many citizens to sell the vouchers for cash instead of holding them.

The Vouchers Had A Face Value of 10,000 Rubles

Finally, and for interesting reasons, the vouchers were given a “face value” of 10,000 rubles (approximately 25 USD as of the end of 1992, albeit highly volatile). Why? Boycko, Shleifer, and Vishny8 describe two reasons:

Having a face value printed on the vouchers gave the vouchers the feeling of a monetary gift to the people from the government, and helped create support for the fledgling program.

The denomination of the vouchers in a currency was purposely designed by pro-privatization government officials to make the government commit to the program. Had the vouchers been denominated using points, for example, it would have been easier for a future government committee to cancel the privatization program later on. But since the vouchers felt like real money, canceling or rescinding them would be very difficult.

The apparent effect of that 10,000 ruble face value (again, about 25 USD as of late 1992) on the trading price cannot be overstated.

It inadvertently created an anchor around which the vouchers traded. That anchor served to keep voucher prices low for virtually the entire time they were outstanding through June 1994 and created the opportunity that Li was talking about in Lukoil (and virtually every other Russian business at the time).

Cheap Russian Businesses Attracted Western Investors

The extremely low prices for Russian businesses implied by the voucher prices held sway for a few years and, indeed, throughout virtually the entire time the vouchers auctions were taking place. From December 1992 to June 1994, 15,052 Russian businesses were taken private, in whole or in part, almost all of them at prices that were incredibly low compared to their counterparts in other countries.9

Boycko, Shleifer, and Vishny describe two of the bargains:

VAZ, the auto maker of the popular Lada cars, came out of its auction with a total market value of $45 million. As a point of comparison, in 1991, Fiat reportedly offered the Russian government $2 billion for the company.

Gazprom, the gigantic Russian natural gas monopoly, emerged from its auction with a market value of $228 million. This was roughly 1/1000th the value of put on the company by foreign investment banks, presumably by comparing it to other natural gas companies around the world.

So, in those early years from 1992 to some time in 1994, Russian voucher prices and the market values of companies coming out of auctions and their subsequent traded stock prices were extremely low.

The most active foreign investment bank by far at the time appears to have been Credit Suisse First Boston, in large part through the efforts of its president Hans-Joerg Rudloff, who hired the very active deputy Boris Jordan and his teammate Steven Jennings. The two were exploring privatization opportunities for CSFB in Russia at the time and supporting the Russian government in its efforts. Prior to 1994, foreign interest in Russian privatization and investing was nil:10

Jordan recalled that he had tried, in vain, in March 1993, before Yeltsin won the referendum, to interest foreign investors in the vouchers. “I would go out and tell people about Russia, and no one would let me into their office,” he recalled. “Nobody cared.

Bill Browder was working for Salomon Brothers at the time and suffering from the same disinterest that Jordan at CSFB was:11

“I was running around Salomon Brothers trying to find someone who would listen that this was going to be the most unbelievable investment opportunity there ever was,” [Bill] told me. Eventually, he got permission to invest $25 million, a tiny sum for one of the world’s largest investment houses, but a large commitment for Russia at the time. Browder bought as many vouchers as he could, and then bought shares in little-known companies.

This lack of interest was surprising to foreigners on the ground in 1992 and 1993, but it all started to change in the spring of 1994. Around that time, investing in emerging markets was becoming hot. Also, The Economist published an important article in May of that year, entitled Sale of the Century.12 The article highlighted the cheapness I mentioned above:

For long-term foreign investors prices still look cheap... For instance, shares in Bolshevik Biscuit now cost $53 - three times the price at privatization in 1992. Even at this level, which Russian investors think is dear, Bolshevik’s market capitalization divided by its output of biscuits produces a market-value-per-tonne of $9. Wedel, a (not noticeably crumbier) Polish biscuit maker, is valued by its stockmarket at $850 a tonne.

At the time, the article created a stir, and it caught the attention of foreign investors:13

Right after the Economist article appeared, Browder recalled a flood of interest in Russia among his colleagues in London, who earlier would not give him the time of day. “I was sitting on the trading floor and all of a sudden all the managing directors are around my desk. ‘Bill,’ they said, ‘Interesting stuff you are doing there. Can you get us some Lukoil?’”

Russia Was Cheap But It Was Incredibly Volatile

I mention this turning point in 1994 in the attitudes around foreign investment in Russia because it highlights just how difficult it is to recreate the investment as Li saw it at the time. When Li discusses Lukoil and Gazprom, he doesn’t mention exactly when he made his investment. And Russian equity prices were so volatile in the 1990’s that understanding exactly when an investment was made could change the potential return by several multiples.

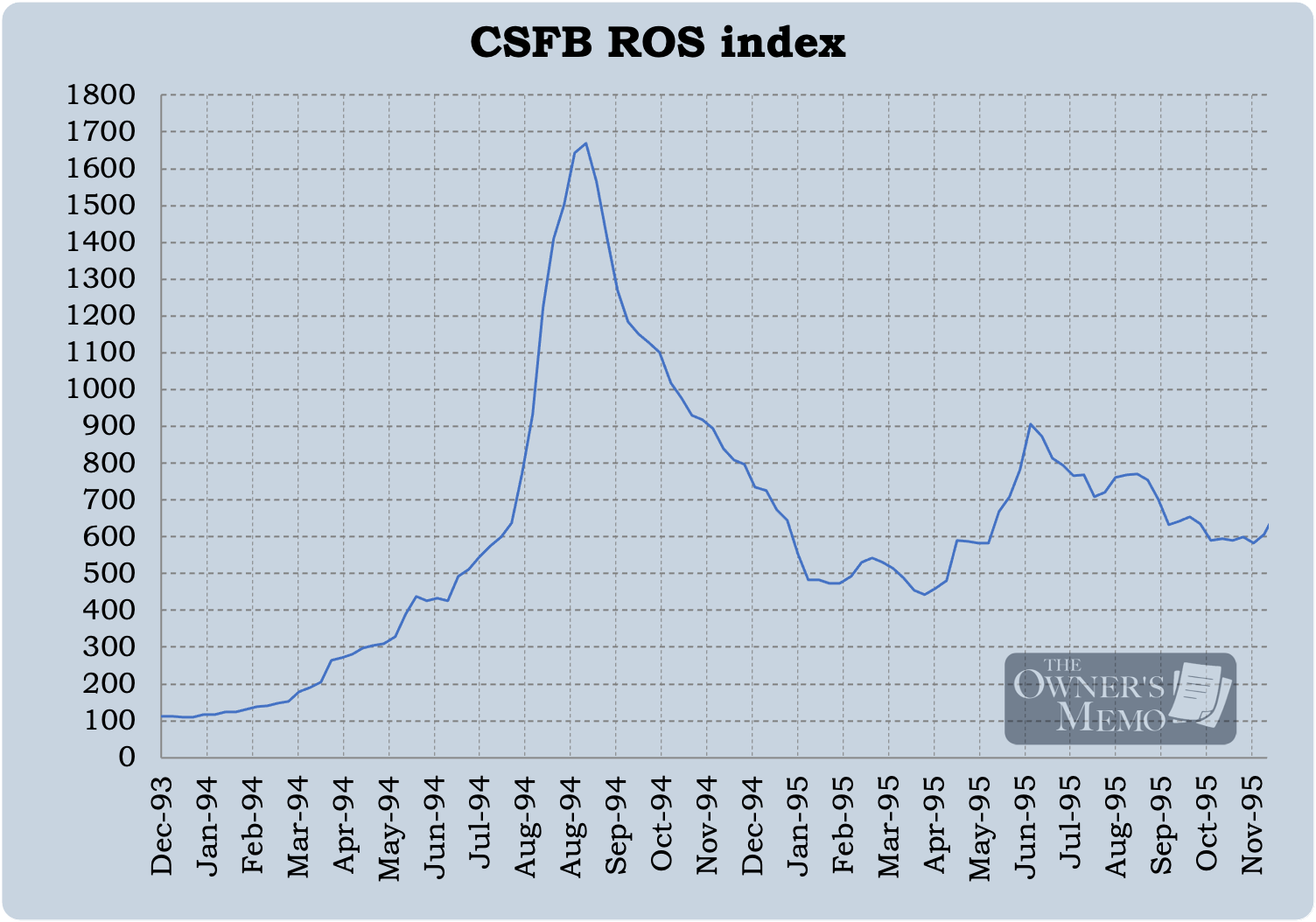

1994, for example, was an incredibly volatile year. The ROS index of 30 Russian stocks (created by CSFB) surged from 116 at the start of the year to a peak of 1,669 in September of that year. Yes, the index was up 1,338% in nine months. That is not a typo. It later dropped to a low of 443 in April 1995.

The End of The Voucher Period and The Start of Russian Stock Trading

So, 1994 was an important year for Russian privatization as an investment. It marks the end of the “voucher period” when Russian vouchers were trading at absurdly low prices and marks the deeper involvement of foreign investors (and the re-pricing and volatility that came with them). It is the time when the price of Russian businesses went from absurdly low to merely very low.

This is important to understand because it makes recreating Li’s exact investment returns virtually impossible. But we can still ascertain what he generally saw in the investment and learn some lessons about extreme opportunities. For example, Li’s commentary in his speech that Lukoil was trading at “10 cents to 20 cents” per barrel of oil reserves on the balance sheet, is consistent with the market cap of the company implied from voucher prices. We’ll see more of this in the next part.

The first period of Russian privatization, of vouchers and voucher auctions, provided astounding opportunities for (very) enterprising investors to invest in Russian businesses at dramatically low prices.

Next week, in Part Two of this case study, we will explore the mid-1990’s period when Russian stocks began trading, we’ll focus on one company in particular (Lukoil) and recreate its market valuations during that period, and we’ll discuss the real risks in investing in Russia at the time.

References

(1) Privatizing Russia by Maxim Boycko, Andrei Schleifer, and Robert Vishny (1995).

(2) The Oligarchs by David Hoffman (2001).

(3) Kremlin Capitalism by Joseph K. Blasi, Maya Kroumova, and Douglas Kruse (1997).

Many sources report a third option for the vouchers: Russian citizens could turn over their vouchers to private voucher investment funds, as a form of investment. This was a popular option: those funds collected 45 million vouchers from Russian citizens. [Reference 1] However, it also revealed the rampant corruption in Russia at the time, and a major risk Li certainly knew about. In July 1994, the market price of one popular fund, MMM-Invest, fell over 99% and was later revealed to be a Ponzi scheme. [Reference 2]

Reference 1, chapter 5, page 102.

Reference 3, page 192.

World Bank Group, https://data.worldbank.org/indicator/CM.MKT.LCAP.CD?locations=US

Reference 3, page 190.

Garnering support for the Russian privatization program in a society coming out of years of communism and entrenched interest was very complicated, and by all accounts in the early years, Chubais did a mostly heroic job. Importantly, the design of the program recognized that (1) the public should receive some stake in the companies as a matter of principle and to garner support for the program, (2) managers and employees also needed to receive an outsized stake because they effectively controlled the companies and also, coming out of communist rule, there was a strong political culture around treating workers well, and (3) the government should also retain some stake in many companies, particularly those in industries deemed politically sensitive, like oil and gas drilling. This last point is debatable, of course, but seemed to have been a necessary political compromised at the time.

The privatization program gave Russian companies and their managers a choice of three options for privatizing. Quoting from the excellent description given in Reference 1:

Option 1 offered workers 25 percent of the shares in their firm for free, but made these shares nonvoting to prevent worker control. Workers could buy an additional 10 percent of the shares at a 30 percent discount from book value, which was set at a very low level, as well as some extra shares for the pension plan. Top managers received 5 percent of the shares at a nominal price. These benefits to the workers and managers far exceeded those offered in any other privatization ever attempted in the world.

Option 2 was the employee-management buy out, which allowed managers and workers together to buy 51 percent of the voting equity at a nominal price of 1.7 times the July 1992 book value of assets. The multiple of 1.7 was said to be based on calculations made by GKI experts, and looked scientific enough to deter critics who demanded individualized revaluations of all Russian companies. The approach worked, and 1.7 was accepted as a reasonable multiple, making assets available to workers at extremely low prices in light of the prevailing inflation rate. Under Option 2, workers could pay for their shares in cash, with vouchers, or with the retained earnings of the firm, and could extend payments over some relatively short period of time. In short, the Parliament offered insiders control over privatized firms.

Option 3 allowed the managers to buy up to 40 percent of the shares at very low prices if they promised not to go bankrupt. (Amazing, right?) Luckily, this option did not go very far. First, a compromise with Chubais restricted the applicability of this option to small firms. And, amusingly, the regulations on Option 3 were written in traditional Russian bureaucratese, which meant that hardly anyone, including the managers, could understand them.

According to Reference 3, “The Russian National Survey of 1994-95 found that option 2 had been chosen by 53.64% of the firms, option 1 by 37.42%, and option 3 by 1.32%; 7.62% of firms had been privatized under the 1991 privatization program, by leasing, later choice of an option (usually option 2), and other means, often special decrees of the government.”

The actual mechanics of the Russian voucher auctions are fascinating, and, once again, Reference 1 gives a great, detailed account. Because of the large amount of businesses to be privatize, Russia chose a decentralized auction process rather than a centralized one, and made the privatization process voluntary (and with incentives of course as shown above). The auctions needed to be as simple as possible so public officials can run them and Russian citizens might be encouraged to participate, they needed to designed in such a way that citizens might be able to bid without knowing much about the companies, they must allow citizen-investors to succeed in getting shares once they bid (and not feeling shut out of the process), and they must allow citizens to pay the same price as professionals.

To account for all these needs, a simple auction procedure was designed. Any investor who wanted to purchase shares in a company simply needed to show up at the auction and submit his voucher as a bid for the company’s shares. At the end, the total number of vouchers is added up and the shares that were offered by the company are distributed pro-rata in proportion to all the vouchers submitted. For example, if the company offers 10,000 shares for auction, and 500 vouchers are submitted, then each voucher buys 20 shares. If 20,000 vouchers are submitted, on the other hand, each voucher buys 1/2 a share.

Reference 1, chapter 4, page 86.

Reference 3, page 192.

Reference 2, chapter 8.

Ibid.

The article appears to have been so popular that it inspired a second article with the same title in The Economist the following year, 1995. Although a reprint of the article does not list an author, it seems highly likely that the author was Chrystia Freeland, who later wrote the excellent book with, again, the same title, published in the year 2000, that chronicles the broader period of privatization in Russia and the people involved. In more recent years, Freeland has become a prominent Canadian politician, and, as of 2025, serves as the country’s Minister of Transport and Internal Trade.

Reference 2, chapter 8.