A Penny on the Dollar: Li Lu's Bet on Russian Privatization, Part 2

The Owner's Memo #11; Seeing just how cheap Lukoil was versus Exxon, and the risks present in investing in Russia at the time

In Part One of our case study of Li Lu’s investment in Russia, we discussed the the fall of communism, the government plan to privatize Russian businesses, and the voucher system that was used to convey interests in those businesses to private citizens.

Now, I would like to focus on one of the two companies mentioned by Li to try to get a more specific sense of what he saw at the time. That company is Lukoil. A good part of this case study will be focused on attempting to recreate basic information from the time, like Lukoil equity pricing and company fundamentals, since it is very difficult to get any good information about Russian stocks from that period.

The History of Lukoil and Early Information Advantages

Lukoil was formed in 1991 with the merger of three companies, the Langepas Oil Company, Urai, and Kogalym (the “Luk” in Lukoil)1, and in November 1992, Boris Yeltsin officially designated Lukoil one of three integrated holding companies2. In those early days of the company’s formation and Russian market privatization, the trading of stocks was in its infancy and systems were rudimentary:3

The new network faced one major problem at the outset: existing telephone lines were so bad that they could not communicate with one another at reasonable speed...

By mid-1995 only a dozen exchanges handled equities at all, and the volumes traded were small - between $600,000 and $3 million per week country-wide.

The lack of good trading infrastructure is relevant for our case study today. Early trading prices for Lukoil are not available in any records I checked, which may be due to the disorganized nature of trading in those days. The first trading price I was able to find for the stock was January 12, 1996 from Bloomberg.

The same goes for information about company financials or any supplemental information. In fact, it was so difficult to obtain basic information about Russian companies in the early 90’s that it was cited by some investors as a distinct advantage. From David Hoffman’s The Oligarchs:4

Browder had an advantage. He knew an oil trader in Moscow who had rudimentary information about the companies that were being privatized, especially in oil. “At the time, just knowing the names of the companies and roughly what the production and reserves were was huge, valuable information,” Browder recalled. He had the facts on a spreadsheet but was careful not to show it to anyone. He had the first crack at the best investments, since everyone else was in the dark.

The earliest annual report I was able to find for Lukoil was from the year 1996. It is from that report that I obtained the total for the company’s share count and for the company’s proven oil reserves that I will use in the analysis below.

Do The Legwork Others Won’t

The lack of financial and pricing information available raises a critical point about Li’s investment in Lukoil: it shows what it takes to invest well.

In the early and mid 1990’s, Li Lu was a student at Columbia University. If simply finding information about Russian companies was as difficult as it seems, especially for a student in New York like Li, it speaks to the extreme level of dedication and commitment he must have had in pursuing an investment like this.

Some very interesting and compelling investment opportunities come with the need to do “frontier”-type of work. (See also Li’s willingness in his investment in Timberland to travel to the hometown synagogue of the managing family to get to know them.) In the case of Lukoil, Li would have needed to figure out how to simply obtain basic information about the company and also how to execute a purchase of Lukoil’s stock.5

Recreating Lukoil’s Market Price History

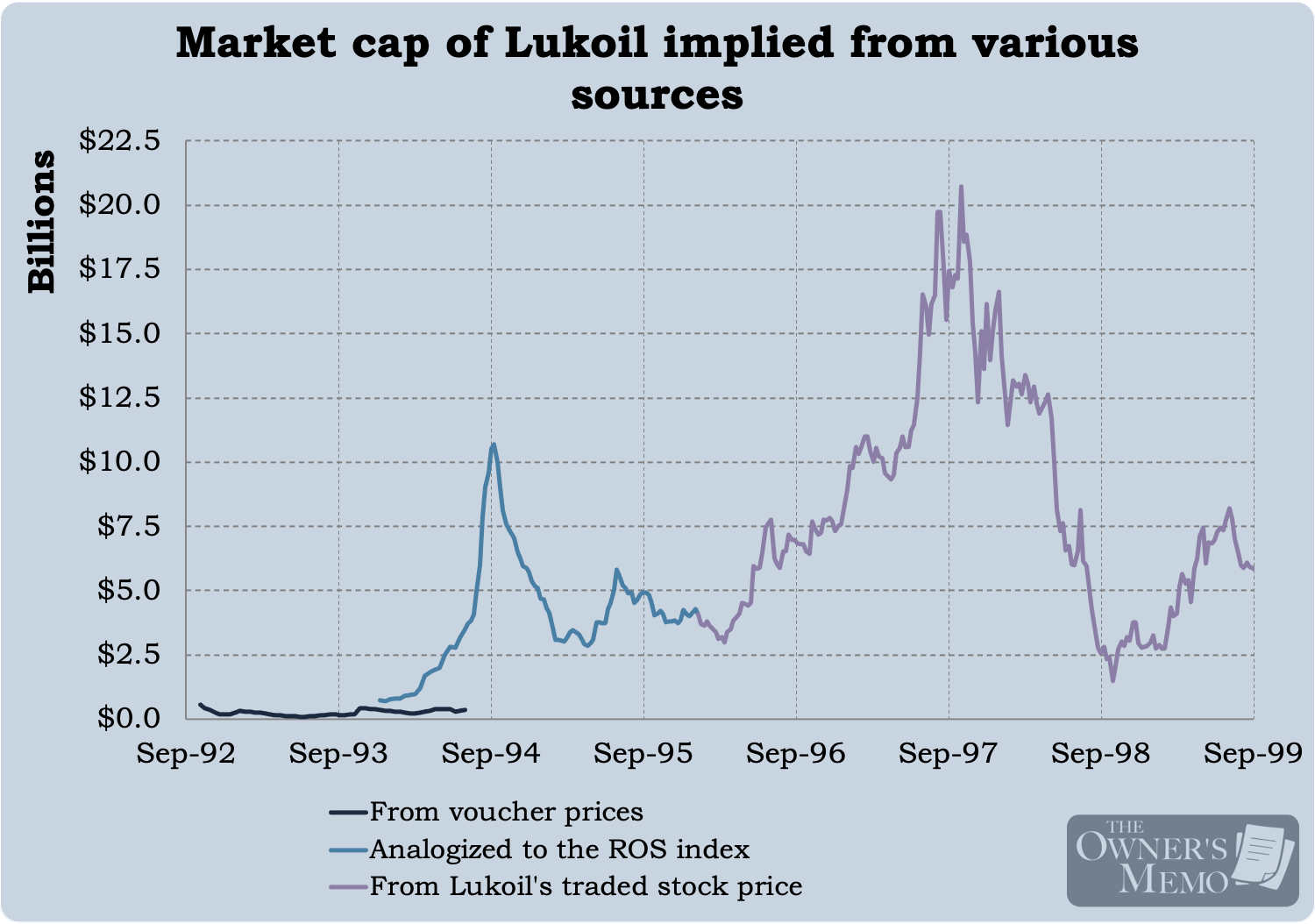

Let’s imagine what Li might have seen in those early years of Lukoil’s formation and trading, recreating the company’s market cap and market price from those years, even if we can only do so crudely.

Since the first trading price of the stock I was able to find was January 12, 1996, I will stitch together an effective “Lukoil market price” for the stock prior to that date from a few data sources. It won’t exactly match the pricing traded by Russian stockbrokers from those early years, but it should be close enough for us to see how this investment unfolded.

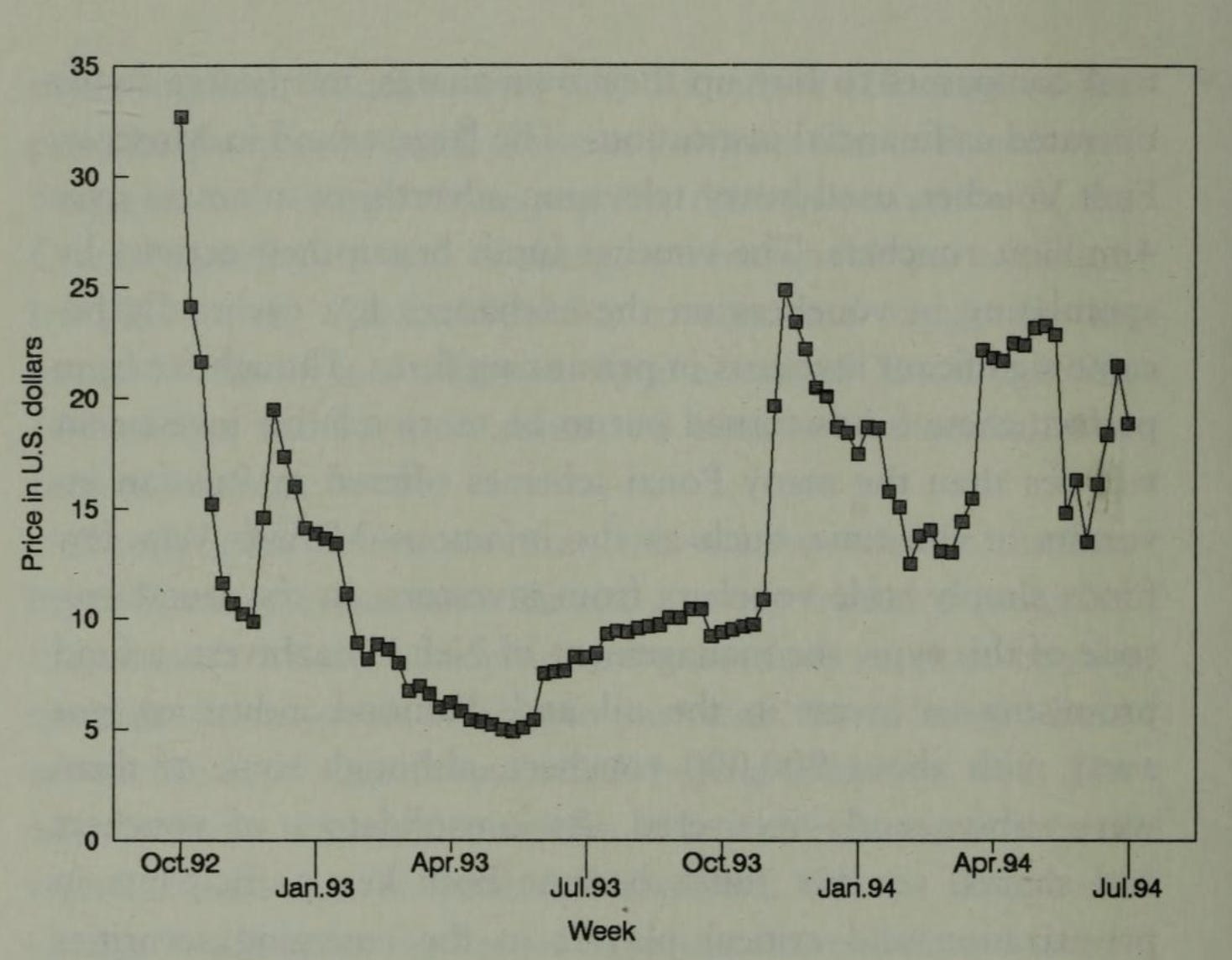

From 1992 to December 1993, I used the pricing for vouchers we saw in Part One of this article. That figure is reproduced below. However, I could find no information about the outcome or pricing of Lukoil’s first privatization auction in April 1994.

But some sources did report the results of the Gazprom auction as valuing the entire company at $228mn. Gazprom’s auction took place between April 1994 and June 1, 19946. And just a few years later, in 1996, Gazprom was trading at $1.775bn of market cap (versus $3.073bn for Lukoil)7.

In determining the effective “voucher-price” of Lukoil, I used the assumption that Lukoil’s market cap coming out of auction was equal to the same ratio of 1.73 times that of Gazprom. It is very crude, and it shouldn’t be relied on for anything more than what we are doing here: trying to get a feel for roughly how this investment opportunity progressed in the early 90’s.

Credit Suisse created and maintained a valuable index of the Russian stock market called the ROS index, which tracked 30 Russian stocks (one of which was Lukoil). From December 1993 to January 1996, I make the assumption that Lukoil’s stock price tracks the ROS index exactly. This assumption is crude too, but the correlation between the two after 1996 is very high, so, again, this recreation should give a pretty good feel for what Lukoil’s stock price was doing during this period.

From January 1996 onward, I use Lukoil’s stock price from Bloomberg.

Finally, I am going to make two more crude assumptions.

Lukoil’s oil reserves. In his talk, Li does not discuss the earnings of Lukoil at all. In fact, he only mentions one metric that indicated how severely undervalued Lukoil was at the time: the number of barrels of proven oil reserves on the company’s balance sheet.

Finding this figure was difficult, but I was able to discover one annual report of the company’s from those early years, the annual report for 1996. In that report, the company lists its total proven oil reserves in Russia as 10.5 billion barrels of oil and 2.150 trillion cubic feet of natural gas8, for a total of 10.9 billion barrels of oil equivalent. While these reserves will change each year as the company taps those reserves and discovers new reserves, we will use it through 1998 as a fixed value in order to recreate the metric Li spoke about. I was able to find annual reports from 1998 onwards, so any reserve figures from those years will be accurate.

Lukoil’s share count. In the same vein, I could find no sources that gave specific share counts for Lukoil’s common stock in the early years. So, I use the total from the 1996 annual report (714,563,255 total shares), assume that figure is fixed through 1998, and use it to calculate Lukoil’s market cap from its stock price.9 Again, I was able to find annual reports from 1998 onwards and have used share count figures for those years.

With the details out of the way, here is my recreated chart of Lukoil’s stock price (or its voucher-equivalent) from 1992 to 1999, made from the above data sources.10

The chart above makes the extreme undervaluation of Lukoil plain in absolute terms. To further drive home just how cheap Lukoil was relative to the rest of the world, consider how it stacked up against a major Western peer.

Lukoil versus Exxon

Lukoil was cheap in those days, but how cheap was it? Let’s take a look at the valuation of Lukoil versus that of another leading oil company at the time, Exxon.

While Lukoil’s trading prices implied a market cap of 20 cents to 50 cents per barrel of proven oil and gas reserves around the time of Li’s purchase, Exxon’s valuation implied a market cap around $6 to $8 per barrel. In other words, Lukoil was trading about 5% the value of Exxon on a reserve basis ($0.35 divided by $7). At the time, the price per barrel of crude oil on world markets was around $20.

Seeing the market cap of Lukoil at such a big discount from the market price of oil during that period (and versus other oil and gas companies as well) makes an investment in the company seem like a no-brainer. And according to Li’s comments in his speech, at the time, he regarded it as such.

But it is impossible to go back in time and truly recreate how any of us would have reacted at the time. To further explore that, let’s discuss the arguments against an investment in Lukoil.

Giving Weight to Arguments Against Russian Investments

To avoid looking at the past through rose-colored glasses, let’s explore some of the arguments against Russian stocks at the time.

Argument #1: Russian companies needed too much capital

At the time of Li’s investment, in the early 1990’s, Russia was still recovering from the collapse of communism, and it was widely thought that Russian companies needed a lot of capital to modernize after underinvestment in the years prior.11

How much capital investment is necessary to modernize all 18,000 privatized corporations? When estimates by top managers in the Russian National Survey in 1995 are telescoped to all privatized corporations, the amount is between $150 and $300 billion.

Moreover, these concerns seemed to be more than just academic. In fact, Russian oil production was suffering declines in the early 1990’s:12

Annual production declines, which had been in the double digits in 1991-1993, slowed in 1994, and by 1995-1996 were only between 2 and 3 percent. By the end of 1996, the decline in crude output had bottomed out. Russia in 1996 produced only half as much oil as in 1987, its peak year in the Soviet Union, and oil investment stood at less than one-third, but there was now hope that the worst had passed and that the sector was poised for recovery.

Argument #2: Rampant inflation

Another argument against any equity investment in Russia was that inflation was rampant in the country at that time. I spoke about this in Part One of this article. Prior to the fall of communism, the prices of many goods and services were set by the state. Starting in 1989 and in a few stages in the years following, Russian leaders slowly freed prices from government control. The effect was a massive inflation that gripped the country in the 1990’s, as shown in the table below.13

For me, this argument is an easier one to rectify than the first. Here, I’m reminded of Mohnish Pabrai’s investment in the Turkish company Reysas in 2019. Reysas owns warehouses in Turkey that are leased to large multi-national corporations.

At the time, Pabrai was concerned about the rampant inflation (both current and future) in Turkey, but rightly reasoned that a company that controls valuable and irreplaceable assets as part of its business should be able to raise prices to keep pace with inflation (or better). He was right, and, for Li’s investment, Lukoil’s proven oil reserves have a similar aspect.

Argument #3: Rampant corruption

This one is easy for a Westerner to understand today, and it is difficult to rectify. At the time, and despite its moving toward more democratic politics, Russia had a reputation for corruption. Perhaps nowhere was this more evident than in the “loans for shares” scandals that pervaded Russia’s privatization charge.14

One day in late summer of 1995, as they were talking, Kokh asked Ryan casually, “What do you think about Uneximbank and Menatep?”

Ryan discovered that Kokh was working on a privatization deal that would change Russian capitalism and politics forever. On his desk was a scheme in which Russia would give away its industrial crown jewels-the most lucrative oil companies and richest metal mines —to a coterie of tycoons, all of them from the Sparrow Hills club. Vladimir Potanin of Uneximbank was first in line, followed by Mikhail Khodorkovsky of Menatep. From the beginning, Kokh had handpicked the winners, Ryan recalled. According to the plan, shares in the factories were to be given to the tycoons for safekeeping, in exchange for a loan to the government. Everyone knew the deficit-ridden government would not repay the loan. Then the tycoons would sell the shares, as repayment of the loans. But there was a twist. The tycoons would probably sell the shares to themselves, very cheaply, through hidden offshore companies. That way, they would get the valuable assets for next to nothing. It looked to Ryan suspiciously like a backdoor giveaway, a loan to the government in exchange for colossal oil and mineral riches. The scheme was called “loans for shares,” and Ryan told Kokh: “This loans for shares thing really stinks.”

The loans for shares program was emblematic of how much corruption was at play in Russia at the time, and the scheme helped fuel the subsequent rise of the Russian oligarchs. To give a more concrete feel for some of the undervaluations that resulted from the scheme, 5% of Lukoil was sold in these schemes for $35mn to $45mn, when the value for 5% of the company that was implied from stock market trades was $180mn.

Argument #4: Russia was cheap, and it should have been.

This argument goes along with #3: There is good reason for the cheapness of Russian stocks. Corruption puts the rule of law at risk, particularly property laws around equity ownership. As in the loans for shares deal, there was no guarantee that further portions of Lukoil wouldn’t be sold for large discounts, effectively diluting existing owners and raising their (per barrel) cost of ownership. Moreover, investing as a Westerner in a country that just came out of a Cold War with the US would have raised serious questions about the risk of the Russian government being antagonistic toward Western ownership.

Next week, in Part Three, the final installment of our case study, we’ll see how Li weighed these arguments, what he ultimately decided, and piece together his investment and just how lucrative it was.

References

Capitalism Russian-Style by Thane Gustafson (1999)

Wheel of Fortune by Thane Gustafson (2012)

Kremlin Capitalism by Joseph K. Blasi, Maya Kroumova, and Douglas Kruse (1997).

The Oligarchs by David Hoffman (2001).

Reference 1, chapter 5, page 108 and 126.

Reference 2, chapter 2, page 76.

Reference 1, chapter 3, page 67.

Reference 4, chapter 8.

One additional note. Because I am using facts from a 1996 annual report, one could argue that I am not using facts relevant to any investment made before that time. But the opportunity available in Lukoil (and other Russian companies) was so extreme, that, as long as one could somehow find information on Lukoil fundamentals, like share count and oil reserves, the exact numbers (whether from 1994 or 1995 or 1996) did not matter so much as simply having a rough idea of them.

[19] “Russia’s Gazprom starts share sell-off”, April 25, 1994. https://www.upi.com/Archives/1994/04/25/Russias-Gazprom-starts-share-sell-off/5130767246400/ph

Reference 3, page 197.

“Taking into account the audit of the Company’s Western Siberian reserves carried out by Miller and Lents in 1995, LUKOIL total proven oil reserves in Russia exceed 10.5 billion barrels and 2,150 billion cubic feet of gas. LUKOIL has the largest proven oil reserves among the world’s private oil companies.” Since the value of Lukoil’s gas reserves at the time was only about 2-3% of its oil reserves, we will ignore its gas reserves for the case study.

The annual report lists 649,551,391 common shares and 65,011,864 preferred shares, with a market price lower for the preferred than the common shares. For the sake of simplicity, I will use the total share count and assume the price of both shares is equal to the price of the common stock.

There is one immediate and glaring issue with the pricing shown above: the market cap implied for Lukoil from voucher prices (blue line) is much lower than that implied or reflected in the ROS index (green line), which tracked the trading of actual stocks. But there are two reasons to believe the discrepancy may be real or at least not totally wrong.

First, the vouchers were somewhat difficult to obtain, especially by foreigners, since they don’t seem to have been easily tradable. One could obtain them easily, of course, on the streets of Russia, but that doesn’t do much good for, say, investors around the world who want to invest in Russian businesses. Such a restriction on demand may have resulted in lower voucher prices when compared to comparable equity securities.

Second, prices in the Russian stock market really took off in the spring and summer of 1994, and June 30, 1994 was the last date that vouchers could have been turned in for company stock. As a result, and with the opportunity to use the vouchers expiring, it is reasonable that the traded prices of vouchers did not keep up with the traded prices of Russian stocks.

Reference 3, page 178.

Reference 2, Chapter 2, page 94.

Reference 3, page 190.

Reference 4, chapter 12.