Li Lu’s 7x Return on Timberland, Part 2

The Owner's Memo #4

Part One of this story was published in The Owner’s Memo #3.

Part Three is available as well in The Owner’s Memo #5.

Yesterday, we discussed how Li Lu first discovered Timberland in the fall of 1998 when it was trading at a P/E ratio of 6.6. Some thorough research revealed that the company had a beloved brand and growing revenues, and yet the stock had fallen -55% in three months.

Why was it so cheap?

Today, we’ll discuss the four concerns that were an overhang for the stock, what Li’s research made of each, and the remarkable scuttlebutt that gave him the conviction to act.

The concerns about Timberland

Despite the good reputation that Timberland had among its customers, there were a few big issues that seemed to be dragging down the company and its stock in 1998.

A thorough search of company filings and news articles from the 1990’s revealed four major concerns. Understanding whether or not Timberland was a bargain at the time would have hinged on deeply understanding these issues and whether or not they were harbingers of poor performance to come.

Let’s discuss each of them.

Concern #1: The Asian Financial Crisis

In his talk, Li Lu cites one reason for the drop in price, the Asian Financial Crisis, but he also goes on to say how ridiculous such a reason was. Timberland only had 4.3% of its sales from markets outside the US and Europe according to its 1998 second quarter 10-Q, so a weaker Asian consumer would not have a meaningful impact.

Now, a thorough reading of company reports does show more exposure to Asia than simply a low sales number. In the early 90’s, the company began outsourcing its manufacturing to foreign manufacturers. By the end of 1997, Timberland had 37% of product manufacturing in Asia, up from 21% for all international manufacturing in 1993:

The Company also continued to shift production of its footwear products to third party manufacturers... Approximately 27% [and] 10%... of the Company’s 1997 footwear unit volume was produced by [two] independent manufacturers located in China [and] Thailand. Source: Timberland 1997 10-K.

So, the Asian Financial Crisis could have affected the company’s manufacturers, but that reasoning alone doesn’t seem plausible enough to justify such a low valuation. After all, the speed with which the company shifted manufacturing over four years from in-house to third-parties suggests that a similar shift away from certain third-parties, if necessary, could be undertaken again with more ease.

But a more thorough investigation of the market at the time shows that the Asian Financial Crisis was likely not the reason for the stock’s precipitous decline. The bigger reasons appear to have been three other large concerns.

Some of these were discussed by Li and some were not.

Concern #2: A struggling retail shoe industry

Li does not mention in his talk one of the issues that seemed to be depressing shoe company stocks at the time, an industry facing lower-than-expected sales. Indeed, the commentary from the August 21st Value Line sheet says as much:

Timberland shares have fallen by over 25% in price since our May report. We believe that the primary reasons for the decline are that the second-quarter sales increase was lower than expected (though earnings exceeded Wall Street’s estimate), and that shoe companies’ stocks, as a whole, are being pummeled in response to sluggish demand in the industry.

And the following is from a Wall Street Journal article from 1999 describing the sentiment in the 1998 period:

Last year was indeed a struggle for the shoe industry, as the market was flooded with cheap close-outs from the shutdown of Kinney Shoes by Venator Group, the successor to Woolworth that has reorganized its shoe-retailing businesses.

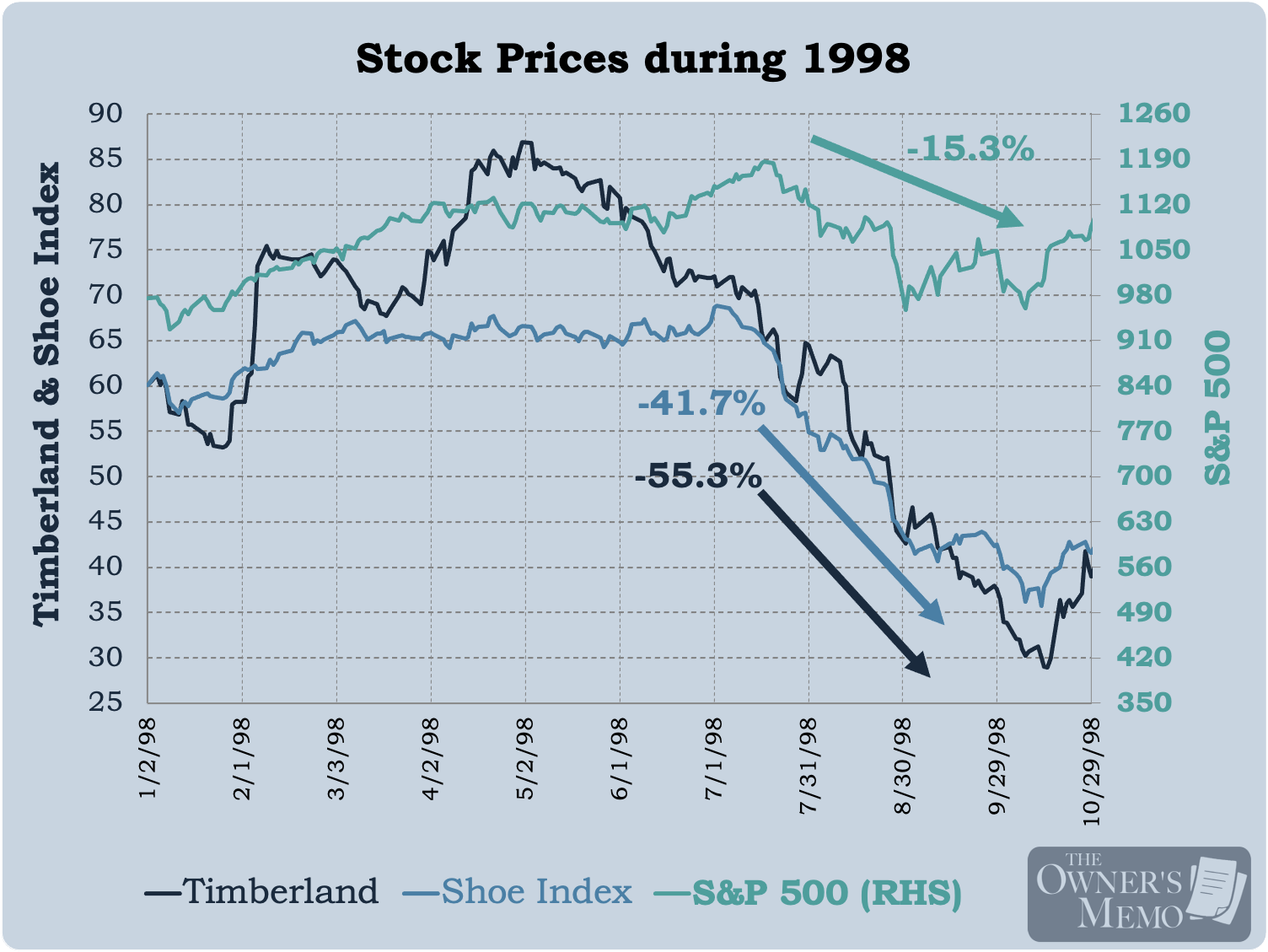

There were several other public stocks at the time that could be classified as “retail shoe” companies, among them Brown Group, Deckers, Foot Locker, Nike, Nine West, Payless, Reebok, RG Barry, Stride Rite, and Wolverine World Wide. I created an equal-weighted index of these stocks using historical prices, and that index would have been down -41.7% from July 17, 1998 to October 14, 1998, in contrast with the S&P 500 which was down -15.3%. Timberland, as I mentioned earlier, was down -55% over that time.

But digging deeper into the concerns at the time shows that much of the anxiety was centered around athletic shoes. Another article from the New York Times highlights the distress among makers in that subsector:

For the quarter ended March 31, Fila’s parent company lost $8.7 million. When Nike posted a $67.7 million loss last month, its first quarterly loss in 13 years, Phil Knight, the company’s chairman, said, ‘’It was not a good year by Nike standards, but then our futures aren’t very good either.’‘ Nike’s Asian business is in turmoil, and it is laying off 1,600 workers. Reebok lost $3.4 million in its first quarter ended March 31. Converse reported that sales of its basketball line tumbled 50 percent in its first quarter, which also ended March 31.

But Timberland, on the other hand, is cited as a bright spot in the struggling shoe industry:

Some companies and analysts say they believe consumers are shifting their tastes to the so-called brown shoes, footwear made by outfits like Doc Martens and Timberland.

In fact, the trends we saw earlier in company revenues reinforce that Timberland was doing relatively well in this period of stress. Timberland’s Q2 1998 revenue was up 9.5% from the year prior, compared to Nike’s which was down -2.8%.

Yet, despite this relative (and outright) strength, Timberland’s stock was down -55% over the period mentioned above, while Nike was down only -22%.

Concerns about a “struggling shoe industry”, in fact, seemed overextended to Timberland, whose fundamentals stood in contrast to other companies that saw revenues and earnings actually falling.

Concern #3: The shareholder lawsuit

In his talk, Li discusses that there were “a whole bunch of lawsuits” against the company that could have caused concern for investors at the time. He also mentions how important it is to do the legwork and “download every single... document from the court cases“ and read them.

A search of legal filings against Timberland from 1992 through 1998 revealed just one major lawsuit against the company (and two minor ones related to a distributor-manufacturer disagreement and the selling of counterfeit Timberland products). That major lawsuit, Schaffer v. Timberland Co., was a consolidation of two separate suits and was not hard to find, as it is mentioned directly in the company’s 1997 annual report:

The Company and two of its officers and directors were named as defendants in two actions filed in the United States District Court for the District of New Hampshire, one filed by Jerrold Schaffer on December 12, 1994 and the other filed by Gershon Kreuser on January 4, 1995. On April 24, 1995, the District Court granted plaintiffs’ motion, assented to by defendants, to consolidate the two actions.

In the lawsuit, two investors in Timberland stock sought to charge the management team with a violation of SEC Rule 10b-5 due to the severe drop in Timberland’s stock price from May 12, 1994 to December 9, 1994, when the stock dropped roughly -36%.

What does this mean? SEC Rule 10b-5 is very brief, and it can be found here. It is a broad rule preventing anyone engaged in securities practices from committing fraud, making untrue material statements, or omitting material facts.

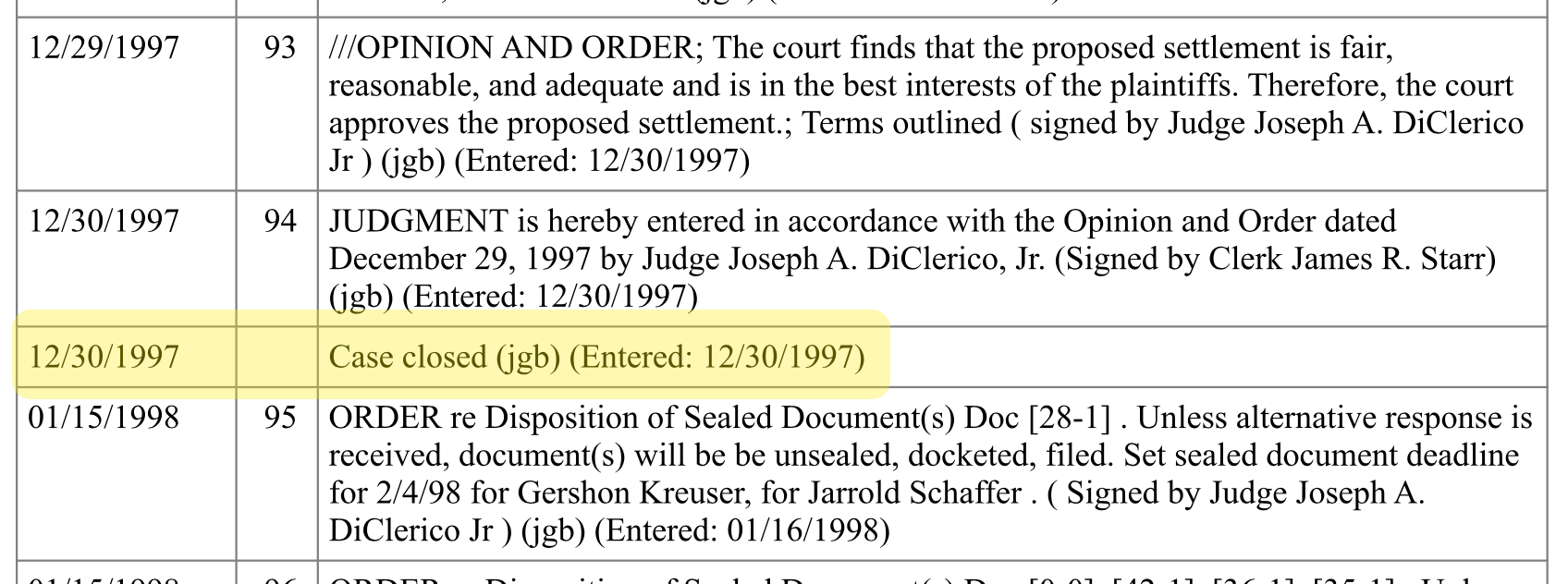

While the lawsuit seems concerning on its face, the 10-K also reveals a simple and critical piece of information: the lawsuit had been settled as of December 1997 / January 1998, ten months before Li was considering an investment. The docket for the case also reinforces that fact.

On December 29, 1997, the District Court entered an order granting final approval of the Stipulation. Under the terms of the Stipulation, the settlement of this litigation was final and effective on January 29, 1998. The settlement of this litigation did not have a material adverse effect on the Company’s financial position, results of operations or cash flows. Source: Timberland 1997 10-K

This is a critical piece of information for an investor in Timberland at the time, and it’s one that Li neglected to mention in his talk. Li would have known in October 1998 that the case would not have significant financial impact on the company.

However, although the case was settled, Li was still concerned about the lawsuit. Specifically, because of the nature of the case, he wanted to be sure that the management team was not a group of corporate fraudsters. We’ll discuss below the novel way in which he tackled that issue, with a personal visit to the management team’s home town.

Concern #4: The earnings decline in 1995 and the charge of incompetent management

During the talk, Professor Bruce Greenwald of Columbia Business School asks Li if he had any concern about “what happened between 1994 and 1996”, apparently referring to the company’s reporting negative income in 1995. Li mentions that the decline was due to poor marketing at the company around waterproofed versus non-waterproofed shoes and a hit to reputation and margins that resulted, but he doesn’t address the concern further.

The company’s disclosures from the period don’t say much about the marketing mishap, except for a brief line in the 1995 10-K about expanding its creative staff to better manage its brand.1 But I discovered that there were more issues in the 1995 period than the waterproofing issue alone.

1995 issue #1: A big restructuring at the company

In the 1995 period and earlier, Timberland suffered from the critique that their net margins were too low for a retailer of high-quality, desirable apparel. From a scathing article in CNN Money in May 1995 titled Will Timberland Grow Up?:

For all the brand’s strength and to-the-moon growth, the company has barely enough profit to fill a mukluk... a net margin of 3.9% - terrific for an A&P, but terrible for a worldwide superbrand. Nike, for instance, nets 8%.

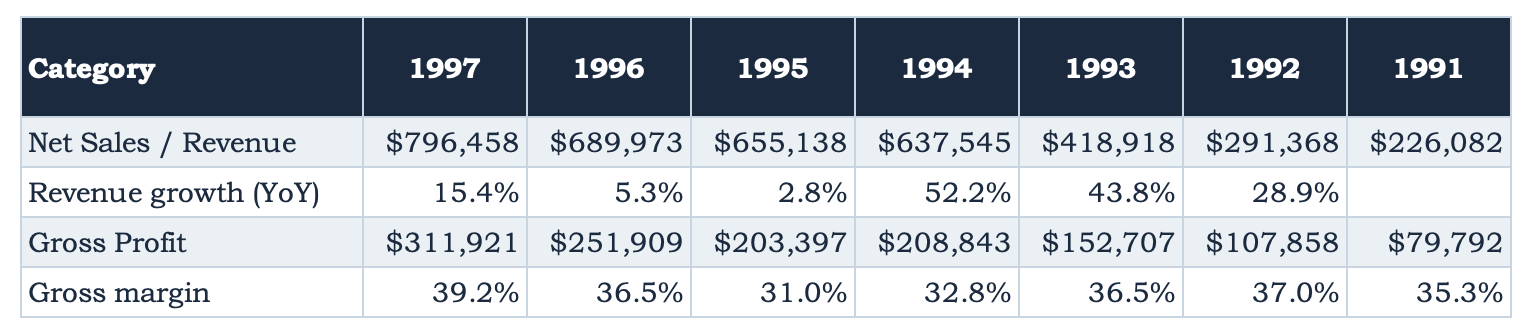

With that concern squarely in mind, CEO Sidney Swartz embarked on a plan to stop manufacturing most of the company’s products and begin the outsourcing of their production in order to save on costs and raise gross margins. During 1995, the company took its biggest step in that direction, shutting down two manufacturing facilities in the US and reducing operations in the Dominican Republic. The actions resulted in a one-time restructuring charge of $16.0mn for 1995. In the 1995 10-K, the company also reported that it expected to realize annual savings of $7mn as a result of the restructuring.

The company reported a -$11.6mn net loss for 1995, so adding back the restructuring charge and adding on the anticipated $7mn of net savings brings the pro forma net income for 1995 to $11.4mn. While it’s true that only represents a 1.7% net margin on $655mn of revenue, it is a much better picture than the headline net income figure suggests.

Perhaps most importantly, the restructuring charge demonstrates that management did not have its head buried in the sand when it comes to making difficult choices to better manage its business and implement good, modern, high-margin business practices. By 1997, the company had outsourced 72% of its footwear products manufacturing, compared to only 21% in 1992.

1995 issue #2: Lower gross margins after product pricing cuts

Starting in 1993 and into early 1994, Timberland lowered prices on some of its boots to help increase volumes and in an attempt to bifurcate or better appeal to its different customers. Those changes helped dramatically drive revenues up 52% from $419mn in 1993 to $638mn in 1994. But in 1995, when revenue only increased 2.7% to $655mn (and footwear volume actually declined by 6.0%), the pricing strategy was criticized.2 From the same CNN Money article:

The inexperienced Jeffrey [Swartz, then COO of Timberland] compounded the problem by lowering prices on some products in an inexplicable effort to bring the premium-priced brand down to a less lofty level. As often happens, the price cuts didn’t spark offsetting higher volume. Result: margin squeeze.

Such a strategic move might have been hard to analyze in 1995, however, any potential questions about the company’s strategy were quickly rectified as revenue growth picked up again in 1996 and 1997 and, most importantly, gross margins were not just exceeding the poor 1995 levels, but were near or above record levels. All of this would have been apparent to Li considering an investment in October 1998.

1995 issue #3: More company debt, more interest expense, and more SG&A than in prior years

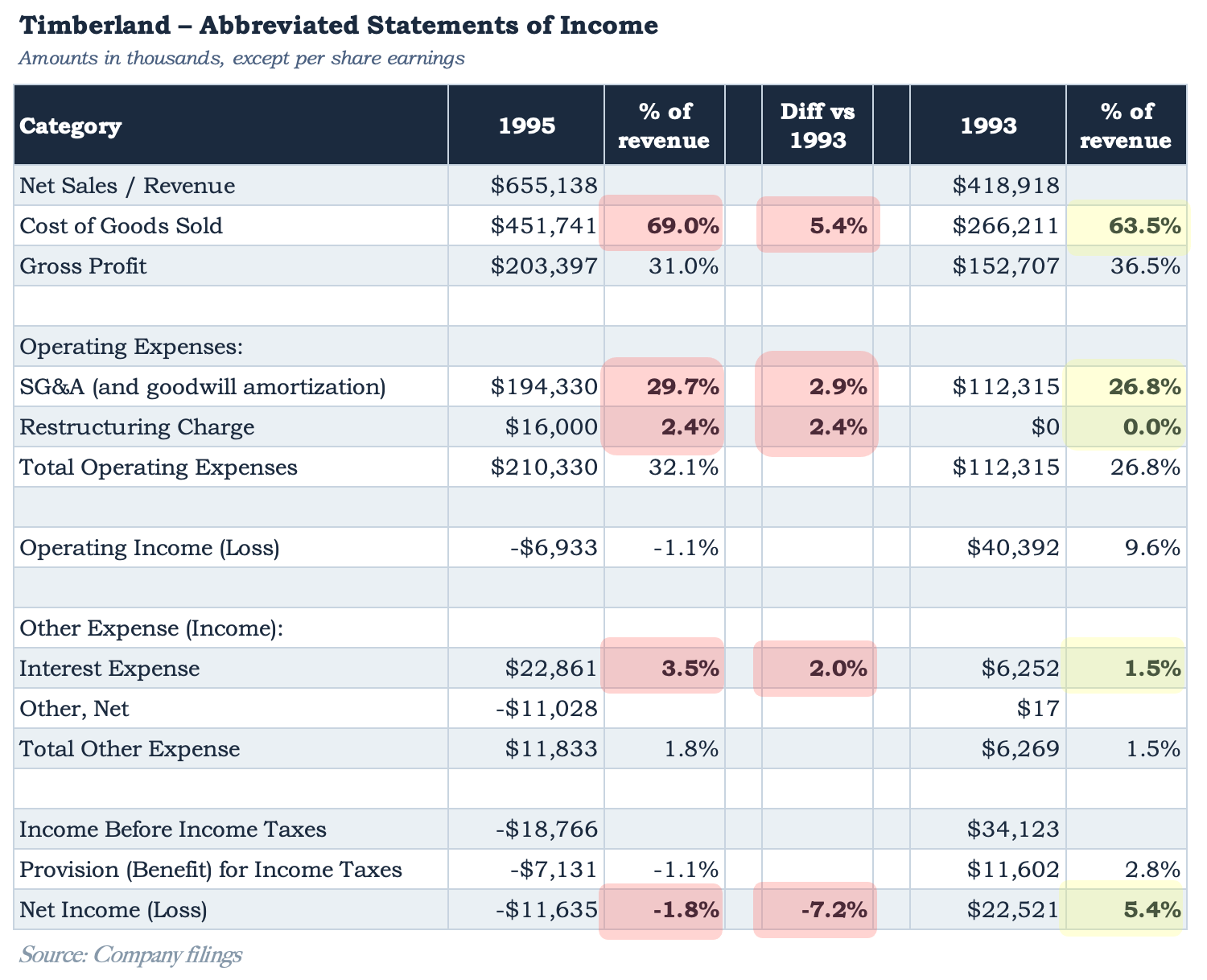

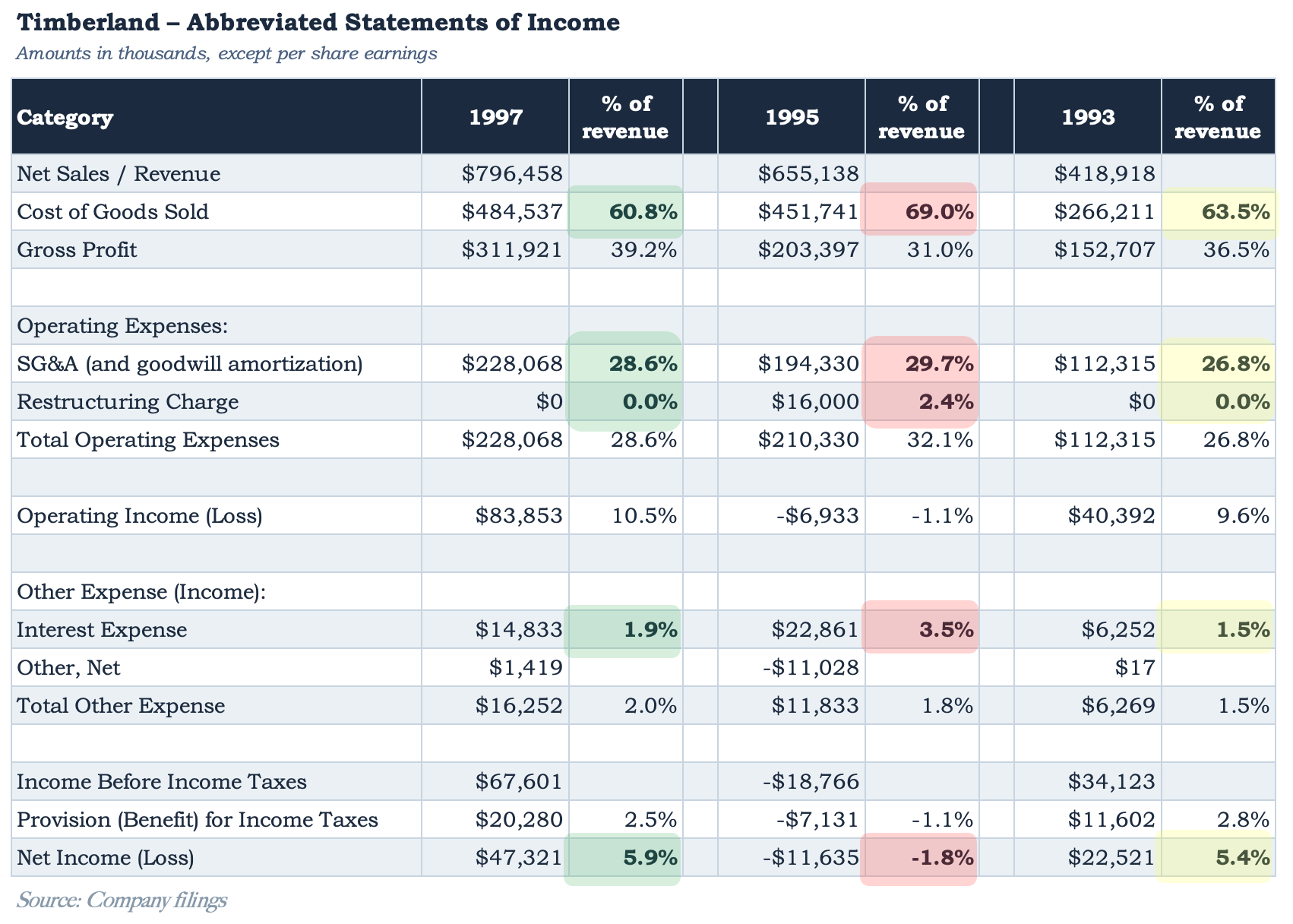

Timberland’s 1995 income statement can be broken down to show another concern not mentioned by Li: both SG&A expenses and interest expenses had risen sizably as a percent of revenue. The 1995 income statement is shown below versus the 1993 statement for comparison.

The company’s 1995 10-K does not give much commentary around why this was the case, except to say that increased debt levels are being used to prepare the company for more growth:

Interest expense increased to $22.9 million in 1995 from $15.1 million in 1994 and $6.3 million in 1993. The increases primarily reflect higher debt levels attributable to business growth and to support higher than anticipated inventory levels. The increase in 1994 also reflects higher interest rates.

I think the lack of disclosure here is stark, and lack of disclosure is perhaps the main reason why Timberland’s stock price was down so much in 1998. It is clear from reading Timberland’s company reports that management had no interest in making more disclosures than it absolutely needed to and, as a result, had a reputation among investors and the media as being nebulous at best and incompetent at worst.

The lawsuit mentioned above seems to have been a big part of that. Also, as Li mentions in his talk, and as cited in the company’s 1997 proxy statement, the founding family owned 51% of the company’s stock, and the company tended to generate more cash than it needed to run the business. As a result, it did not have much need for the equity brokerage services of Wall Street (and didn’t need to cooperate with or cater to Wall Street equity analysts either). Without the need for Wall Street, and, worse, having been punished with a lawsuit for stating too much, company management now kept its mouth shut. And if the stock suffered because of it, who cares? The Swartz family owned 51% of the stock and the company generated enough cash flow to sustain itself.

To the owner/managers of Timberland, no one or nothing would bully them, not lawsuit plaintiffs, not media commentators accusing them of incompetence, not equity analysts pining for more information, and not swoons in the stock price.

This was another important understanding that Li gained in his research. The company had its own reasons for ignoring public commentary and ignoring its stock price, all while consistently improving the company’s fundamentals. Timberland’s management followed the Mr. Market parable, and Li would as well.

In addition, it would become further evident how wrong the popular narrative was around management when Li met them himself, as we’ll soon see.

Most importantly, the issues around SG&A and interest expense had abated by the time of the investment in October 1998. By then, the company’s investments in SG&A had become apparent, with revenues increasing and gross margins at or above all-time highs. And the company had used some of its cash to pay down over $100mn of the $225mn in debt it incurred in the 1993-1994 period (and, as a result, its interest expense came down too).

Timberland had a lot going for it

Throughout the talk, Li describes the extensive work he did to assuage himself that concerns around Timberland were not serious. In fact, as mentioned, many of the criticisms of the company were outright resolved by October 1998.

But the lawsuit, in particular, made Li curious. Maybe he missed something, and the suit was indicative of a management team that was irresponsible or even committing fraud. In the most entertaining and engaging part of his discussion, Li describes visiting the community where the Swartz family lived and even going to their synagogue. He got to know their friends and community members. From start to finish, Li reports that his entire investment research took him “a couple of weeks”, so it seems like this boots-on-the-ground scuttlebutt may have taken him only several days in the Boston, Massachusetts area.

During that time, Li discovered not only that the family wasn’t a bunch of crooks, but actually that they were admirable and well-respected. Li would have been 32 years old in October of 1998.

The Chairman and CEO of Timberland for many years was Sidney Swartz, son of the company’s founder, and he would have been about 63 years old at this time. In June of 1998, his son Jeffrey took over as CEO. Jeffrey would have been 38 years old and Li’s contemporary. In a clever and original move, Li realized that Jeffrey was on the board of a company with one of Li’s friends, and Li managed to have himself placed on that board, just to get to know Jeffrey better. Li says that the insights he gained painted a very different picture than the media’s image of Jeffrey as a young and inexperienced CEO:

He took over as CEO and he had entirely different ideas about how to run a company. It was very articulate. He was one of the most articulate [people I] ever met. Still is.

This hands-on visit to Jeffrey’s home town is the most striking and eye-opening part of Li’s talk. It demonstrates the kind of dedication it takes to invest well and also the kind of novel thinking that helps unearth insights that others may not have.

By going the extra mile (literally), Li was able to gain a critical and novel insight about the family that the media and other investors were missing. The family and the company’s young CEO were very competent, in contrast to the prevailing narrative. Also, and importantly, the new CEO was about to change the company’s stance on Wall Street and begin communicating more, increasing the likelihood that investors would begin to see what Li was already seeing. In fact, Li mentions that the company began holding analyst meetings shortly after Jeffrey took over as CEO and Li began investing:

He initiates... analyst meetings and the first meeting... how many people showed up? It was him, me, and another analyst, three people. And the last analyst [meeting I went to some time in the year 2000] the room is just absolutely filled with nearly 50, 60 people. [Half-joking] So, that’s how I know when I have to sell.3

Li’s investment

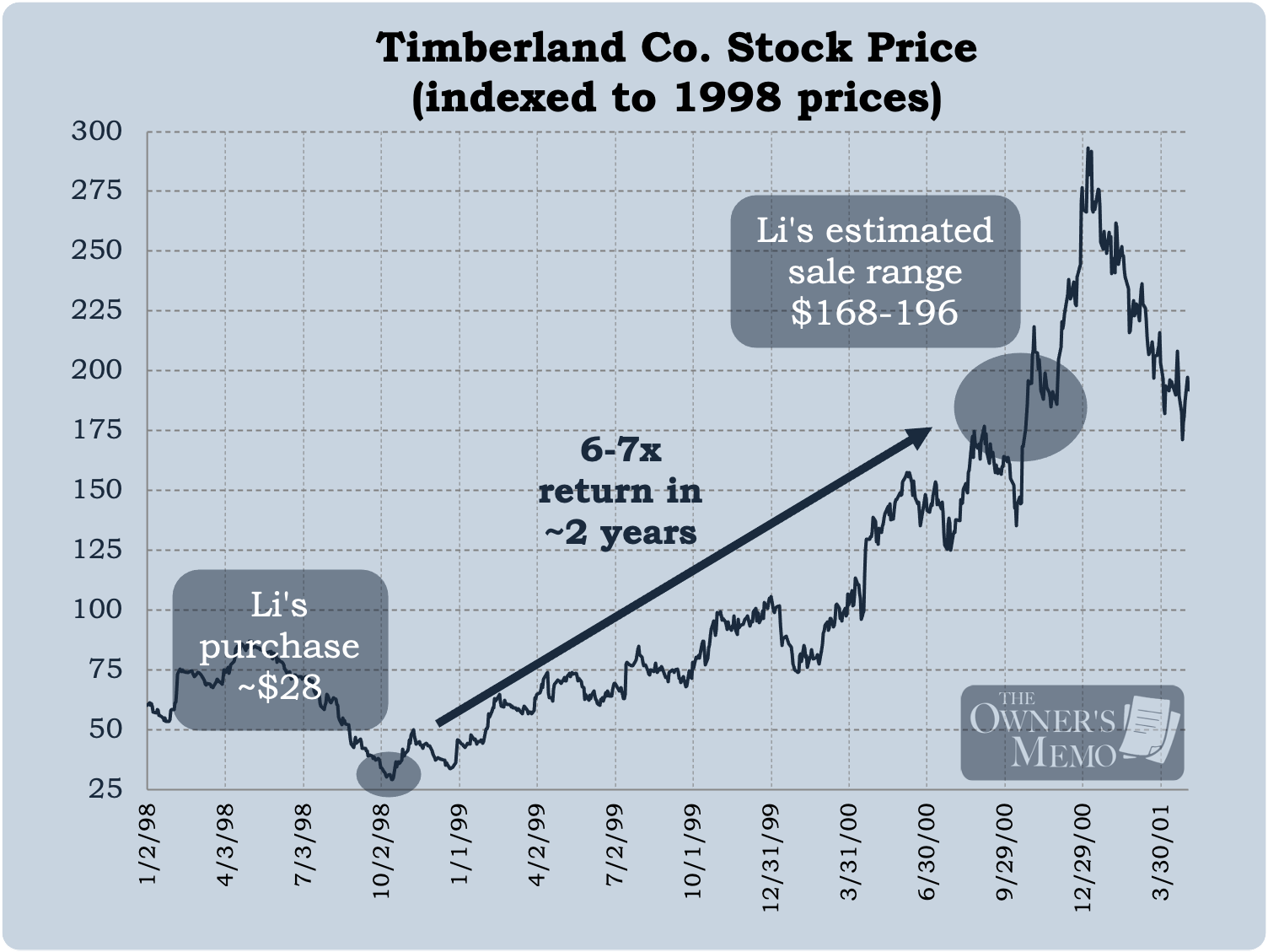

In the end, Li made an investment in Timberland some time in October of 1998. He cites a price of around $28 per share; such a purchase would have been remarkable timing. Timberland’s shares closed as low as $28.94 on October 15th and only closed below $30 per share for three days around that time.

We don’t know exactly when Li sold his shares, but he describes a stock that subsequently went up seven times. Timberland closed as high as $293.00 per share (unadjusted for stock splits) in January 2001 which would have resulted in a 10.1x return trough to peak in just over two years. (The real-time price peak would have been $73.25 after two 2-for-1 stock splits.)

Summary: A very good company at a very low (and temporary) price

Li Lu’s purchase of Timberland is a particular type of great investment. Timberland was a very good company (though not an all-time great one) that had a lot going for it, like a great product and increasing customer demand. Revenues were consistently increasing, and the company had invested a lot of money in prior years anticipating even more revenue growth. Earnings were increasing along with revenues too. And with that backdrop came a stock that had irrationally been beaten down to a P/E ratio of 6-7x, or an earnings yield around 15%, on industry concerns that felt more like a hiccup for the company.

After unearthing all the potential concerns he could and doing a boatload of research and live scuttlebutt too, he realized that those concerns were not valid enough to hurt the company’s long-term prospects (and, to state it more strongly, they arguably weren’t even meaningful to the company at all).

Timberland wasn’t a once-in-a-lifetime great company or investment that could be owned forever. (It is very difficult for retail clothing manufacturers or fashion companies to rise to that level.) But it was one example of a good investment: a very good company that makes a great, beloved product, whose revenues and earnings have been rising and that is suffering a decline in stock price due to extraneous factors that didn’t threaten the business long-term.

In addition, the study of Timberland also highlights the power of using Value Line as a source for new investment ideas. The manuals are still printed today, and a diligent and tireless review of the tables and companies listed still offers the chance at a great investment opportunity like the one in Timberland.

Timberland’s financial reports seem to give only sparse details around many aspects of the business at the time. One is left to wonder whether the 1994 lawsuit had a impact on Timberland’s management and led them to report only the bare minimum to investors. It would have made an investor’s job harder in 1998, but the rewards for digging in would have been great.

Boot-industry sales were lackluster too in 1995 due to “warm weather”, which also hindered Timberland that year.

Li also mentions that Jeffrey Swartz would go on to become an investor in one of Li’s funds. It seems that the diligence with which Li pursued his investment in Timberland made a great impression on Jeffrey. This tidbit also provides an interesting lesson: great, hard work has a way of conveying benefits that the practitioner may not even intend.