Tenneco Automotive: Charlie Munger’s $80 Million Bargain, Part 1

The Owner's Memo #7; In 2001, Charlie Munger read one article and made an $80 million decision in ninety minutes.

This edition is Part One of Charlie Munger’s investment in Tenneco Automotive. Find Part Two at The Owner’s Memo #8.

The story of Charlie Munger’s investment in Tenneco Automotive is a fascinating one. And as far as I can tell, it’s only been told in a cursory way before now.

Munger made the investment in 2001 and it likely returned to him somewhere between 4 1/2 to 7 times his money and an annualized return over three years of 65% to 93%.

This is the story.

Casually discussing an $80 million profit

At the 2017 annual meeting of the Daily Journal Corp., Charlie Munger spoke to visitors for almost two hours, answering any of their questions. At one point, he mentioned an investment that made him $80 million in profit.

The exchange between Munger and the off-camera crowd of onlookers is very funny. Munger mentions the $80 million, and you can feel the people around him restraining themselves but wanting to ask him about every detail.

Munger never mentioned the company name, but I’ve come to find out that the company he invested in was Tenneco Automotive Inc. (which we will refer to as Tenneco).

Let’s break down what Munger saw at the time and what we can learn from it.

Below, I have transcribed the relevant part of Munger’s comments:

I read Barron’s for 50 years. In 50 years, I found one investment opportunity in Barron’s out of which I made about $80 million with almost no risk. I took the $80 million and gave it to Li Lu, who turned it into 4 or 5 hundred million dollars. So I have made 4 or 5 hundred million dollars from reading Barron’s for 50 years and following one idea... I didn’t find them that easily but I did pounce on one.

It was a little automotive supply company... It was a cigar butt... It was [the maker of the] Monroe shock absorber... The stock was a dollar and the junk bonds which paid 11 3/8% were [priced at] 35. And when I bought the junk bonds, they paid me the 35% and they went right to 107 and were called. And the stock went from 1 to 40, but of course I sold my stock at 15.

Audience member: How long [did it take] you to make the 15x on the stock?

Maybe a couple years.

Audience member: How long did it take you to make the decision to buy it once you read the article?

Oh, about an hour and a half.

I kind of knew based on experience how sticky some of that auto secondary market was, and how many old cars needed Monroe shock absorbers, and I just knew it was too cheap. I didn’t know it would work for sure but I knew [it was cheap].

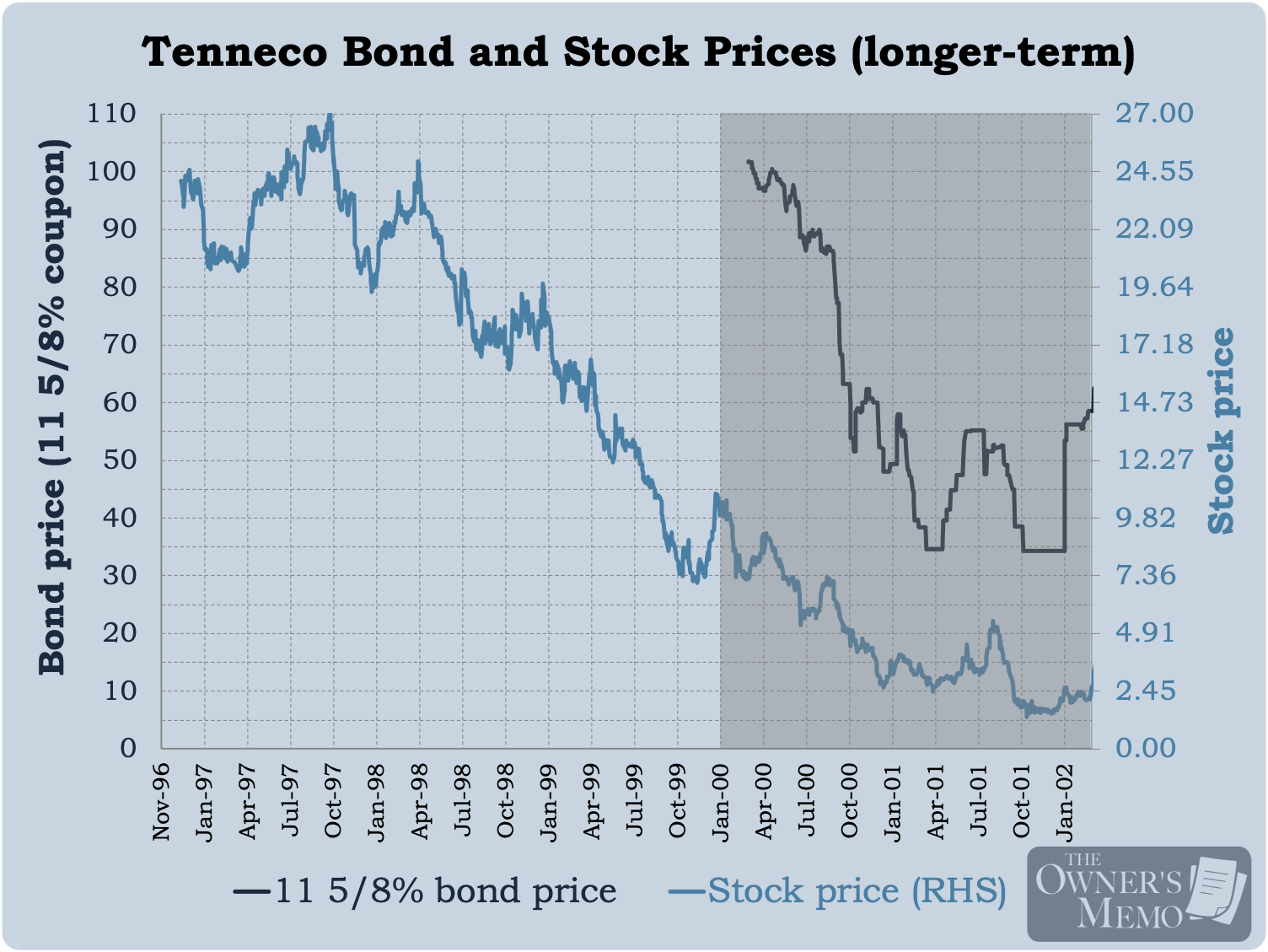

When did Munger make his investment?

Determining the identity of the company Munger was talking about was the easiest part of this case study. A quick internet search revealed that Tenneco Inc. is the manufacturer of the Monroe shock absorber today, and the company’s financial filings show that it has been doing that business since acquiring the Monroe Auto Equipment Company in 1977.

Based on Charlie’s comments above, I believe he made his investment in Tenneco late in 2001. How do I know this?

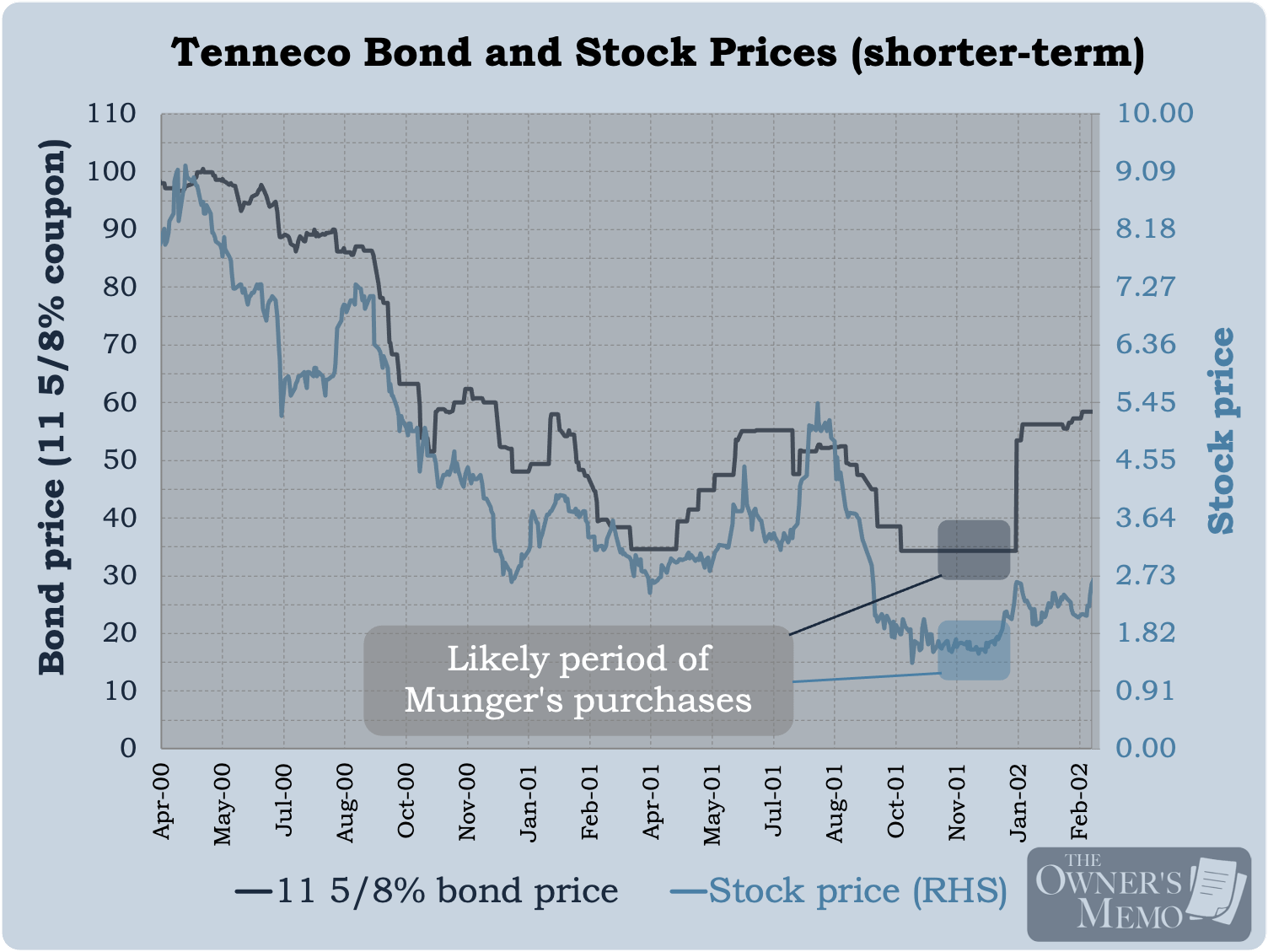

Charlie mentions the stock price being “a dollar” and the bonds with a coupon of 11 3/8% being priced at 35. I created a list of the historical issuance of Tenneco bonds using Bloomberg, and the list did not show any bonds with an 11 3/8% coupon, but it did have one bond with an 11-handle coupon, the 11 5/8% bonds issued in October 1999. Prices for that bond indeed show a sharp decline during 2000 and 2001, bottoming right around 35 in March and October 2001. I think these were the bonds Munger bought, and he simply misremembered the coupon.

Also, while Tenneco’s stock price never actually reached the price of $1, it was trading in late 2001 in a range from as low as $1.35 to around $2 per share.

Based on that pricing, I think this is the period when Munger read the article that he mentioned and made his purchase in Tenneco’s bonds and stock. As I’ll show later, I think he did so in December 2001 specifically.

What was the mystery article that Munger read?

Munger mentions that he read an article in Barron’s about Tenneco, and that’s what made him investigate the opportunity to invest. I was intrigued by the idea of finding the exact article he read, so I made a thorough search of the Barron’s archives from June 2000 through 2002 using the ProQuest research database. However, I could find no articles that substantially discussed the company.1

Perhaps Munger misremembered the publication he was reading that contained the Tenneco article. After all, he was telling this story in 2017, fifteen or sixteen years after it happened.

With that in mind, I conducted a more thorough search of news archives using ProQuest. And I came across an article that seemed to fit the scant details provided by Munger. The article is titled “Tenneco Struggles to Pare Down Debt”, and it appeared in the December 3, 2001 issue of Crain’s Business Chicago. I’ve reproduced the article here.

I believe this is the article that Munger actually read, despite him remembering it as being in Barron’s.

Why do I think so?

First, the article was published around the right time, when the stock and bonds were trading at prices close to those mentioned by Munger. And the article specifically mentions Tenneco’s bonds as suffering, not just the stock price:

...the company’s stock closed on Nov. 29 at $1.68, nearly 70% off its 52-week high... Meanwhile, the $500 million in bonds the company issued in 1999 are trading at around 34 cents on the dollar.

Second, the tone of the article is pretty well balanced. It describes the troubles Tenneco was having, but it also quotes the CFO discussing how Tenneco might survive. That may have served to stir Munger’s thoughts about the company getting through the downturn and emerging in good shape.

With $443 million available on a $500-million revolving credit facility at the end of the third quarter, Tenneco Chief Financial Officer Mark McCollum says he’s not worried about a cash squeeze.

“It’s not a situation we believe would create ... an immediate liquidity problem if the revolver is available,” he says.

As far as I can tell, this is the first time anyone has found a candidate for the article Munger may have been talking about.2 The article isn’t critical to understanding the Tenneco investment, but it is useful and intriguing to see the actual material that may have spurred Munger’s thinking.

With that itch scratched, let’s now dig into the research that Munger might have done at the time, what he would have seen in the company’s fundamentals, and what compelled him to think that a purchase of Tenneco’s bonds and stock would be profitable.

Assuming Munger read the Crain’s article in the month of December 2001, he would have had access to the 10Q filing from Q3 of 2001 (filed on November 14, 2001) and the annual report from 2000 (filed on March 30, 2001). Naturally, we will restrict ourselves to financial information from those reports and earlier, nothing later.

The Fundamentals of Tenneco’s Business

It’s always amazing to me how much can be learned from simply reading company reports and disclosures. For Tenneco, there are a few relevant points or challenges that jump out of the 2000 annual report.

Challenge #1: Massive company change

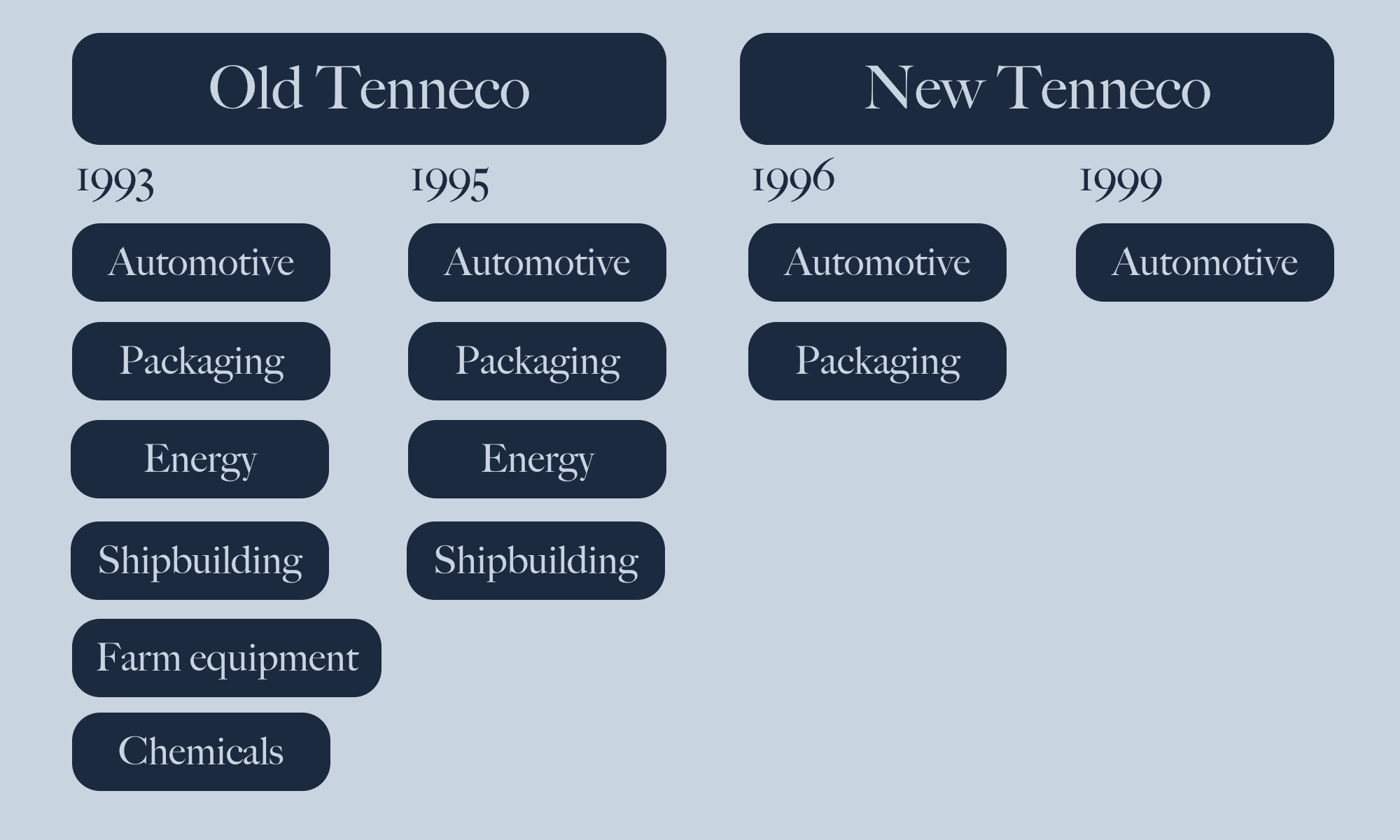

In the years prior to 2000, the company underwent several major spinoff transactions of other businesses, completely changing the company.

In 1993, “Old Tenneco” was a large conglomerate in six businesses: automotive, packaging, farm equipment, shipbuilding, energy, and chemicals. In 1994 and 1995, each of the chemicals and farm equipment businesses had been spun out in IPO’s. In 1996, the company spun off its shipbuilding business and sold its energy business. The automotive and packaging businesses were transferred to the “New Tenneco” company. Then, in a series of three transactions in 1999, New Tenneco spun off its packaging business, first forming and retaining 43% of a joint venture, then selling a part of the business, then ultimately spinning off all of its packaging businesses in a new company called Pactiv Corp.

What remained at the end was Tenneco’s automotive business, which sold emissions products (exhaust systems) and ride control products (like shocks and struts). It was this business, Tenneco Automotive Inc., that Munger was considering in 2001.

To say the above series of transactions dramatically changed the nature of Tenneco’s business is an understatement. The company went from being a large, diversified conglomerate with $13.2 billion in revenue in 1993 to a smaller single-line automotive businesses with just $3.5 billion in revenue in 2000.

The substantial changes to the company may have contributed to the decline in the company’s securities prices at the time Munger was looking at the company. I am reminded of Joel Greenblatt’s book You Can Be A Stock Market Genius, in which he discusses the merits of investing in spinoffs:

The spinoff process itself is a fundamentally inefficient method of distributing stock to the wrong people. Generally, the new spinoff stock isn’t sold, it’s given to shareholders who, for the most part, were investing in the parent company’s business. Therefore, once the spinoff’s shares are distributed to the parent company’s shareholders, they are typically sold immediately without regard to price of fundamental value.

In the case of Tenneco, something similar may have been happening to the parent company. There were likely a bunch of shareholders who first owned shares in a diversified conglomerate (as recently as 1998 or 1999) and, by 2001, found themselves owning an undiversified automotive business in an industry suffering from a recession. That could have been a recipe for indiscriminate selling.

Challenge #2: Tenneco’s debt load

Tenneco was saddled with a lot of debt as a result of the spinoff transactions.

After all these spinoff transactions were finished, Tenneco was left with approximately $1.5 billion of long-term debt. After reading the history of Tenneco above, I suspect the automotive business was a victim of circumstance with respect to its debt load, being the last business standing after management spun off or sold five others.

When management spins off or sells a business, the natural inclination is to support that business in order to make the spinoff successful or the business attractive to a buyer. Often, this means allowing the spinoff or sale to leave some of its debt behind at the parent.

This was the case for Tenneco’s automotive business, the last of six businesses remaining.

The prior spinoff and sale transactions, each in small steps, left a little too much debt behind at the parent company in order to ensure their successes. Tenneco’s automotive business, by virtue of being the last business remaining, was the entity that was forced to deal with the excess debt at the end of the day.

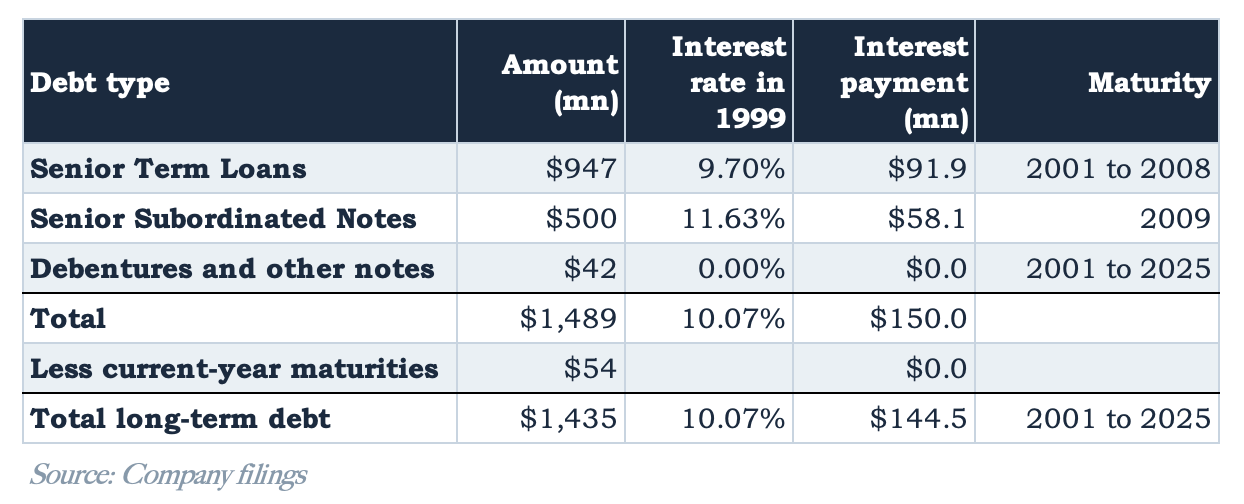

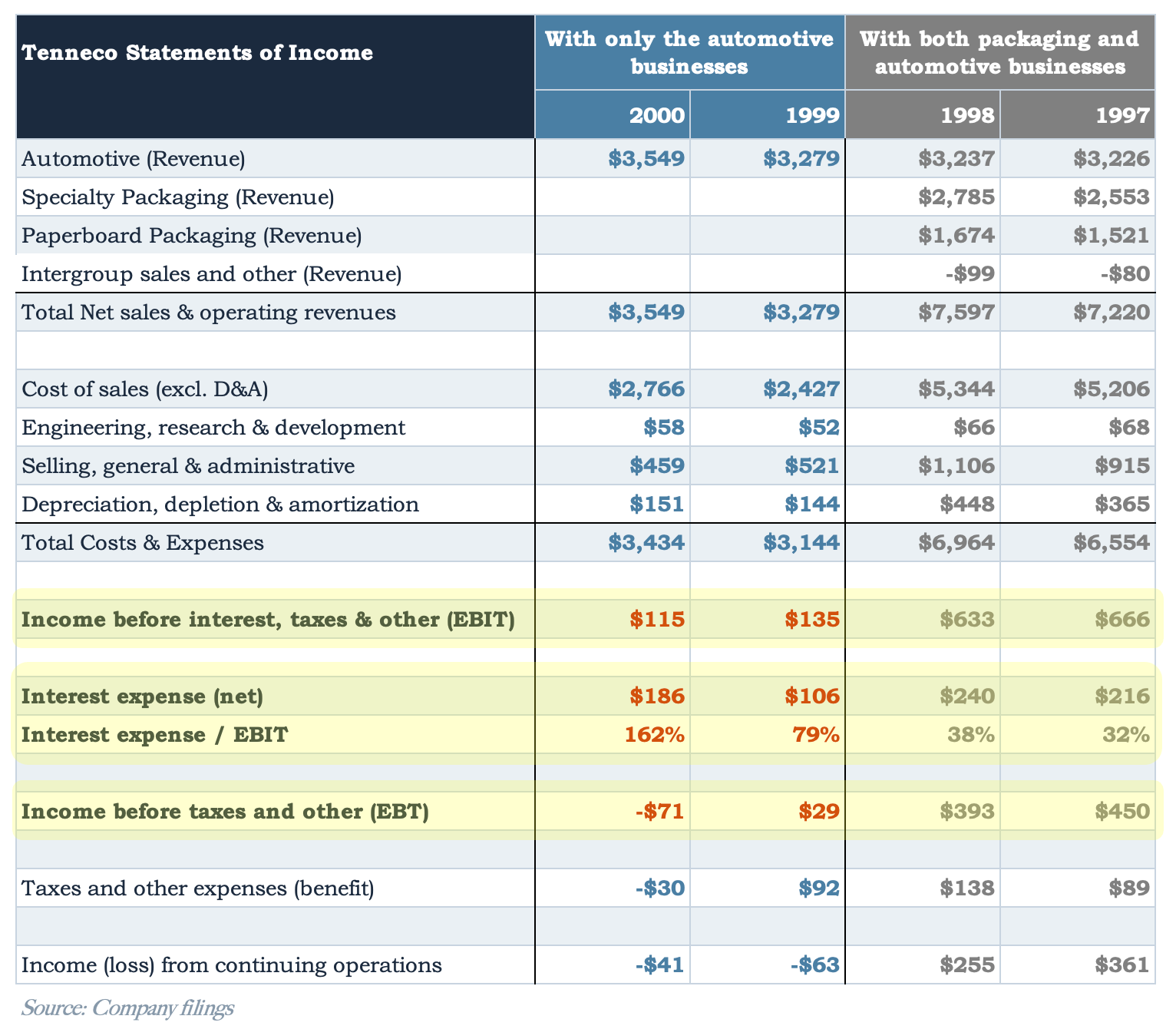

Tenneco’s long-term debt profile, per its annual report from the year 2000, is shown below.

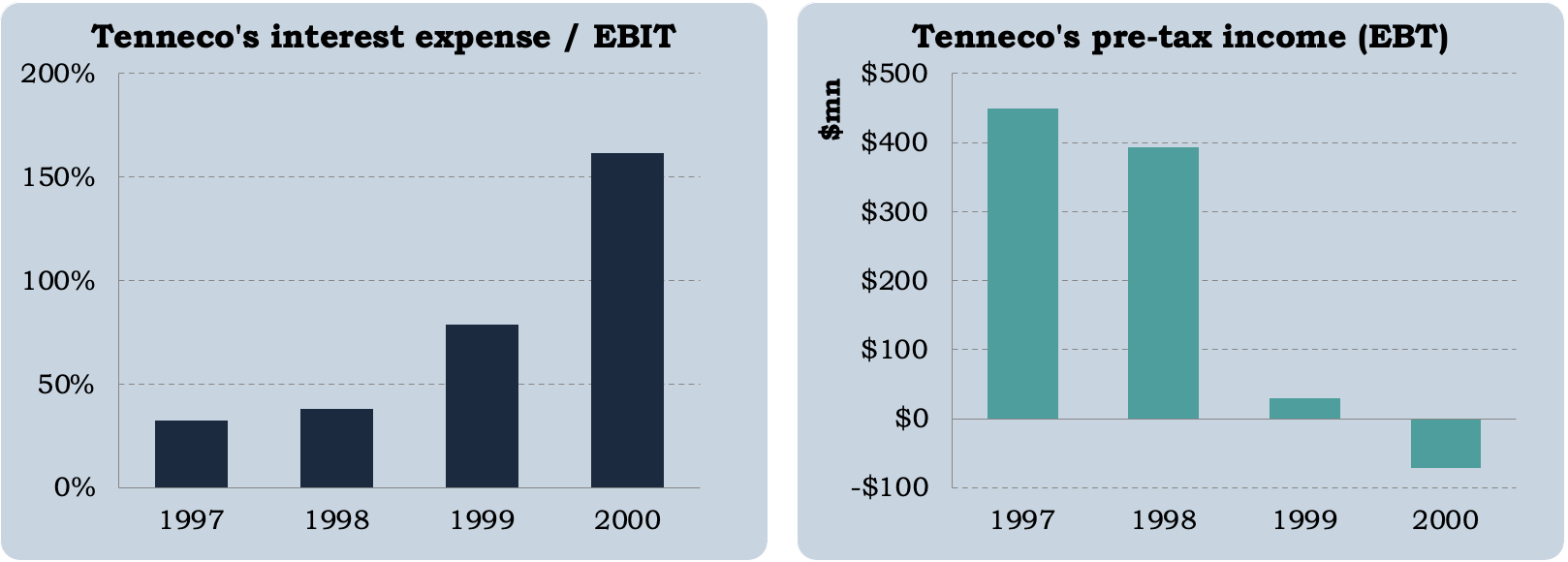

Pactiv Corp. was spun out in November 1999, and after that, it was almost immediately clear that $1.5 billion of debt was a dangerously large amount for Tenneco’s remaining automotive business to bear. The table below shows the company’s financials for the years 1997 and 1998 (with both the packaging and automotive businesses) and 1999 and 2000 (with only the automotive business, plus a lot of debt).

Focus for a moment on the company’s Operating Income (EBIT) and Interest Expense. Prior to the spinoff of Pactiv, the company was doing well, earning $633mn in EBIT in 1998 and spending $240mn in interest payments, but after the spinoff, the company was earning only $115mn in EBIT and spending $186mn in interest payments. Clearly, the company had too much debt at too high an interest rate.

Challenge #3: The 2001 recession

Tenneco was burdened with too much debt, and it was obvious from looking at their financial reports.

To add insult to injury, Tenneco’s revenues were also suffering from the 2001 recession.

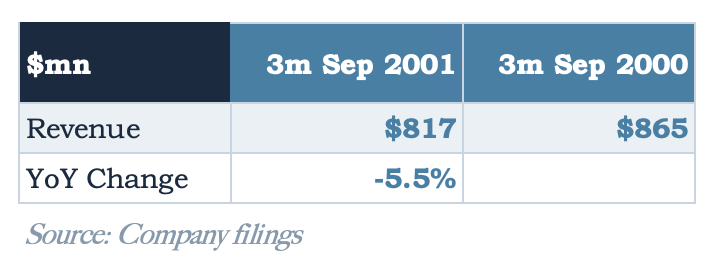

Tenneco served two broad sets of customers, original equipment manufacturers (auto makers) and the aftermarket (auto repair shops). Both were suffering lower sales. The 10Q report from 2001 Q3:

In late fourth quarter 2000, several of the company’s major North American original equipment customers began announcing significant reductions in scheduled vehicle production levels. Based on these reductions, we anticipate that the North American original equipment manufacturer build rate for light vehicles in 2001 will be down from 2000 levels in the range of 10 percent to 12 percent and that weaknesses in the heavy-duty truck market will continue through 2001 and into 2002... The global aftermarket exhibited a further weakening of demand for replacement parts during the latter portion of last year. We anticipate that there will be further declines in the global aftermarket industry in the range of 6 percent to 10 percent in 2001.

The recession and auto industry weakness can be seen in this 10Q report, the latest financial report that Munger would have had access to at the time. Sales were down in Q3 2001 by -5.5% year over year.

Finally, let’s also not forget that, if Munger was looking at the company in December 2001, the public and the stock market would still have been reeling and worried about the effects of the September 11th attacks.

Challenge #4: Principal payments were coming due

Not only were the interest payments on Tenneco’s debt too much for the company to handle in the years after completing its spinoff, but, on top of that, principal payments were starting to come due in 2001. The annual report from 2000 lists those upcoming maturities as $54 million, $109 million, and $99 million for 2001, 2002, and 2003, respectively. From the perspective of a casual analyst or observer, it was not clear at all how Tenneco could make those payments or how likely they were to work with their lenders on renegotiating terms.

Tenneco’s situation, viewed from the outside in late 2001, looked pretty grim. A company drowning in debt, revenues shrinking, and principal payments coming due. Was there anything worthwhile that an enterprising investor could see? Next week, in Part Two, we’ll look at what Charlie Munger saw beneath the surface, and how it made him $80 million.

There were six articles in total that made only passing mention of Tenneco during that search period. There were two substantial articles as well, “Parting Company“, and “Flunking Math“, but those were from February 22, 1999 and February 14, 2000, when the stock and bond prices were much higher. I could find no substantial articles in Barron’s around the time that Munger would have been making his investment.

There was also a compelling second article that could have been the one Munger read. It is entitled “Tenneco: Swerving Away from Chapter 11?”, and it appeared in the September 10, 2001 issue of a trade journal called the Mergers & Acquisitions Report. I’ve reproduced that article here. While it is impossible to know which one Munger actually read, I believe the Crain’s article is the better candidate due to the popularity of that publication and due to the timing of its article. On September 10, the last recorded bond and stock trading prices were 47.50 and $3.30 per share, higher than the prices Munger quoted, whereas, on the day the Crain’s article was published, those prices were 34.25 and $1.56.

Looking forward to part 2

Great detective work!