Tenneco Automotive: Charlie Munger’s $80 Million Bargain, Part 2

The Owner's Memo #8; What did Charlie Munger see in Tenneco, a struggling auto equipment maker on the brink of bankruptcy?

In Part One, I laid out the challenges facing Tenneco Automotive in late 2001: a crippling debt load, a recession, and a business that had been turned inside out by five years of spinoffs and business sales. It looked like a company heading toward bankruptcy. So what compelled Charlie Munger to invest?

Was there anything positive about Tenneco’s business?

Given all the challenges I discussed last week, Tenneco’s situation seemed pretty dire to the casual observer in 2001 (and even to many financial analysts). However, beneath all these challenges, there were some positive points about the company, each of which were evident with a careful reading of the company’s annual and quarterly reports.

Positive point #1: Tenneco had great brands and a broad customer base

Tenneco produced auto products in two business segments: Emission Control and Ride Control. In both of those business segments, it had brand names with an excellent reputation and market share. Their leading position is backed up by disclosures in the 2000 annual report:

In each of our operating segments, we manufacture market leading brand names. Monroe® ride control products and Walker® exhaust products are two of the most recognized brand names in the automotive parts industry...

In the [original equipment] market, we believe that we are among the top four suppliers in the world for both emissions control and ride control products and systems. In the aftermarket, we believe that we are the market share leader in the supply of both emissions control and ride control products in the world.

Moreover, Tenneco’s list of original equipment manufacturers was large, including just about every major auto maker in the world. And the largest automaker (GM) accounted for only 16.6% of the company’s sales, indicating the sales were nicely diversified.

Munger understood the great reputation of Tenneco’s products, as indicated by his brief comments at the Daily Journal meeting, when he stated:

I kind of knew based on experience how sticky some of that auto secondary market was, and how many old cars needed Monroe shock absorbers.

I think this point is critical to understanding Munger’s willingness to purchase these securities. Since customers loved and needed Tenneco’s products, the company still had fundamental value as an ongoing concern. We will see how pivotal this was in assessing the company’s likelihood to pull out of its debt problem.

Positive Point #2: Tenneco’s business was fundamentally healthy and profitable, apart from its large debt load

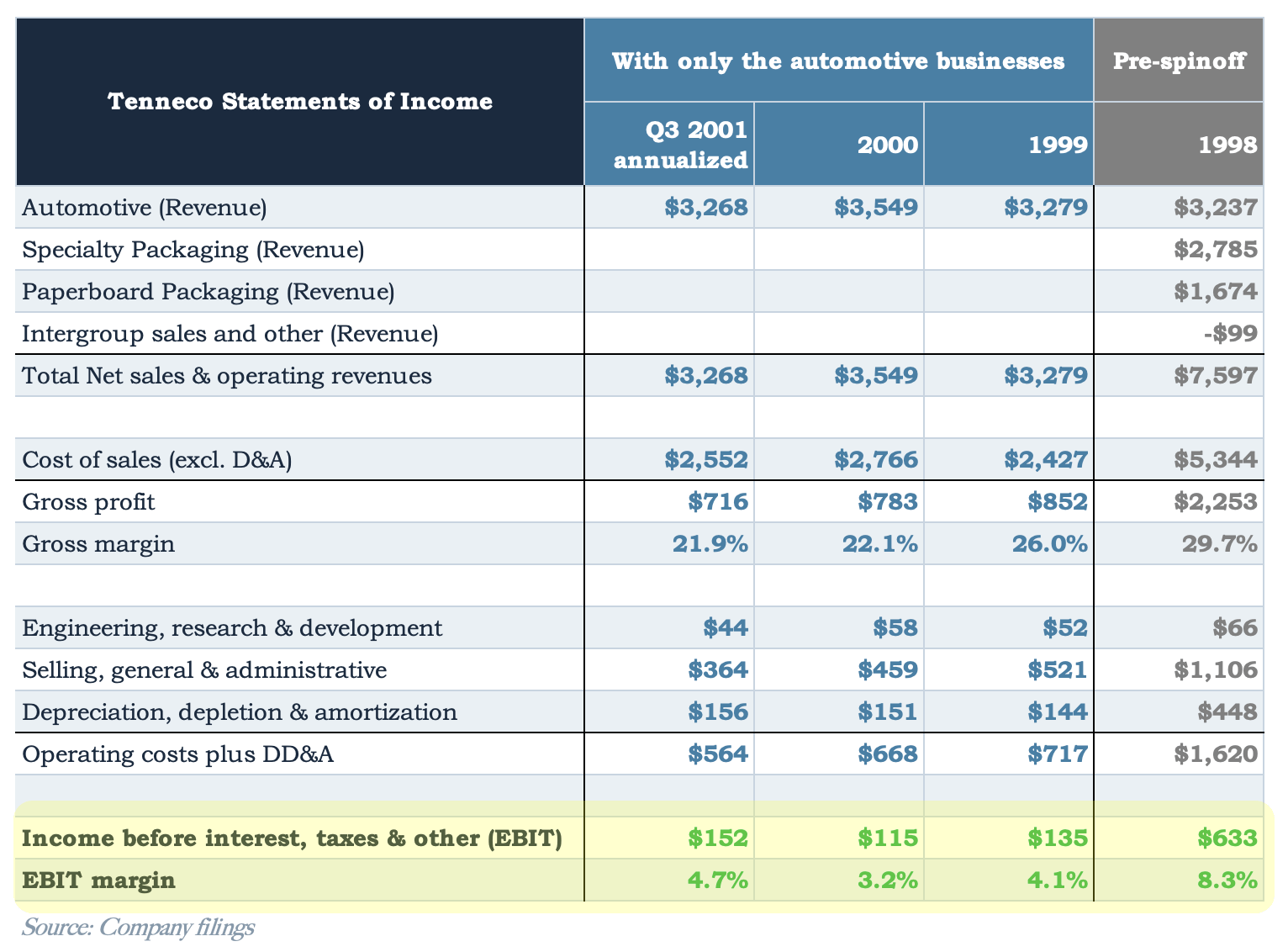

As indicated in Figure 4 last week (and as suggested by the company’s brand strength), Tenneco’s business was fundamentally profitable before accounting for the large interest payments on its debt.

Figure 8 below reproduces the abbreviated income statement from last week, this time stopping at EBIT and the EBIT margin. While the EBIT margin was low, especially compared to the company’s prior pre-spinoff years, Tenneco was still profitable before the large interest payments on its debt.

Moreover, even though sales were flagging as a result of the recession, the competitive nature and long lead times in the auto business meant that Tenneco’s management had a good idea about its order book for the coming two to three years, and those numbers revealed that the decline in sales, at least for the OEM segment, seemed to be abating by 2002. From the Q3 2001 10-Q report:

Based on anticipated vehicle production levels our global original equipment customer book of business is currently $2,305 million, $2,533 million, and $2,583 million for 2002, 2003, and 2004, respectively.

Positive Point #3: Management was pursuing aggressive cost controls post-spinoffs

Importantly, and perhaps underappreciated by the market, Tenneco was still in the midst of a major transition in its business. It had gone through five major spinoffs or sales of business units since 1993, it was facing its first recession since that time, and it was coping with all the debt it was saddled with after those spinoffs.

But digging in a bit to the company’s annual and quarterly reports makes it clear that management was keenly focused on right-sizing company expenses and running a more efficient organization. This is from the 2000 annual report:

Beginning in the fourth quarter of 2000, we undertook an aggressive cost-cutting initiative to reduce global salaried employment, followed by a second round of salaried employee reductions announced in the first quarter of 2001. We expect these combined actions to eliminate approximately 22 percent of our global salaried work force by early 2002. When this initiative is fully implemented, we anticipate realizing cost savings of $72 million annually.

We are also again tightly controlling capital spending and implementing a zero-based budgeting program that challenges spending requirements and habits throughout the organization. In addition, we are seeking to improve our manufacturing efficiency through the further adoption of lean processes and, most important, Six Sigma. We anticipate that these initiatives will provide savings of at least $20 million in 2001.

So, as of the end of 2000, management expected to generate a total of $92 million of savings by right-sizing its workforce and by adopting more efficient processes and practices.

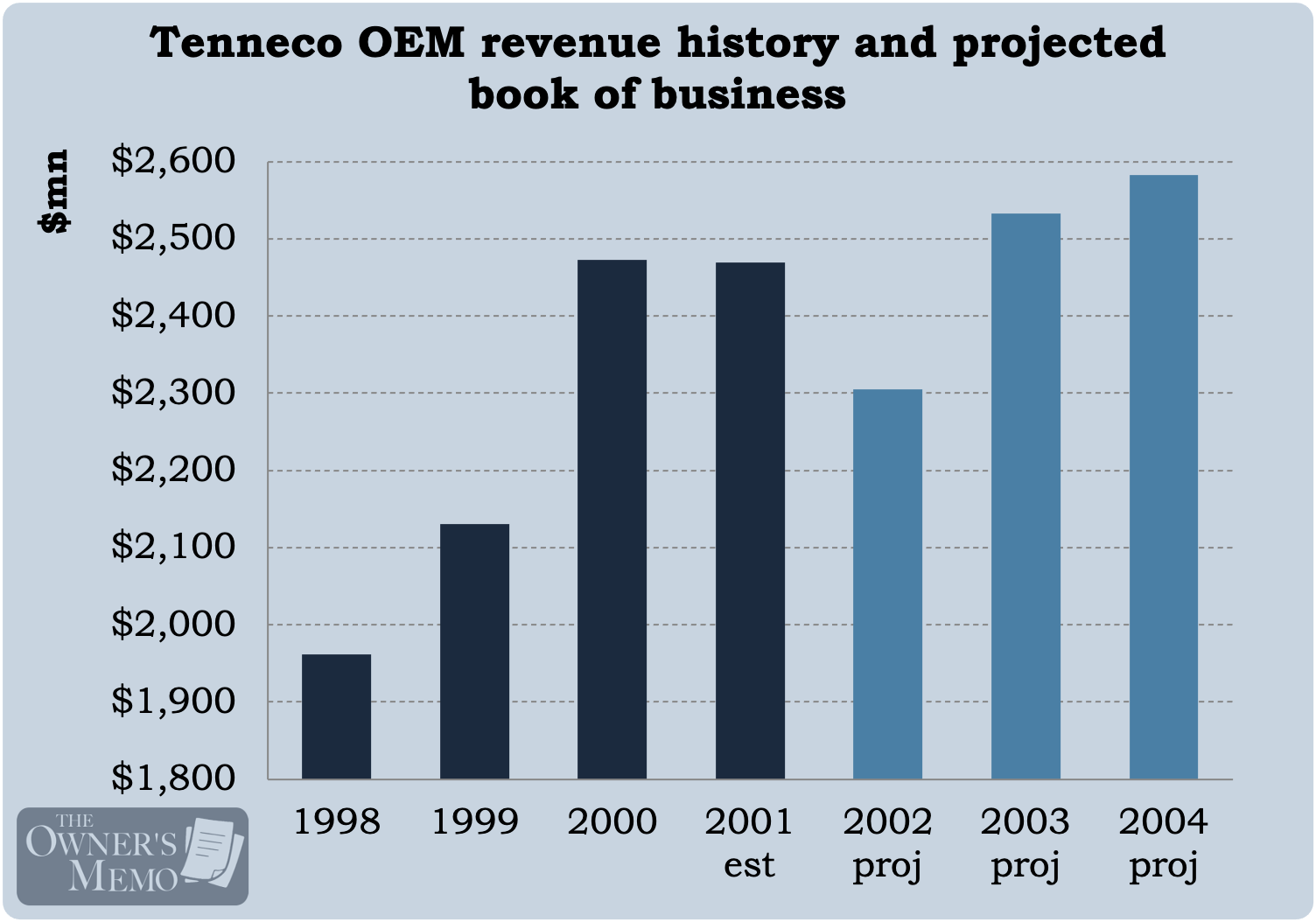

In fact, it was already becoming evident by Q3 of 2001 that those efforts were working better than expected. Figure 10 below (which is Figure 8 reproduced) shows annualized operating costs (plus DD&A) that were $104mn lower than those for the year 2000. And those lower operating costs boosted EBIT by 32% to $152mn.

Not only was the cost cutting working, it was having a large impact on earnings before interest.

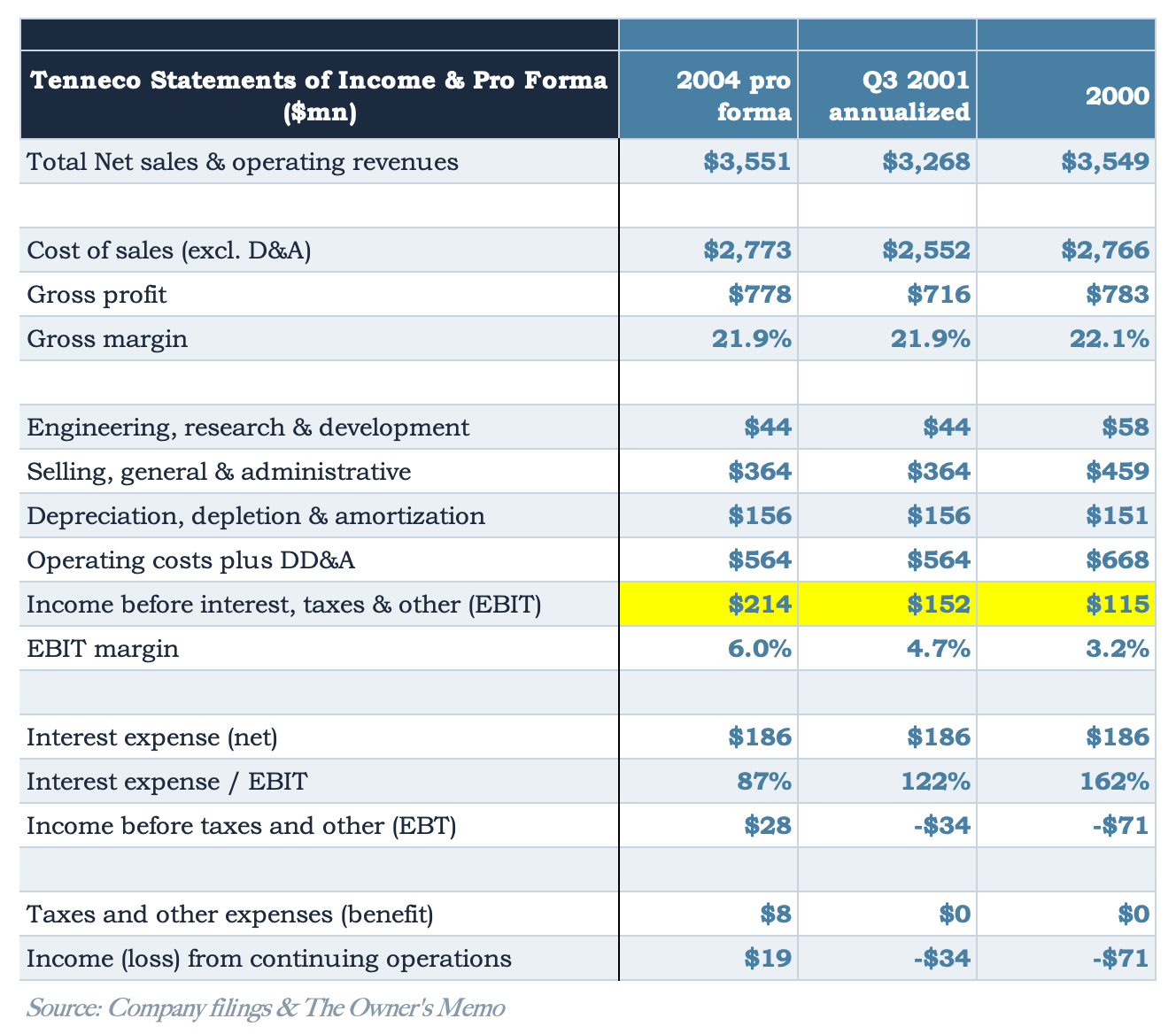

The Pro Forma Tenneco

To drive the last two positive points home, let’s imagine a pro forma income statement that accounts for both these cost cutting measures and the forecasted increase in OEM sales (using management’s OEM forecast for 2004). That pro forma income statement is shown below, next to the Q3 2001 (annualized) figures and the year 2000 figures for comparison.1

As you can see, it seems plausible that Tenneco could once again become a profitable company. Perhaps more importantly, Tenneco seemed poised to almost double its EBIT from $115mn in the year 2000 to a pro forma $214mn.

Big deal. What about all the debt?

Of course, all this says nothing about paying down the extraordinary debt load the company was burdened with. However, I think these positive points are ultimately what caused Munger to believe that the company’s bonds, around a price of 35, and the company’s stock, around a price of $1.55 per share and a market cap of only $59mn, were way too cheap. For reference, the entire enterprise value of the company was $1.1bn, a figure I arrive at by conservatively assuming that the company’s debt is valued at par (apart from the 11 5/8% bonds, which I value at 35 cents).

I think Munger saw a very difficult financial situation for the company, and he probably acknowledged that a further, prolonged downturn in the economy and/or a group of unfriendly bank lenders could have pushed the company into bankruptcy. And in bankruptcy, in the wrong economic environment, it was quite possible that his debt and equity got wiped out.

The fact that Munger did not invest fully in Tenneco’s equity, which was more likely to be wiped out in bankruptcy, and chose to split his investment between bonds and equity, shows that he realized this was a possibility.

But more likely, by his judgment, the company could survive a recessionary environment (perhaps by delaying repayment on its debt through the use of its revolver for awhile and continuing to cut costs if the environment got worse). And yet, the pricing of the equity (at a market cap of $59mn) and the debt (at a price of 35 cents) was awarding almost no probability to a recovery.

Bankruptcy game theory

Now, here is the real kicker.

I think Munger likely reasoned about how a potential bankruptcy might play out, and I think this was the most important point of all, prompting him to make his investment.

If Tenneco was forced into bankruptcy, its lenders would then have to decide on the best course of action that might get them a full recovery on their lending amounts. The total amount of long-term debt outstanding was $989mn plus the $500mn of subordinate bonds which Munger would invest in.

Tenneco’s lenders would rightly ask themselves: How are we best off to recover our $989mn?

We could force a liquidation of the business and attempt to be paid in full. That would involve a few years of wind-down work, staggered employee layoffs and plant and equipment sales, along with the severance and interim operating costs that come along with it. Plus, we would also need to engage in a process to sell the valuable Walker and Monroe brands, two of the most valuable assets the company had.

Or...

We could effectively realize the value of those brands by recapitalizing the company and operating as usual. One way to do that might be to forgive Tenneco’s debt completely, take an equity stake in the new company without debt, and then sell the equity in the new company to make ourselves whole on the lending amounts.2

Munger may have realized that option number 2 (or some variant of it) looked pretty attractive from the perspective of the bankers, especially compared to the more cumbersome option 1.

Once again, the strength of Tenneco’s brands, as evidenced by the healthy operating profit they generated, may partly be what Munger was communicating when he spoke positively about them: “I... knew based on experience how sticky some of that auto secondary market was“. It may also have been part of the reason that Tenneco’s CFO, Mark McCollum, suggested in another article3 that delaying loan repayments by using capacity on the company’s revolving line of credit might be an appealing course of action to their lender, Chase Bank, for the time being:

Investors are worried whether Chase [Bank] would approve, and how the company will come up the money it needs going forward, said Peters.

McCollum said Chase, whose name is on the revolver, as well as the term loan, would not be opposed to such an “in one pocket, out the other” scenario.

“Are they [Chase] going to be happy? No. But they realize that it’s not a bad answer,” he said. Tenneco has $357 million left on the revolver.

Munger’s investment decision and outcome

In the end, Munger decided that the pricing of Tenneco’s 11 5/8% bonds (at 35) and its stock (around $1.55 and a market cap of $59mn) was accounting for too severe a set of outcomes and not enough for what was likely to happen based on (1) the strength of Tenneco’s brands, (2) management’s right-sizing initiatives, and (3) the likely game theory with Tenneco’s lenders.

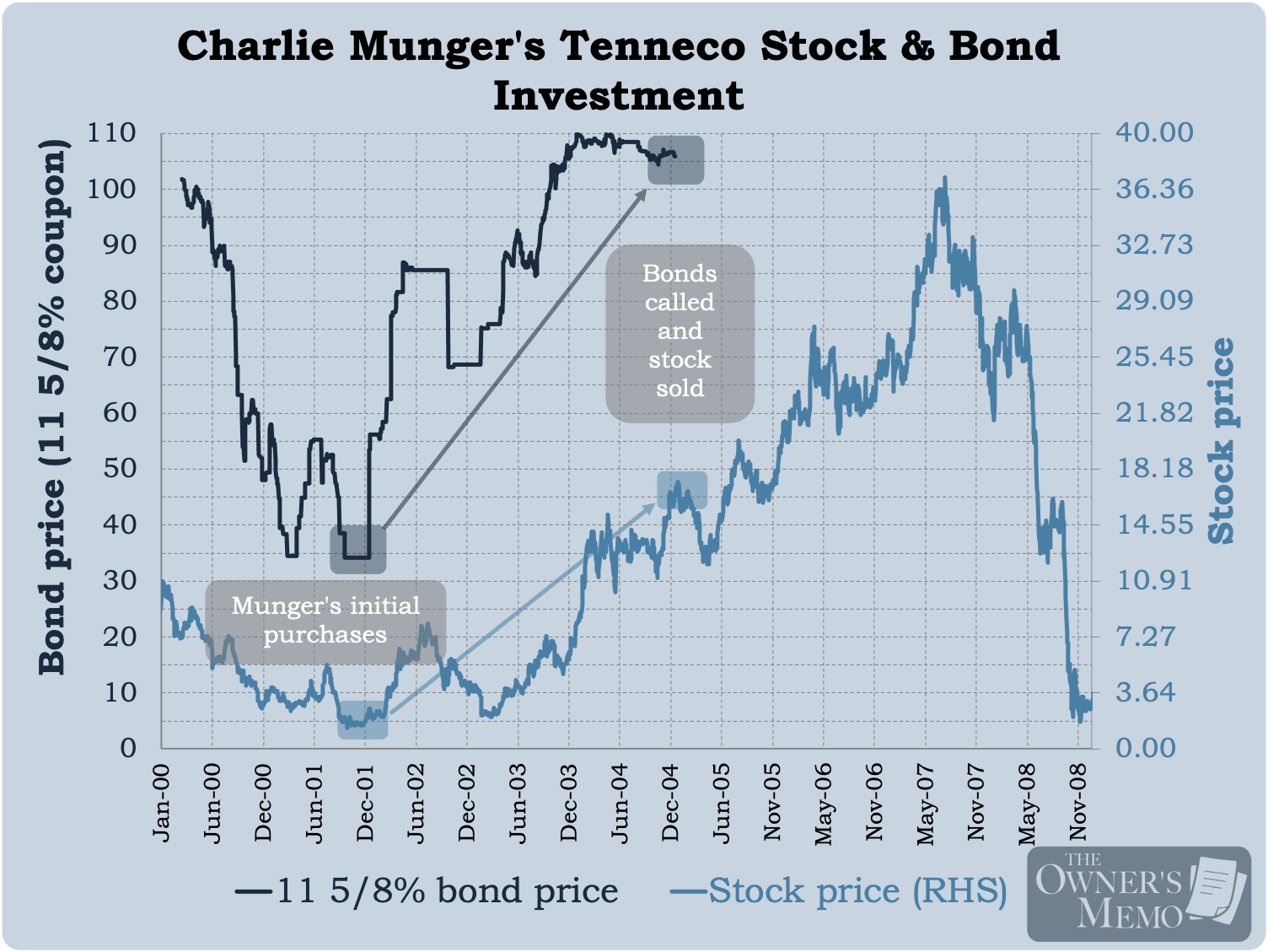

We know he purchased the bonds and stock around those levels, and we know, from his comments, that his bonds were called away from him and that he “sold [his] stock at 15”.

The chart below shows that Munger likely held his investment for three years until December 2004. Tenneco’s 11 5/8% bonds were called on December 20, 2004 at a price of 105.81, and its stock on that date closed at $16.44, close to Munger’s report of $15.

How much did Munger invest and make?

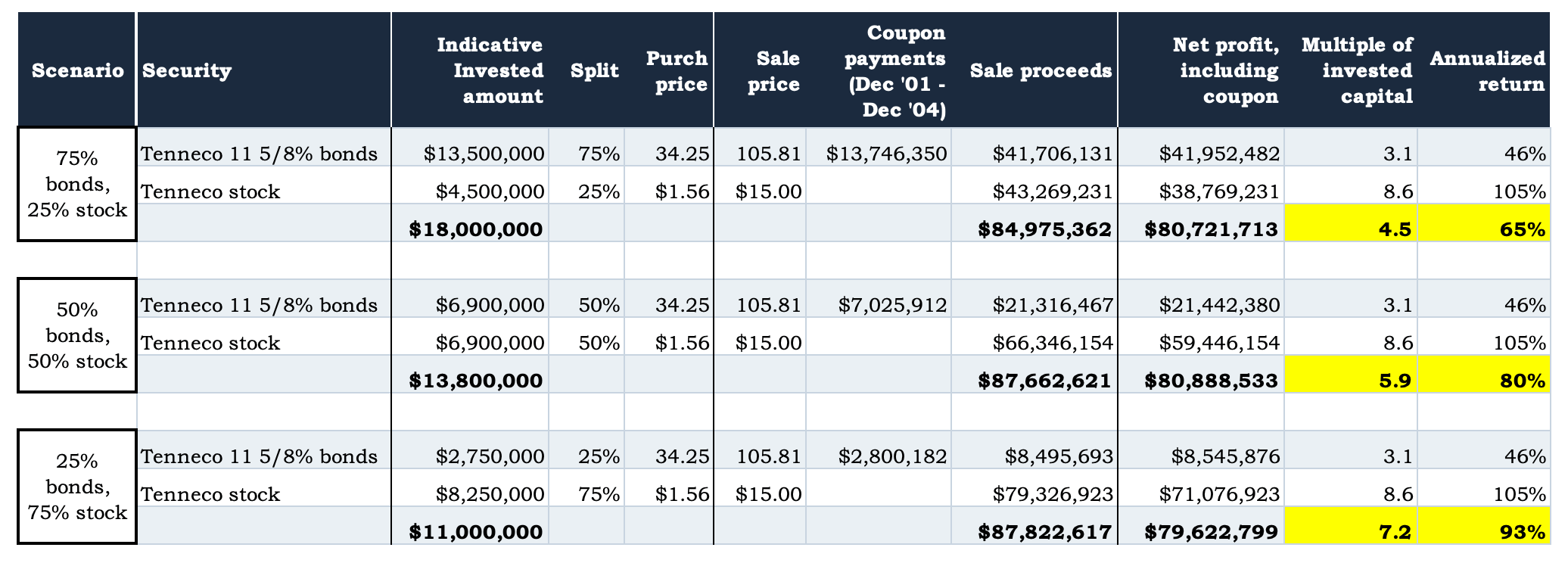

We also know that Munger made “$80mn” on the investment. But we don’t know specifically how much he invested in either of the securities. Let’s speculate on that for some fun.

The table below backs into rounded amounts that Munger is likely to have invested in each class of security, assuming:

he purchased the securities around the prices listed above,

the bonds were called from him at 105.81 in December 2004 and he sold the stock at $15 at that time as well, and

he made approximately $80mn on the trade in full, including bond coupon payments.

We don’t know how much he invested in each class, so I show the outcome of the trade if he put 25%, 50%, and 75% of his investable capital in each class. Corporate bond markets are typically much less liquid than equity markets. So, in practice, Munger may have simply had approximately $14mn to invest, bought as many bonds as were available, and then put the rest into Tenneco’s stock.

Assuming Munger invested somewhere between 25% and 75% in Tenneco’s bonds (and stock), he likely made anywhere from 4.5 times to 7.2 times on his investment in three years, from December 2001 to the time the bonds were called in December 2004 (and when he likely sold his stock as well). Those returns imply an annualized return of 65% to 93%.

Summary and takeaways

I think there is one clear takeaway from Munger’s Tenneco investment.

When you encounter a company with a quality, in-demand product and/or a great brand, and that company is suffering, look twice.

Tenneco manufactured a quality and beloved product, but it was being punished by the market because of the 2001 recession and a huge debt load from five past spinoffs and business sales.

But the recession’s impact appeared overblown, and we were able to see this with a detailed reading of the K’s and Q’s. Management was making great progress on a large cost-cutting initiative, and they had a book of orders that implied sales would be rising again.

The bankruptcy issues were scarier, perhaps, and the lesson there even more important. If a company has “hidden” assets, like a beloved product and/or a great brand (and could have a healthy business but for its debt), put yourself in the shoes of the lenders and ask “what is the best move for them?”

Postscript

In Munger’s discussion of the $80 million he made in the Tenneco investment, he also mentions that he “took the $80 million and gave it to Li Lu, who turned it into 4 or 5 hundred million dollars”.

In his foreword to Poor Charlie’s Almanack, from 2010, entitled “My Teacher: Charlie Munger”, Li mentions that Charlie first invested money with him in 2004, which lines up nicely with the timeframes presented above.

In 2004, Mr. Munger became my investment partner and has since become my lifelong mentor and friend — an opportunity I would have never dared to dream about.

I tried to keep the pro forma assumptions somewhat conservative. They are: (1) OEM revenues of $2,583mn as forecasted by management for the year 2004 from their 2000 annual report and aftermarket volumes of $968mn, which is 10% less than the year 2000 figures, (2) gross margins of 21.9%, the same as Q3 2001, (3) no further improvements to expenses versus that achieved by Q3 2001, (4) the same interest payments as represented by the Q3 2001 annualized figures, and (5) a tax rate of 30%.

Obviously, this is not a small matter. And I am dramatically simplifying the thought process here by saying that the lenders could ”forgive all the debt” (including that owned by bondholders). But I’m doing so to illustrate the point. Whether the newly imagined company had no debt or $500mn in debt (or an amount in between), it would be dramatically healthier, with an equity valuation that should reflect that.

That would be a much better path for a bank lender (and for bondholders) than liquidating the company. Ultimately, It’s that economic interest that should bring a bank lender and bondholders to the negotiating table. (And a shrewd investor would understand this and make an investment in anticipation of it being the best outcome.)

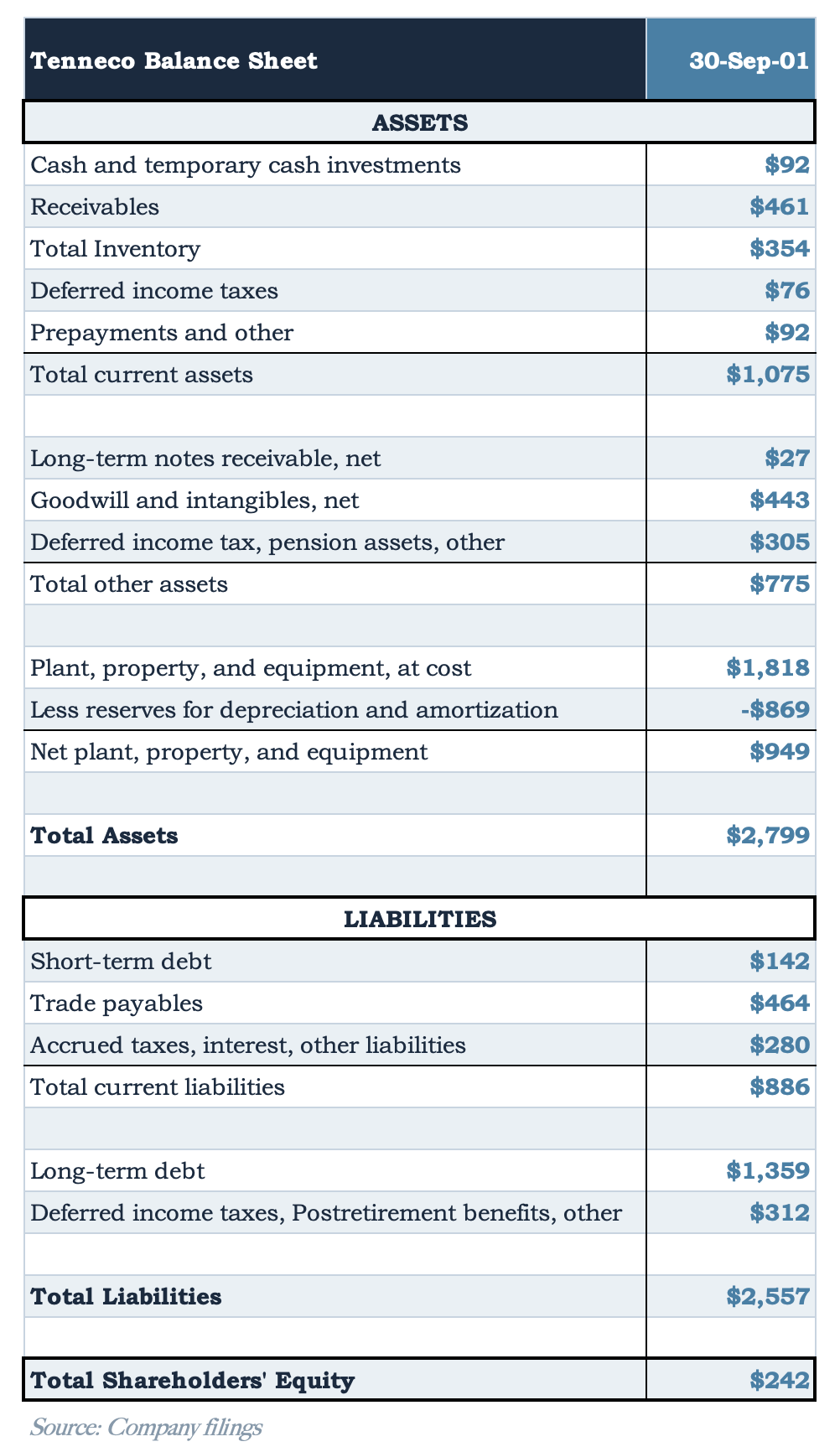

To allay a lingering doubt about the risk of a company liquidation, I’ve reproduced Tenneco’s balance sheet from Q3 2001 which shows that the company had $242mn of book value; the point here is that it would not be obvious to a bank lender that a liquidation of the company (after all costs) would provide enough proceeds to fully pay back $968mn of loan debt. That supports the allure of the equity recapitalization idea.

“Tenneco: Swerving Away from Chapter 11?”, Mergers & Acquisitions Report, September 10, 2001.

Thank you for publishing this article on mungers tennaco investment. Great reading material.... I always thought it was a pure cigar but play as when he talked about it he made it seem that way but after reading your write up. It's made me rethink that it was not just as simple as munger made it sound lol