A Penny on the Dollar: Li Lu's Bet on Russian Privatization, Part 3

The Owner's Memo #12; Li Lu's bold bet made him anywhere from 2.5 to 6.6 times his money in just over two years

In Parts One and Two, we discussed the government plan to privatize Russian businesses using an interesting voucher system after the fall of communism, and we saw just how cheap Russian businesses were at that time. We also discussed a host of risks in investing in the country at that time.

With the value case established and the risks weighed, we can now attempt to put together Li’s actual investment in Lukoil at the time.

Piecing Together Li’s Investment in the Company

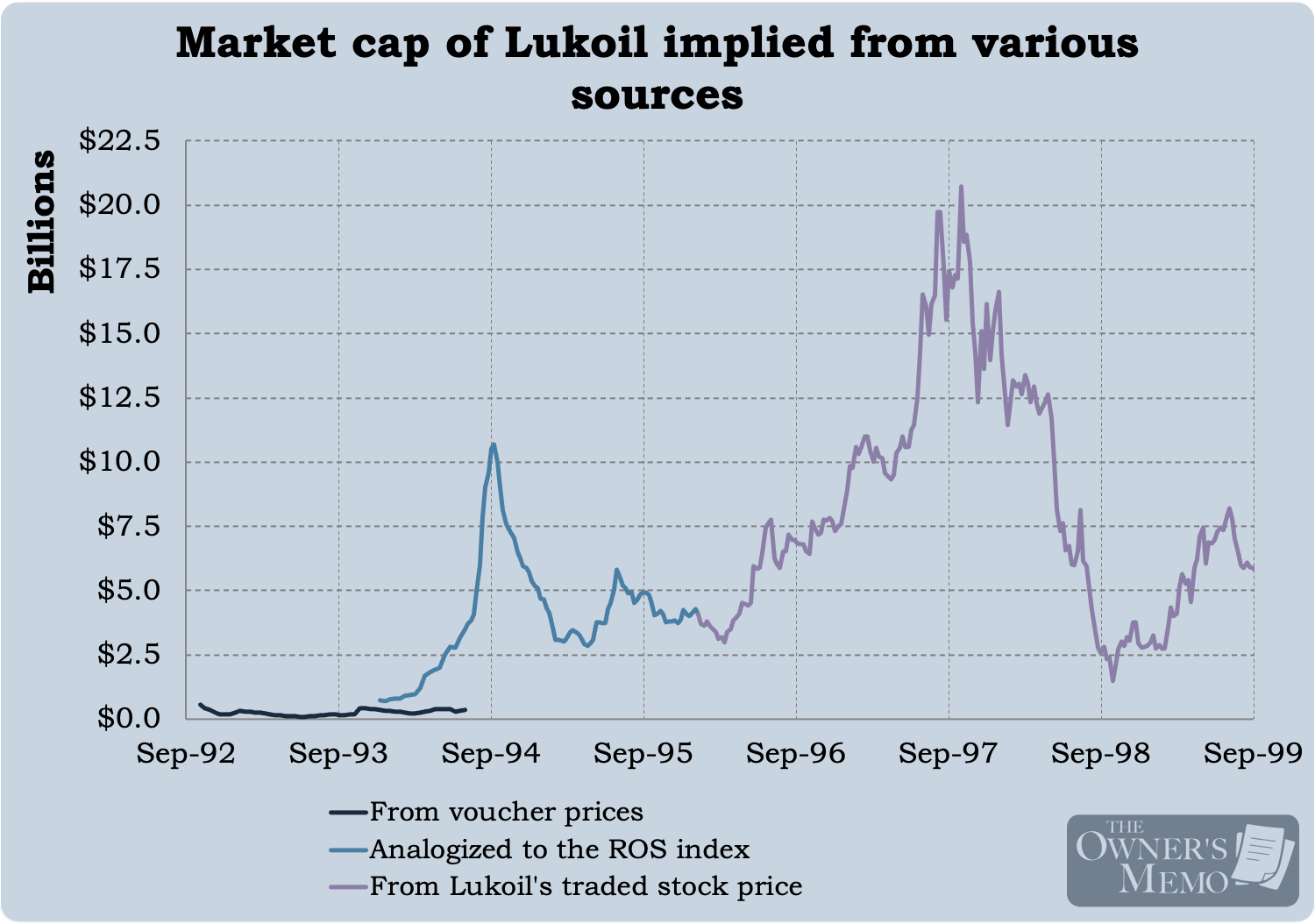

At the end of Part Two, we recreated Lukoil’s market cap from three different sources. I’ve reproduced that chart below.

Now that we have that recreation, can we piece together Li’s investment more specifically? Li speaks briefly and vaguely about the market prices of Lukoil and Gazprom around this time and is not very specific about the exact time when he bought and sold the stock, but he does provide some clues:

Forget about the earnings. Just... the assets on the balance sheet. At the time oil prices [in the world market], I think the four or five year average was around twenty dollars [per barrel], and the [value per barrel of proven oil reserves for Lukoil was] at really low prices... about 10 cents to 20 cents per proven barrel of oil on the balance sheet and that’s not even counting the earnings... This is how low it went. It was ridiculous.

From this quote and others throughout the talk, it seems that Li’s main focus was just how cheap Lukoil was trading relative to how much proven oil reserves were on its balance sheet. He seems to have virtually ignored any loss (or any income) that the company was making at the time, reasoning that such an extreme undervaluation relative to the company’s assets dwarfed the numbers on the income statement.

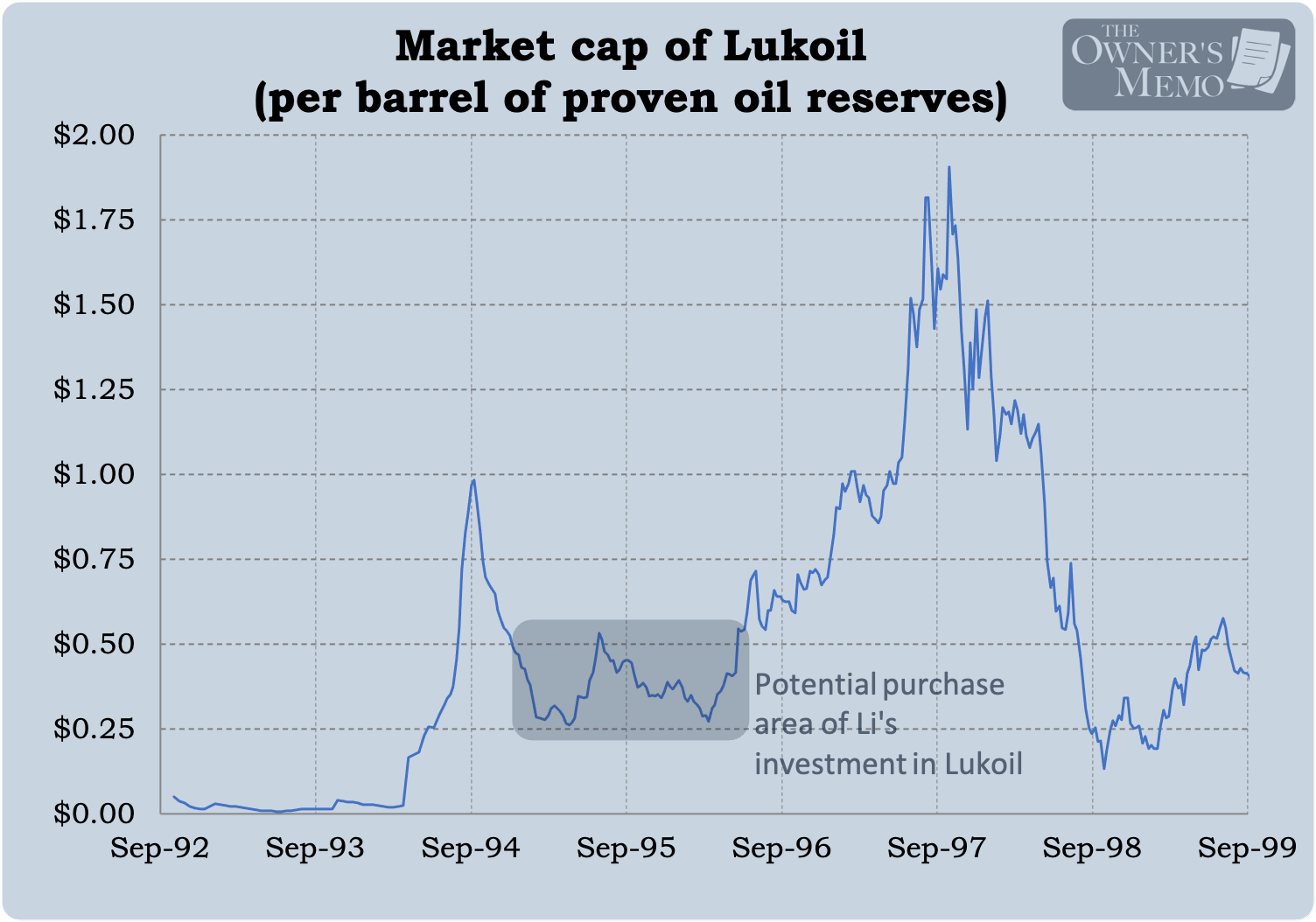

Let’s take Lukoil’s proven oil reserves of 10.9 billion barrels from its 1996 annual report and translate the above chart, this time showing the market cap of the company per proven barrel of reserves.

Now, we are beginning to see what Li saw around the time of his investment. More from Li’s talk:

For the longest period of time [the market cap of Lukoil or similar firms] was at 20 or 30 cents [per barrel of proven oil reserves], [then] 50 cents, then quickly moved to a dollar and briefly traded to three dollars.

From this quote (and Li’s discussion of the 1992-1994 voucher period in his talk), I am going to surmise that Li made his initial investment in Lukoil somewhere in early 1995 to mid-1996.

More clues:

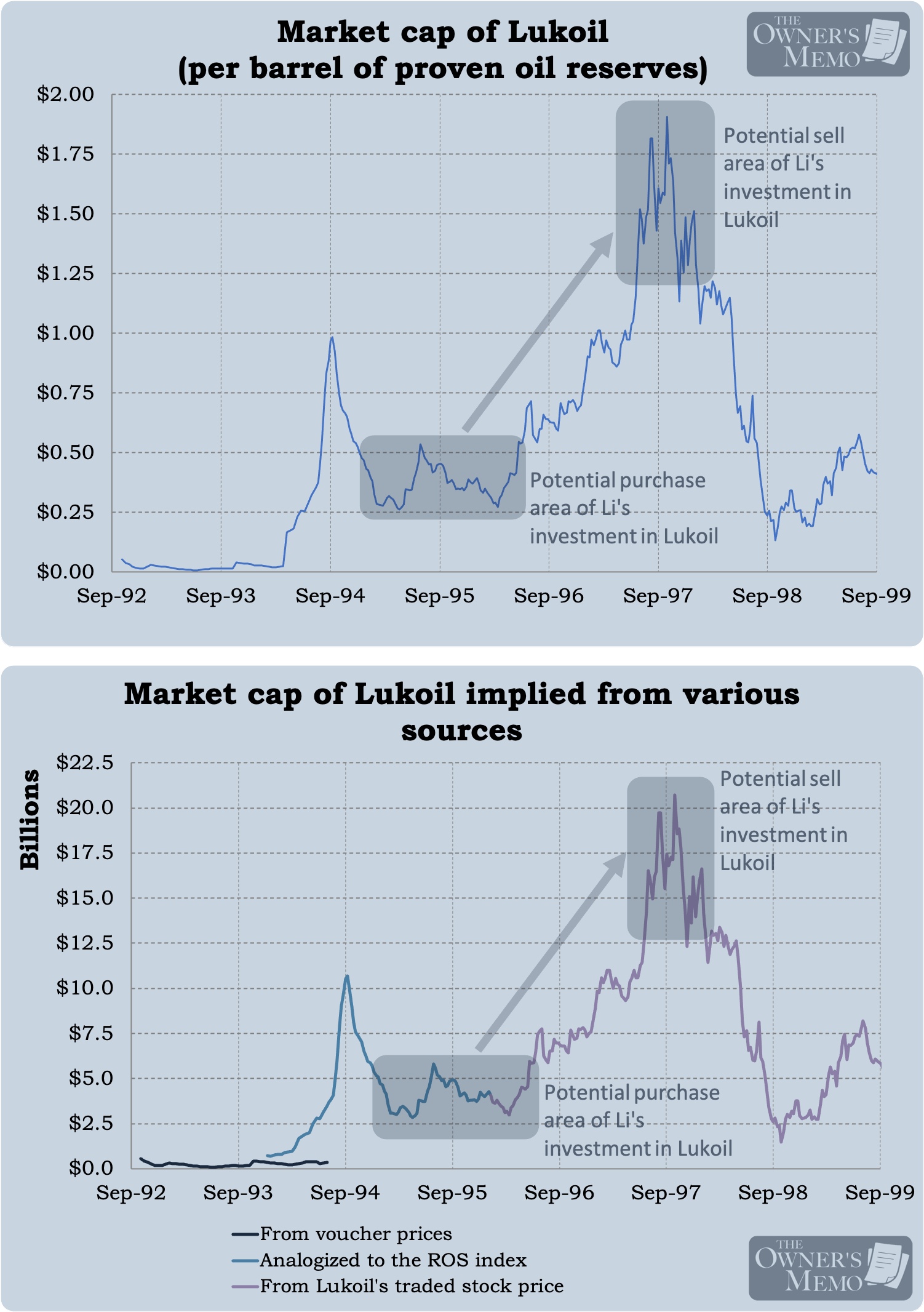

And then a few years later the Asian Financial Crisis occurred and Russia devalued the currency. All of a sudden that two dollars [per proven barrel of] oil no longer looks very protected because the currency [is] literally at one point... down ninety percent... But if you bought [Lukoil] at ten cents [per proven barrel of reserves]... you still came out all right. In fact, you still probably made 10 times your money.

For example... in Lukoil and Gazprom, I sold it two years after I first bought it... but at the time they [were] still kind of trading probably 80 to 90 percent discount, but i think the 80 to 90 percent discount is warranted somehow. Today [Author’s note: “today” was the year 2012], they are still trading at a huge discount.

When Li talks about the 80 to 90 percent discount for the stock, he seems to be referring to Lukoil’s market cap per proven barrel of oil and gas reserves versus the market price of crude oil. I’ve recreated that in the chart below, effectively showing the price of Lukoil’s stock (its market cap) versus the market price of Lukoil’s “stuff”: all of its proven oil and gas reserves.

When I saw this chart, I thought I might be off a bit, since Li mentions that he sold when Lukoil was trading at a discount of “80 to 90%”, but after extending this chart over an even longer timeframe, the market cap of Lukoil versus the market price of oil does not meaningfully cross 10% (which is a discount of 90%) until the year 2020! However, from the early 1995 to mid-1996 time period, Lukoil does go from trading around a 98% discount to a 91 or 92% discount.

All in all, with the limited information we have, I think the most reasonable conclusion is that Li made his initial investment in Lukoil somewhere in early 1995 to mid-1996 when the stock was trading around $3 billion to $5 billion in market cap and $0.30 to $0.50 per proven barrel of oil and gas reserves, and he sold it somewhere around mid-1997 to mid-1998, in the region of $12 billion to $20 billion of market cap and $1.25 to $2.00 per proven barrel of reserves. (Recall his comments from earlier, that he sold “two years after” he first bought it and that the $2.00 price per proven barrel of oil no longer looked protected.)

With those crude, round numbers, his investment would have made him anywhere from 2.5 to 6.6 times his money in just over two years of time.

Li Lu first got interested in investing after attending a lecture by Warren Buffett, who was invited to the school to speak, in 1993. (It is possible the exact date was October 27.) At the time of his investment in Lukoil, he may still have been a student at Columbia University, from which he graduated in 1996. He worked at the investment bank Donaldson, Lufkin & Jenrette for about one year before founding Himalaya Capital in 1997. It was likely right at the start of his work at Himalaya that he sold his stake in Lukoil (and any other Russian oil and gas companies he may have bought).

I mention this as a brief aside because it may suggest something about Li’s boldness of character. After first learning about investing just two or three years back, he had the temerity to both do the work on a foreign investment in an emerging democracy and to pull the trigger.

How Cheap Is Cheap Enough?

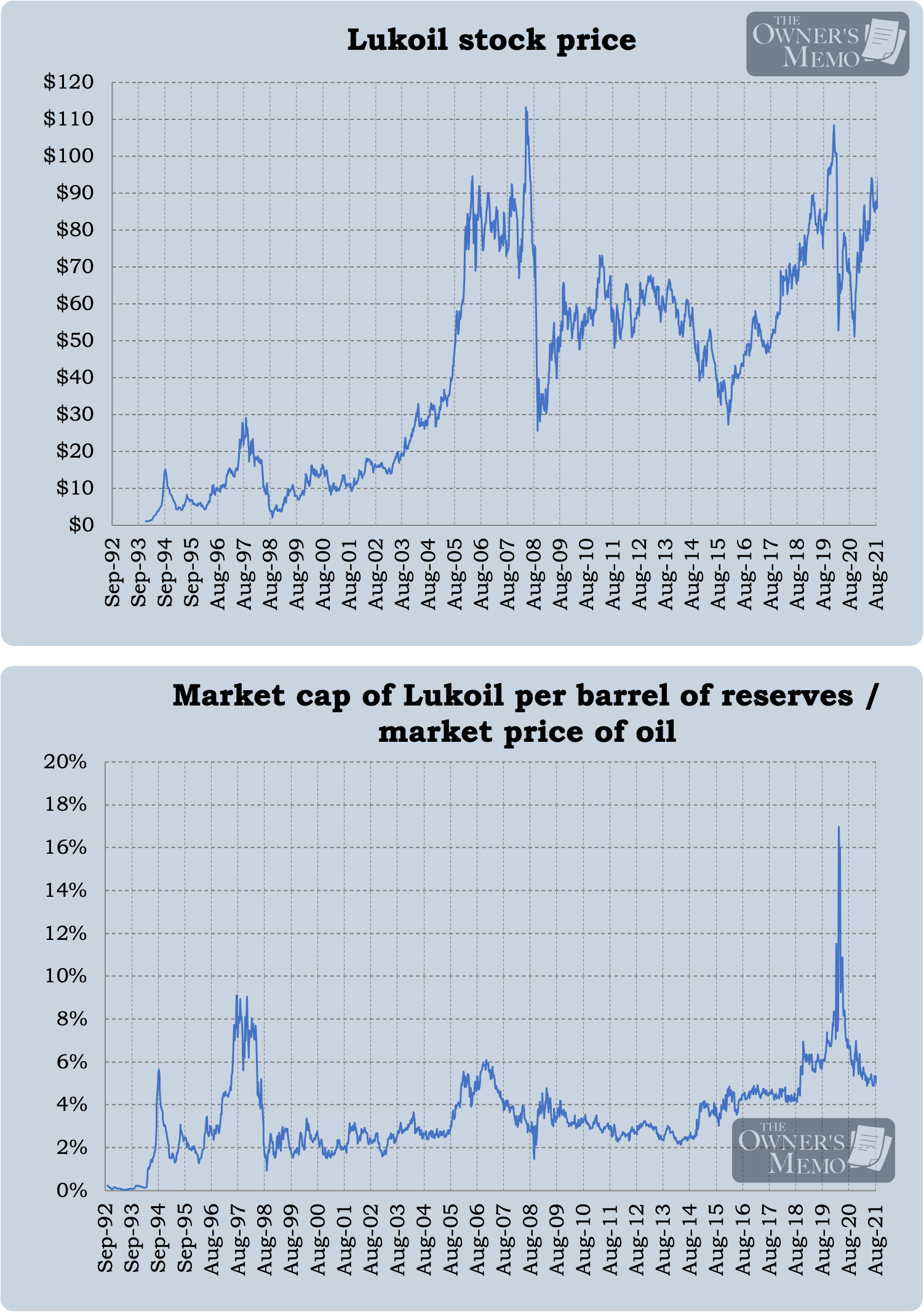

Li talks about the dramatic cheapness of Lukoil and other Russian stocks at the time, and he was right to some extent. But that cheapness had its limits. Below, I show the price of Lukoil’s stock from 1993 to 2021. I also show a variation of the chart with Lukoil’s market cap versus the value of its proven oil reserves (a measure of Lukoil’s “cheapness”).

The charts paint a picture that is difficult to rectify: For virtually the entire period from 1993 to 2021, Lukoil appeared to be cheap, trading at a market cap that almost never valued the entire company greater than 8% of the value of its proven oil and gas in the ground. Exxon (and later Exxon-Mobil), by comparison, averaged a market cap of 34% of the value of its reserves from 1993 to 2021.

So, at all points, an investor might have thought that Lukoil was cheap. And yes, buying the company’s stock in 1995 and holding it for two years, like Li, would have produced a great return. Even holding it for 10 years, from, say, June 1995 to June 2005 would have produced an annualized return (excluding dividends) of 21%, as the stock went from $5.21 to $34.75.

However, the next 10 years, through June 2015, would have only produced an annualized return of only 3%, despite the company appearing cheap in June 2005, when its market value was only 4.7% of the value of its reserves.

As Much As Possible, Seek a Catalyst

What are we to think about this? How are we to know, for future investment opportunities, when apparent cheapness is “real” and when it’s not?

This case study was particularly enjoyable for me because the lessons are so difficult to tease out. Simply buying Lukoil stock at any point in its history because it was cheap relative to other companies around the world would have been a mixed bag. Buying in the 1990’s or early 2000’s would likely have worked out great. Buying in the late 2000’s or the 2010’s would likely have been poor. At all times, Lukoil looked cheap versus Exxon and other western oil companies.

It is very difficult to know how to think about this issue, but one thing to keep in mind is the timing of Li’s investment. In the early to mid 90’s, Russia was emerging from communism and still getting accustomed to the cultural shift toward capitalism and democracy. One could argue that, although corruption was still rampant, the prevailing winds were blowing in the direction of a country getting more used to democracy and slowly reaping the benefits of capitalist markets. These trends could serve as a gradual but important kind of catalyst to close the gap between price and value. In Russia, for example, these changes would slowly lead to more Western investors participating in Russian markets through the 1990s and 2000s.

But it’s important to realize too that the lack of such change (or timing) could make for a difficult investing situation, whereby an investor thinks a stock is cheap by some measure but that situation sticks around for many years.

So one takeaway from Li’s investment is that extreme cheapness is a great thing to hunt for, but seek to have it come along with a changing situation or an outright catalyst.

Summary and Takeaways:

Li’s investment in Russian oil and gas companies in the 1990’s was a situation where the stocks were obviously cheap relative to the value of their assets and relative to other companies around the world.

Dramatic changes, like the shift from communism to liberal democracy in Russia, often come with extreme undervaluations.

It is very difficult and perhaps impossible to know just how much discount the market will demand of a given situation or investment. As much as possible, look for undervaluations that come with a naturally changing situation or an outright catalyst.